Commentary

Michael Pettis

{

"authors": [

"Michael Pettis"

],

"type": "legacyinthemedia",

"centerAffiliationAll": "dc",

"centers": [

"Carnegie Endowment for International Peace"

],

"collections": [],

"englishNewsletterAll": "asia",

"nonEnglishNewsletterAll": "",

"primaryCenter": "Carnegie Endowment for International Peace",

"programAffiliation": "AP",

"programs": [

"Asia"

],

"projects": [],

"regions": [

"North America",

"United States",

"East Asia",

"China"

],

"topics": [

"Economy"

]

}

Source: Getty

Asian countries are responding to the economic crisis with policies that may temporarily boost growth but that are likely to make the transition from a development model that emphasizes personal savings and increasing production more difficult.

Source: Financial Times

At the centre of the Asian development model, with China providing a steroid-fuelled example, were policies aimed at mobilising high levels of domestic savings and channelling massive investment into productive capacity. These policies boosted savings by constraining consumption even while they forced rapid growth in domestic production. One of the consequences of the Asian development model has been that production outgrew consumption for decades. When a country produces more than it consumes, it must run a trade surplus to export its excess capacity. The Asian model consequently required high and rising trade surpluses that allowed Asian producers to produce far in excess of what Asian consumers could afford to absorb.

But there cannot be trade surpluses without trade deficits elsewhere. A fundamental requirement for the Asian model was that foreigners were able to run the requisite trade deficits. In practice, only the US economy and financial system were large and flexible enough to play this role. The Asian model, in other words, implicitly involved a massive bet on the willingness and ability of the US to continue to run large and rising trade deficits.

For nearly two decades US households borrowed recklessly to finance the consumption binge that allowed Asian exporters to continue exporting excess capacity but, as household balance sheets in the US became vastly overextended, it was just a question of time before a long deleveraging process would occur. The global financial crisis is part of this very process.

As a consequence, US consumption will grow more slowly than US gross domestic product for many years. This is another way of saying that the US trade deficit must fall and may even become a trade surplus. Since it is clear that Europe, the only other economy large enough to replace the US, is too sickly and indebted to take up the slack, for the next several years Asians will not be able to continue running massive trade surpluses to absorb their excess capacity.

So what can they do? If Asian countries could boost domestic net consumption as rapidly as US net consumption declines, none of this would matter. Unfortunately, and if history is any guide, this is going to take much longer than many hope. The transition from an export-led economy to a domestic consumption-led model involves a long restructuring of the financial system and household behaviour, and a major reversion away from political structures and industrial policies that powered growth in the past.

But, wedded as they are to an outmoded development ideology and rigid industrial and financial systems, many Asian policymakers are making things worse. They are attempting to raise domestic consumption by accelerating the policies that are bankrupt.

These investment-oriented policies raise consumption indirectly, by boosting production, and so although they temporarily boost growth, they cannot result in a sufficiently large increase in domestic net consumption to replace American buying. What is worse, in some cases these policies will sharply constrain future domestic consumption, just when it is needed most.

For example, the unprecedented loan expansion that Chinese policymakers have encouraged in the past five months is not only targeted primarily at boosting investment, but will almost certainly result in a massive expansion in future non-performing loans. As these become apparent and threaten the viability of the banking system, Beijing will be forced to respond, as it did in the past, with policies that further constrain consumption – either by forcing lower deposit rates to increase bank profitability or by capturing savings to recapitalise the banks.

The risk is that China’s transition will be made worse by policies whose effect will be to cause a short-term and unsustainable rise in fiscal borrowing, bank debt and corporate inventory. Eventually working these off will make the transition to a domestic-led economy slower and more painful.

The assumption that implicitly underlay the Asian development model – that US households had an infinite ability to borrow and spend – has been shown to be false. This spells the end of this model as an engine of growth. The sooner Asian policymakers accept this and force through the necessary economic and political changes, the less painful the transition will be. Unfortunately this does not seem to be happening.

Nonresident Senior Fellow, Carnegie China

Michael Pettis is a nonresident senior fellow at the Carnegie Endowment for International Peace. An expert on China’s economy, Pettis is professor of finance at Peking University’s Guanghua School of Management, where he specializes in Chinese financial markets.

Recent Work

Michael Pettis

Michael Pettis

Carnegie India does not take institutional positions on public policy issues; the views represented herein are those of the author(s) and do not necessarily reflect the views of Carnegie, its staff, or its trustees.

India and the United States are close to concluding a Reciprocal Defense Procurement Agreement (RDPA) that will allow firms from the two countries to sell to each other’s defense establishments more easily. While this may not remedy the specific grievances both sides may have regarding larger bilateral issues, an RDPA could restore some momentum, following the trade deal announcement.

