Commentary

Uri Dadush

{

"authors": [

"Uri Dadush"

],

"type": "legacyinthemedia",

"centerAffiliationAll": "",

"centers": [

"Carnegie Endowment for International Peace"

],

"collections": [],

"englishNewsletterAll": "",

"nonEnglishNewsletterAll": "",

"primaryCenter": "Carnegie Endowment for International Peace",

"programAffiliation": "",

"programs": [],

"projects": [],

"regions": [

"North America",

"United States"

],

"topics": [

"Political Reform",

"Economy"

]

}

Source: Getty

Because the U.S. economy is both competitive and flexible, policy makers in the United States can afford to be bold in tackling the country’s large fiscal problem.

Source: Financial Times

Precisely because of concerns about the US fiscal trajectory, however, and given that the US economy is in the middle of a recovery, I am less convinced by his call to hold on implementation of the programme “over the next two to three years until the recovery takes hold”. Though there is a case for targeted support for the unemployed – unemployment remains high and long-term unemployment is higher still (45 per cent of the unemployed have been so for more than six months compared to an average of 18 per cent since 1980) – the US economy is likely to continue to expand and create new jobs.

Recent indicators point to a US corporate sector in good shape, with capacity utilisation only about 2 per cent below the 20-year average, consumer confidence resilient and world trade continuing to grow rapidly; these factors together with low interest rates will play an important role in propping up demand. Again delaying budget consolidation in this situation may well be counterproductive, especially if it undermines confidence about the government’s determination to put its fiscal house in order, as it might well.

Partly because it has paid so little attention to it so far, there is lot that the US can do to correct its fiscal trajectory. US tax revenue over the last decade is the second lowest among the larger advanced countries, after Japan – whose public finances are in disastrous shape. The taxes paid by US corporations represent a much lower share of gross domestic product than either Greece or Italy, according to the Organisation for Economic Co-operation and Development. The US gasoline tax is a fraction of the OECD average.

The International Monetary Fund projects that US gross debt will reach 112 per cent of GDP in 2016; the only countries with higher debt are Japan and three European periphery countries under market attack: Italy , Greece and Ireland . However, among this group, only Japan will see a larger deterioration in its debt/GDP ratio than the US over the next five years. Net debt levels (excluding US government debt held by the Federal Reserve and other public agencies) are lower all around, but tell the same story. The US is also a complete outlier in its spending on healthcare and defence. And, like most other advanced countries, the US will see a large deterioration in its fiscal balances just as a result of aging: its old age dependency ratio is projected to rise from 19.5 per cent in 2010 to 32.7 per cent in 2030.

Unlike Italy, Greece and other European countries in bad fiscal shape, the US can count on a highly competitive and flexible private sector, an independent monetary policy, flexible exchange rate and, for the time being at least, its safe haven status and unparalleled ability to attract foreign investors. For these reasons, it can afford to be bolder than even Mr Rubin suggests in tackling its large fiscal problem.

Former Senior Associate, International Economics Program

Dadush was a senior associate at the Carnegie Endowment for International Peace. He focuses on trends in the global economy and is currently tracking developments in the eurozone crisis.

Recent Work

Uri Dadush

Uri Dadush

Carnegie India does not take institutional positions on public policy issues; the views represented herein are those of the author(s) and do not necessarily reflect the views of Carnegie, its staff, or its trustees.

India and the United States are close to concluding a Reciprocal Defense Procurement Agreement (RDPA) that will allow firms from the two countries to sell to each other’s defense establishments more easily. While this may not remedy the specific grievances both sides may have regarding larger bilateral issues, an RDPA could restore some momentum, following the trade deal announcement.

Konark Bhandari

On the last day of the India AI Impact Summit, India signed Pax Silica, a U.S.-led declaration seemingly focused on semiconductors. While India’s accession to the same was not entirely unforeseen, becoming a signatory nation this quickly was not on the cards either.

Konark Bhandari

This piece examines India’s response to U.S. sanctions and tariffs, specifically assessing the immediate market consequences, such as alterations in import costs, and the broader strategic implications for India’s energy security and foreign policy orientation.

Vrinda Sahai

This paper examines the evolution of India-China economic ties from 2005 to 2025. It explores the impact of global events, bilateral political ties, and domestic policies on distinct spheres of the economic relationship.

