In The Media

David Rothkopf

{

"authors": [

"David Rothkopf"

],

"type": "legacyinthemedia",

"centerAffiliationAll": "",

"centers": [

"Carnegie Endowment for International Peace"

],

"collections": [],

"englishNewsletterAll": "",

"nonEnglishNewsletterAll": "",

"primaryCenter": "Carnegie Endowment for International Peace",

"programAffiliation": "",

"programs": [],

"projects": [],

"regions": [

"North America",

"United States",

"South America",

"Saudi Arabia",

"China"

],

"topics": [

"Economy",

"Trade"

]

}

Source: Getty

As world leaders prepare for next month’s international financial summit, critics remain skeptical about how quickly the IMF and the World Bank can actually adapt to the 21st century. Yet the mere fact that the upcoming summit will include leaders from the G20—rather than just the G7, as tradition would have it—suggests that the world is moving toward an unprecedented new financial order.

Source: The Daily Beast

For some, discussion of the International Monetary Fund or the World Bank means one thing: sex scandals. (Who knew conditional financing was an aphrodisiac?) For others, the two institutions evoke a different reaction. Anger mostly. Mixed with resentment and distrust.

Making the people of emerging economies do a dance choreographed in Washington for the money they need produces that kind of reaction--especially when to many in the countries that are supposed to be helped it seems like much of the money ends up siphoned off by corrupt leaders or wasted on bloated infrastructure projects. It’s little wonder that in developing countries, I.M.F. has inspired its fair share of nasty nicknames.

But set aside those preconceived notions of long, boring meetings discussing balance of payments problems and consider what the upcoming summit is likely to achieve. First, it will seek to create a system that will help prevent a financial crisis like the current one from happening again. That will entail creating the global supervisory and regulatory mechanisms we lack and beefing up the ones we have got. It will also mean taking the Fund and the Bank by the elbow and walking them into the 21st Century.

This will be difficult. Bush, who agreed to the summit during a Camp David meeting with Sarkozy, has already started to make unconstructive noises. Administration officials have said we don’t need more effective global regulation, we just need better cooperation among national regulators. This despite abundant clear evidence to the contrary that such voluntary cooperation hasn’t worked--from Jim Cramer cowering under his desk at CNBC to our ever-diminishing 401K statements.

Without global supervision and regulation, the weakest national regulatory scheme will end up setting the rules for the rest of the international markets as the dubious and the dishonest financial operators gravitate to the places they are least likely to get caught. Furthermore, this past crisis was only a symptom of what happens when you have a massive, complex, opaque global financial system that has grown both radically different from anything current institutions were designed to manage and well beyond the ken of current regulators.

And reforming the IMF and the World Bank may prove to be just as hard. The one thing big bureaucracies do well is resist change.

But whether or not the meetings end up making progress, in one sense the organizers remade the world the moment they sent out invitations to the summit. Because they realized that for the summit to have a chance at creating institutions that reflect the new global financial order, they would have to redefine the concept of who are the leaders of the international economic community. And while many of the old gang who have been at every such meeting since the victors set up the ground rules for the Post-World War II era in 1945 will be there, it’s the new faces who will really underscore the sea-change that is taking place.

Among the few apparent positive outcomes of this crisis is that it has made it clear that the old self-anointed club of countries that have run the economic world for as long as anyone working can remember, the G7, simply can’t get it done any more. With the G1 (that’s us, folks) bending under $11 trillion in debt and others in the group (ciao, Italy) who clearly aren’t in the same league as some who have too long been absent (the Chinese, from whom we have borrowed $500 billion, India, and Brazil), a change in the seating arrangement at the world’s head table is long overdue.

Thus, when Dana Perino announced at the White House yesterday that the upcoming summit would be attended by the members of the G20, it may well turn out that it amounted to one of the high water markets of a Bush presidency that has almost always run dry when it comes to understanding and adapting to the big changes effecting the planet. It meant that along with the usual suspects, the solutions to this crisis would be hashed out by a group including Argentina, Australia, Brazil, China, India, Indonesia, Mexico, Russia, Saudi Arabia, South Africa, South Korea and Turkey.

Once this larger group gathers in Washington next month, it will be as difficult as it would be wrong to go all the way back to the old group of established powers for other such efforts. A reordering of the top group in finance and economics will also prompt new orders elsewhere, in the UN Security Council perhaps, and even in the list of nations America may treat as fellow major powers. What we are witnessing therefore is nothing less than a redefinition of who will lead the international system in the century ahead.

In the end, of course, having 20 nations at all such meetings is likely to prove unwieldly, and different organizations may and should seek somewhat different collections of the most important major and emerging countries. Robert Zoellick, the World Bank’s very effective president, has, for example, argued for a global financial “steering committee” of 14 countries. The group would be the old G7 plus China, India, Brazil, Russia, Saudi Arabia and South Africa. He argues however, that its membership should not be as rigid as the G7 ‘s was and that it should grow and change as circumstances require.

Zoellick notes this core group represents “70 percent of the World’s GDP, 62 percent of its energy production, the major carbon emitters, the principal development donors, large regional actors, and the primary players in global capital, commodity, and exchange rate markets.”

But whatever the final structure, we should welcome this conference, even if it produces less than envisioned. It will mark a long overdue historical watershed and produce a system that might just work better if only because it is much more truly reflective of both 21st Century economic reality and of a more diverse and representative cross section of the world’s people.

This article originally appeared on The Daily Beast.

