Commentary

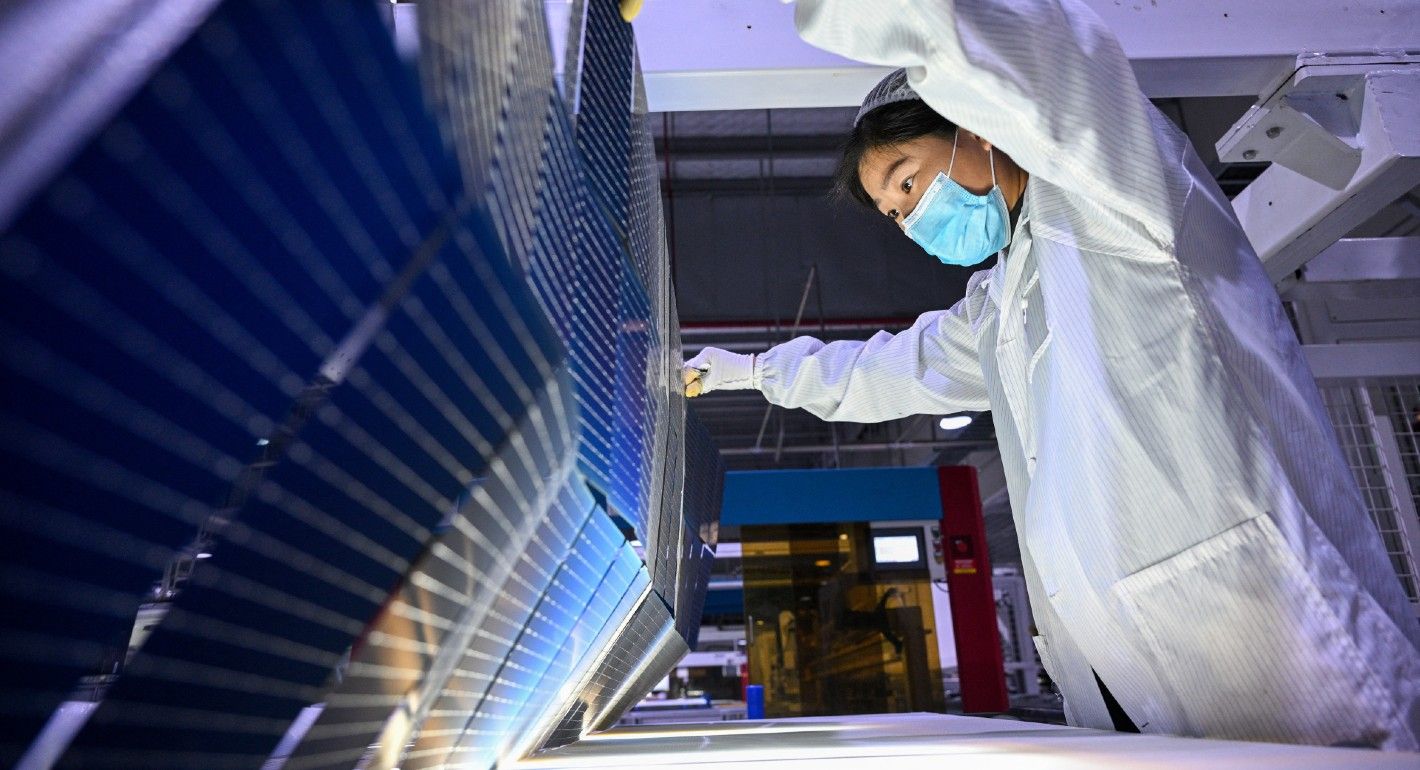

Rather than climate ambitions, compatibility with investment and exports is why China supports both green and high-emission technologies.

Mathias Larsen

{

"authors": [

"Pekka Sutela"

],

"type": "other",

"centerAffiliationAll": "",

"centers": [

"Carnegie Endowment for International Peace"

],

"collections": [],

"englishNewsletterAll": "",

"nonEnglishNewsletterAll": "",

"primaryCenter": "Carnegie Endowment for International Peace",

"programAffiliation": "",

"programs": [],

"projects": [],

"regions": [

"Western Europe"

],

"topics": [

"Economy"

]

}

REQUIRED IMAGE

Unless a major crisis erupts in Europe, Finland’s fiscal prudency and solid banks might well satisfy the markets.

Carnegie does not take institutional positions on public policy issues; the views represented herein are those of the author(s) and do not necessarily reflect the views of Carnegie, its staff, or its trustees.

Rather than climate ambitions, compatibility with investment and exports is why China supports both green and high-emission technologies.

Mathias Larsen

“Involution” is a new word for an old problem, and without a very different set of policies to rein it in, it is a problem that is likely to persist.

Michael Pettis

While China's investment story seems contradictory from the outside, the real answers to Beijing's high-quality growth ambitions are hiding in plain sight across the nation's cities.

Yuhan Zhang

China's stimulus addiction cannot go on forever. Beijing still has policy space to clean up the country's massive debt issue, but time is running short.

Michael Pettis

A quick look at the complexities behind Beijing’s enduring Catch-22 situation with revaluing the Renminbi, despite advantages of a stronger currency.

Michael Pettis