Financial Transmission of the Crisis: What’s the Lesson?

Ironically, the United States is among the countries least affected by the financial crisis. Financial markets have been hardest hit in Argentina and in Eastern European countries such as Ukraine and Hungary.

The current financial crisis is indisputably global in scope, impacting developed and developing, large and small, and open and less open economies. It has spread rapidly through multiple channels, including declines in trade volumes, commodity prices, remittances, and international credit.

This article takes a systematic look at the damage inflicted through financial channels. The financial channel of transmission is of special interest because although the crisis originated in industrialized countries, all of the developing countries were quickly―and disproportionately―affected by the ensuing credit crunch.

Even when the crisis originates in industrialized countries, developing countries are, in fact, highly vulnerable.

We find that several Eastern European countries and Argentina have been most affected through the financial channel, while the largest economies and those less open to the global financial system have remained the least impacted thus far. Ironically, among the least affected is the United States―the country where the crisis erupted―as it has so far succeeded in retaining its safe haven status.

Measuring the Impact of the Crisis

We generate our rankings by examining three of the most significant measures of financial weakness: currency devaluation, equity market decline, and rising sovereign bond spreads. Taken together, these criteria help capture, though imperfectly, the financial impact of the crisis. These indicators do not directly measure damage to the aggregates we care most about―such as GDP, industrial production, and unemployment―but they are available continuously and, during periods of financial strain, tend to track developments in the real economy, as financial strain handicaps consumption, investment, and in many cases government spending, thereby limiting GDP and employment growth.

This article examines the 38 countries for which data is available for all three indicators from the fallout in September 2008 to May 2009. Countries are ranked on each of these measures; these rankings are, in turn, averaged to form the overall rankings.

Eastern Europe and Argentina Hit the Hardest

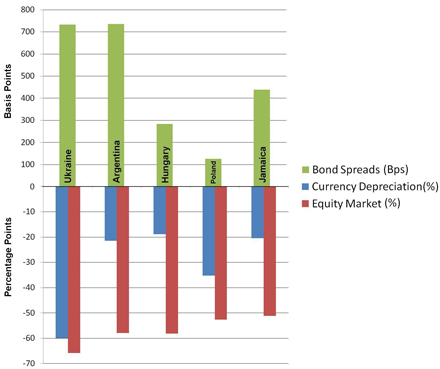

Currency Depreciation, Widening of Bond Spreads and Equity Market (September 2008–May 2009) The financial crisis has thrown the unprecedented development of past two decades in Eastern Europe into doubt, as the region, along with Argentina, emerges as the most severely impacted by the global downturn.

The financial shock to Ukraine has been huge. Bond spreads skyrocketed, increasing by 733 basis points since last fall on fears that the country would struggle to repay debt owed to foreign banks. The 25 percent crash in Ukraine’s stock market is related to the country’s high inflation, which reached 15.5 percent in the first half 2008. Currency depreciation has also been large; the hyryvnia has dipped by 60 percent since September, as exports fell and investors fled emerging markets. In turn, Ukraine’s economy contracted an annual 21.1 percent in the first quarter of 2009, following a contraction of 8 percent in the previous quarter. Industrial production dropped by more than 30 percent for the third month in a row in March.

Argentina is faring equally badly. Its stock market has tumbled 58 percent since September, while its bond spreads have widened by 735 basis points. Questionable policy choices (such as the 2008 nationalization of private pension funds), political uncertainty, and the deterioration of public finances have damaged confidence, sparking bank deposit withdrawals and capital flight, which reached $25 billion in the past year. In the midst of these developments, industrial production in Argentina fell 4.4 percent in January from a year earlier, the most in more than six years.

Hungary has also been severely impacted by the crisis. The stock market, which boasted gains of 10 percent in 2007, plunged by 45 percent in the second half of 2008. Meanwhile, bond spreads have widened by 283 basis points since September. In the same period, the forint has depreciated by 19 percent. The credit worthiness of local banks, companies, and private households, which hold predominantly foreign currency denominated debt, is deteriorating rapidly. The contraction in Hungary’s industrial production has reached double digit figures, plummeting by 28 percent in February. Real GDP contracted by 2.3 percent in the final quarter of 2008.

Developments in these most affected economies exhibited some common characteristics, including large current account and fiscal imbalances, high government debt, and large bank-related capital inflows prior to the crisis.

Countries Most Affected by the Financial Crisis , September 2008–May 2009

Rank

Country

Currency Depreciation (%)

Equity Market (%)

Bond Spreads(Bps)

1

Ukraine

-60

-66

733

2

Argentina

-21

-58

735

3

Hungary

-19

-58

283

3

Poland

-35

-53

127

4

Jamaica

-20

-51

439

Less Impacted Countries

China is among the least affected through the financial transmission channel. China’s banks, which operated in a relatively closed system for many years, have avoided much contact with toxic assets. China enjoys large current account surpluses and its fiscal position is strong. Furthermore, while China is feeling the slump of diminished export demand, its equity and debt markets are substantially less exposed to foreign investors than other emerging markets.

The largest industrial economies are also among the least affected. Although the three largest industrial economies―the United States, Japan, and Germany―have suffered large stock market declines, each has clearly benefited from a safe haven effect, resulting in declines in their less risky ten-year bond yields. The yen and U.S. dollar have appreciated vis-à-vis almost all other countries, and the euro has appreciated vis-à-vis most developing countries. All members of the euro-zone have seen their spreads widen vis-à-vis Germany. Dollar spreads of all countries have widened vis-à-vis the United States.