Former Visiting Scholar

David Rothkopf was a visiting scholar at the Carnegie Endowment as well as the former CEO and editor in chief of the FP Group.

Recent Work

David Rothkopf

David Rothkopf

Carnegie India does not take institutional positions on public policy issues; the views represented herein are those of the author(s) and do not necessarily reflect the views of Carnegie, its staff, or its trustees.

On the last day of the India AI Impact Summit, India signed Pax Silica, a U.S.-led declaration seemingly focused on semiconductors. While India’s accession to the same was not entirely unforeseen, becoming a signatory nation this quickly was not on the cards either.

Konark Bhandari

This piece examines India’s response to U.S. sanctions and tariffs, specifically assessing the immediate market consequences, such as alterations in import costs, and the broader strategic implications for India’s energy security and foreign policy orientation.

Vrinda Sahai

This paper examines the evolution of India-China economic ties from 2005 to 2025. It explores the impact of global events, bilateral political ties, and domestic policies on distinct spheres of the economic relationship.

Santosh Pai

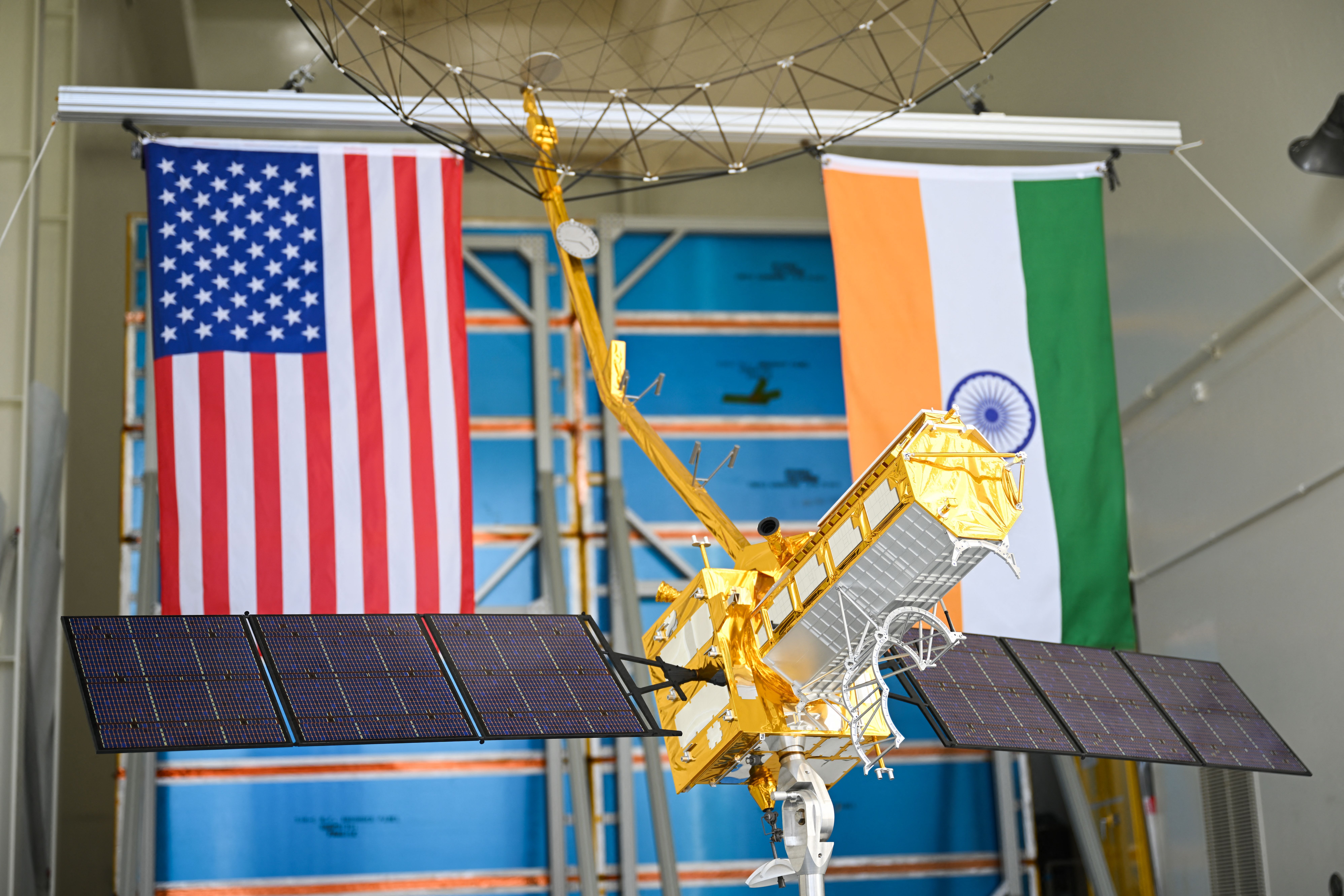

On July 30, 2025, the United States announced 25 percent tariffs on Indian goods. While diplomatic tensions simmered on the trade front, a cosmic calm prevailed at the Sriharikota launch range. Officials from NASA and ISRO were preparing to launch an engineering marvel into space—the NASA-ISRO Synthetic Aperture Radar (NISAR), marking a significant milestone in the India-U.S. bilateral partnership.

Tejas Bharadwaj

This article examines the scale and impact of Chinese IUU fishing operations globally and identifies the nature of the challenge posed by IUU fishing in the Indian Ocean Region (IOR). It also investigates why existing maritime law and international frameworks have struggled to address this growing threat.

Ajay Kumar, Charukeshi Bhatt