Commentary

Uri Dadush

{

"authors": [

"Uri Dadush"

],

"type": "legacyinthemedia",

"centerAffiliationAll": "",

"centers": [

"Carnegie Endowment for International Peace"

],

"collections": [],

"englishNewsletterAll": "",

"nonEnglishNewsletterAll": "",

"primaryCenter": "Carnegie Endowment for International Peace",

"programAffiliation": "",

"programs": [],

"projects": [],

"regions": [

"North America",

"United States",

"Western Europe"

],

"topics": [

"Economy"

]

}

Source: Getty

Countries that can afford to continue to spend, including the United States, should not abandon fiscal stimulus until the private sector recovery is clearer.

Source: Council on Foreign Relations

Countries that can afford to should continue fiscal stimulus until the private sector recovery is clearer. Among the G7, this group clearly includes the United States, Germany, France, and Canada, and may include Britain and Japan, but not Italy. Further fiscal stimulus is essential in Germany, where domestic demand is stagnant and exports are booming, putting even more pressure on the European periphery. Germany has too much at stake in the euro to pursue mercantilist policies. Booming China's massive stimulus must be withdrawn but gradually and with care, given the international uncertainty.

Originally published by the Council on Foreign Relations, July 15, 2010

Former Senior Associate, International Economics Program

Dadush was a senior associate at the Carnegie Endowment for International Peace. He focuses on trends in the global economy and is currently tracking developments in the eurozone crisis.

Recent Work

Uri Dadush

Uri Dadush

Carnegie India does not take institutional positions on public policy issues; the views represented herein are those of the author(s) and do not necessarily reflect the views of Carnegie, its staff, or its trustees.

On the last day of the India AI Impact Summit, India signed Pax Silica, a U.S.-led declaration seemingly focused on semiconductors. While India’s accession to the same was not entirely unforeseen, becoming a signatory nation this quickly was not on the cards either.

Konark Bhandari

This piece examines India’s response to U.S. sanctions and tariffs, specifically assessing the immediate market consequences, such as alterations in import costs, and the broader strategic implications for India’s energy security and foreign policy orientation.

Vrinda Sahai

This paper examines the evolution of India-China economic ties from 2005 to 2025. It explores the impact of global events, bilateral political ties, and domestic policies on distinct spheres of the economic relationship.

Santosh Pai

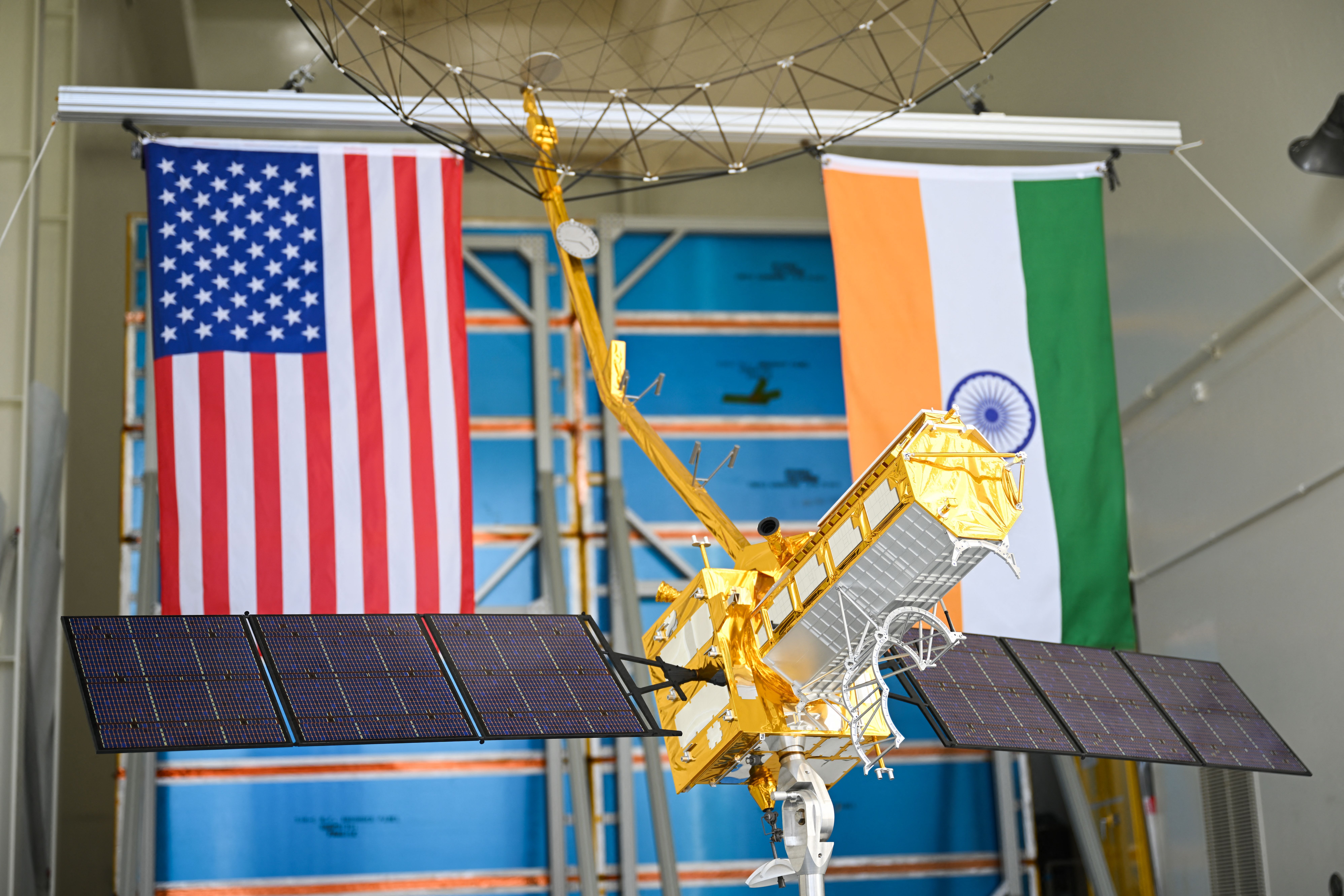

On July 30, 2025, the United States announced 25 percent tariffs on Indian goods. While diplomatic tensions simmered on the trade front, a cosmic calm prevailed at the Sriharikota launch range. Officials from NASA and ISRO were preparing to launch an engineering marvel into space—the NASA-ISRO Synthetic Aperture Radar (NISAR), marking a significant milestone in the India-U.S. bilateral partnership.

Tejas Bharadwaj

The India-U.S. relationship currently appears buffeted between three “Ts”—TRUST, Tariffs, and Trump.

Arun K. Singh