Ironically, among the least affected is the United States―the country where the crisis erupted―as it has so far succeeded in retaining its safe haven status.

However, Japan and Germany have also faced the sharpest declines in industrial production―30 percent and 19 percent, respectively, between September and March―driven by slumping global demand for advanced manufacturing products. Consistent with that picture, GDP in Japan dropped 15.4 percent at an annualized rate (saar) in the first quarter of 2009, while Germany’s GDP fell by 15.2 percent annual rate in the same quarter.

Ironically, despite reduced global demand for its exports, the net effect of international financial channels was to support U.S. activities, as money flowed into the dollar and U.S. assets. GDP in the first quarter of 2009 fell by 5.7 percent in the United States, and is expected to shrink by 4 percent overall for the year.

Policy Lessons

There are two main policy lessons to be drawn from this brief review, one familiar and one less so. The familiar lesson is that developing countries must use great caution in opening up their capital accounts and exposing their financial systems to shocks emanating from abroad. And as they integrate into global financial markets they can only do so sustainably if their macroeconomic policies are sound, they eschew large external deficits, and practice prudential regulation of banks.

Developing countries have a crucial interest in the financial soundness of the United States and other large financial centers.

The less familiar lesson is that, even when the crisis originates in industrialized countries, developing countries are, in fact, highly vulnerable to capital fleeing toward the source of the crisis. For that reason, developing countries have a crucial interest in the financial soundness of the United States and other large financial centers.

No wonder, then, that there has been a push to have the G20, rather than the G8, design the regime to govern international finance. Or that Brazil, Russia, India, and China (the BRICs) organized their first summit to discuss, among other things, the role of the dollar as the reserve currency. A country’s domestic financial health is now a global concern.

Appendix: Countries most affected by the financial crisis through financial channels

Rank**

Country

Currency Depreciation (%)

Bond Spreads(Bps)

Equity Market (%)

1

Ukraine

-59.9

733

-66

2

Argentina

-21.4

735

-58

3

Hungary

-18.9

283

-58

3

Poland

-35.2

127

-53

5

Jamaica

-20.4

439

-51

6

Ghana

-28.0

448

-35

7

Russia

-22.0

144

-44

8

Kazakhstan

-22.0

167

-34

9

Bulgaria

-1.5

175

-51

10

Mexico

-22.6

73

-35

11

Turkey

-21.7

44

-40

12

Greece

-1.2

95

-47

13

Sri Lanka

-6.6

464

-27

14

Indonesia

-8.8

85

-29

15

Austria

-1.2

39

-49

15

Pakistan

-6.3

132

-26

17

El Salvador

-0.3

176

-35

18

Vietnam

-7.1

53

-33

19

Italy

-1.2

13

-50

20

Lebanon

-0.3

57

-45

21

Netherlands

-1.2

17

-42

22

Brazil

-8.4

36

-28

23

Belgium

-1.2

14

-36

23

Chile

-5.5

80

-14

23

Tunisia

-7.7

62

-14

26

Ecuador

0.0

2528

-13

26

Egypt

-3.4

-137

-39

28

Spain

-1.2

20

-31

29

France

-1.2

11

-34

30

Colombia

-3.4

63

-10

30

Germany

-1.2

0

-34

32

Malaysia

-0.9

81

-12

33

Philippines

-0.1

53

-21

34

Peru

-0.4

42

-15

35

South Africa

1.5

39

-20

36

United states

0.0

0

-24

37

Japan

9.2

-5

-17

38

China

0.3

-31

-11

**Rank from most to least affected. The country with the greatest currency depreciation was given a 1 (data from Wall Street Journal). Local currencies were compared to U.S. dollar, U.S. given 0 percent in currency depreciation. The country with the largest percentage drop in equity markets was given a 1 (data from World Bank GEM, Japan data from MSCI Barra). The country with the largest growth in bond spreads was given a 1 (data for EU countries from The Economist; data for remaining countries from World Bank GEM). EU bond spreads were compared to the German bund, while other bond spreads were compared to U.S. Treasuries (U.S. and German were given 0).

Former Senior Associate, International Economics Program

Dadush was a senior associate at the Carnegie Endowment for International Peace. He focuses on trends in the global economy and is currently tracking developments in the eurozone crisis.

Lauren Falcão

Former Junior Fellow, Trade, Equity, and Development Program

Carnegie India does not take institutional positions on public policy issues; the views represented herein are those of the author(s) and do not necessarily reflect the views of Carnegie, its staff, or its trustees.

On March 10, 2026, India’s Union Cabinet approved amendments to Press Note 3, a regulation that mandated government approval on all foreign direct investment (FDI) from countries sharing a land border with India. This amendment raises questions primarily about whether its stated benefits will materialize and if the risks have been adequately weighed. This piece will address the same.

This piece examines India’s response to U.S. sanctions and tariffs, specifically assessing the immediate market consequences, such as alterations in import costs, and the broader strategic implications for India’s energy security and foreign policy orientation.

This paper examines the evolution of India-China economic ties from 2005 to 2025. It explores the impact of global events, bilateral political ties, and domestic policies on distinct spheres of the economic relationship.

This article argues that the geopolitical circumstances have never been more conducive, not merely for the early conclusion of the free trade agreement (FTA) between India and the EU, but also for crafting a substantive and comprehensive strategic partnership.