Konark Bhandari

On the last day of the India AI Impact Summit, India signed Pax Silica, a U.S.-led declaration seemingly focused on semiconductors. While India’s accession to the same was not entirely unforeseen, becoming a signatory nation this quickly was not on the cards either.

Konark Bhandari

This piece examines India’s response to U.S. sanctions and tariffs, specifically assessing the immediate market consequences, such as alterations in import costs, and the broader strategic implications for India’s energy security and foreign policy orientation.

Vrinda Sahai

This paper examines the evolution of India-China economic ties from 2005 to 2025. It explores the impact of global events, bilateral political ties, and domestic policies on distinct spheres of the economic relationship.

Santosh Pai

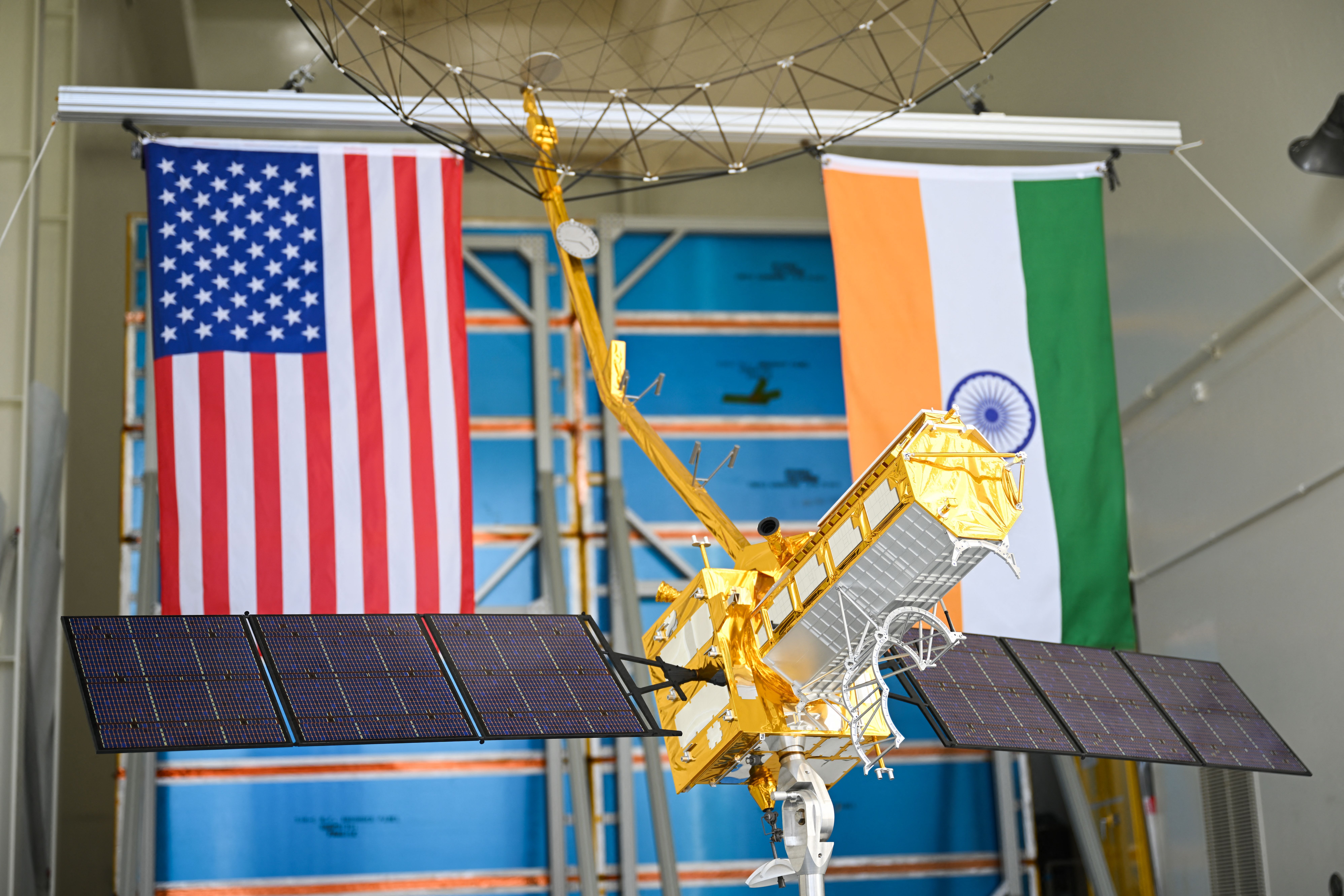

On July 30, 2025, the United States announced 25 percent tariffs on Indian goods. While diplomatic tensions simmered on the trade front, a cosmic calm prevailed at the Sriharikota launch range. Officials from NASA and ISRO were preparing to launch an engineering marvel into space—the NASA-ISRO Synthetic Aperture Radar (NISAR), marking a significant milestone in the India-U.S. bilateral partnership.

Tejas Bharadwaj