Santosh Pai

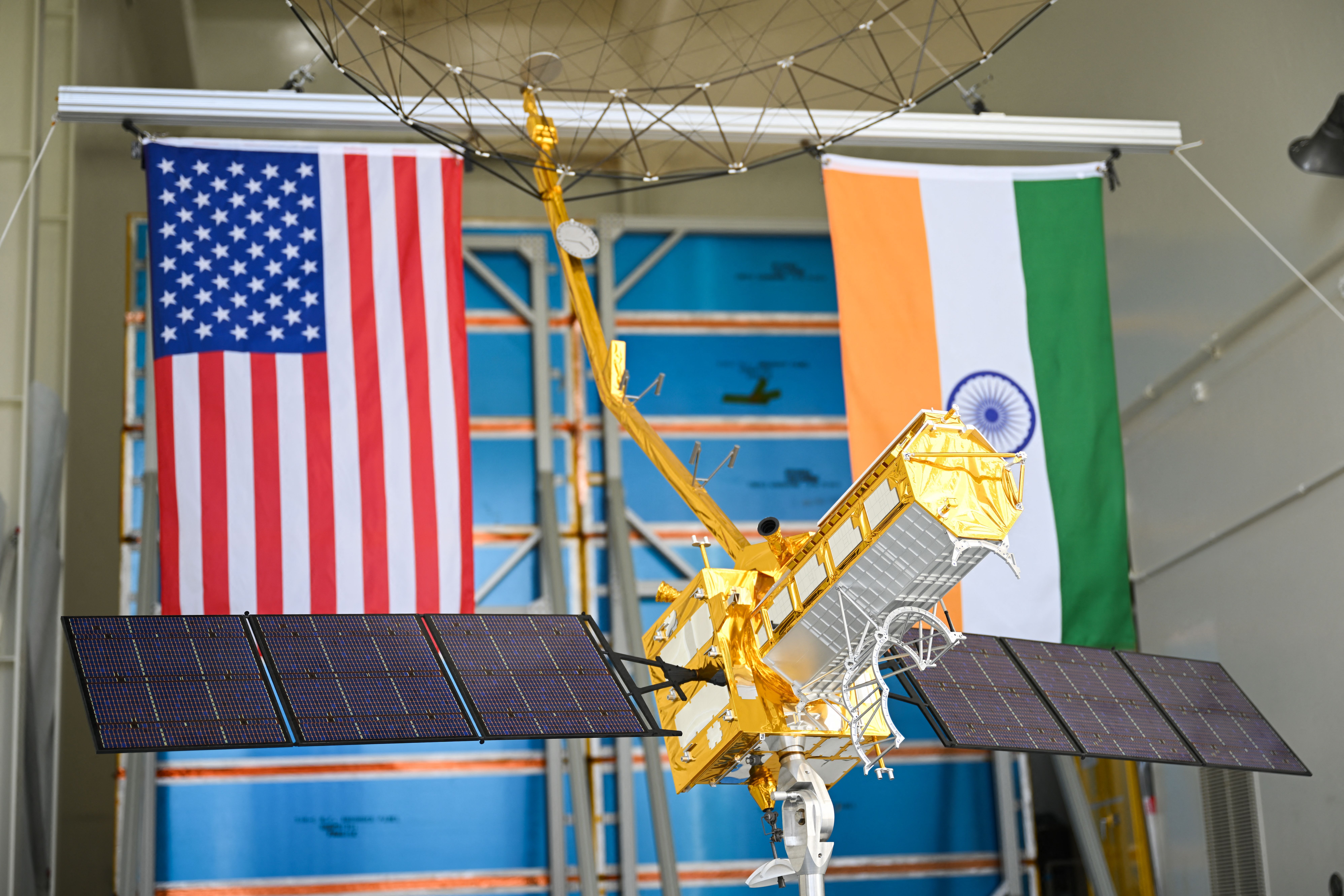

On July 30, 2025, the United States announced 25 percent tariffs on Indian goods. While diplomatic tensions simmered on the trade front, a cosmic calm prevailed at the Sriharikota launch range. Officials from NASA and ISRO were preparing to launch an engineering marvel into space—the NASA-ISRO Synthetic Aperture Radar (NISAR), marking a significant milestone in the India-U.S. bilateral partnership.

Tejas Bharadwaj