Commentary

In the latest Five-Year Plan, the Chinese president cements the shift to an innovation-driven economy over a consumption-driven one.

Damien Ma

{

"authors": [

"Uri Dadush",

"Moisés Naím"

],

"type": "legacyinthemedia",

"centerAffiliationAll": "",

"centers": [

"Carnegie Endowment for International Peace",

"Carnegie Europe"

],

"collections": [

"Brexit and UK Politics"

],

"englishNewsletterAll": "",

"nonEnglishNewsletterAll": "",

"primaryCenter": "Carnegie Endowment for International Peace",

"programAffiliation": "",

"programs": [],

"projects": [],

"regions": [

"Western Europe",

"United Kingdom",

"France",

"Germany",

"Europe",

"North America"

],

"topics": [

"Economy"

]

}

Source: Getty

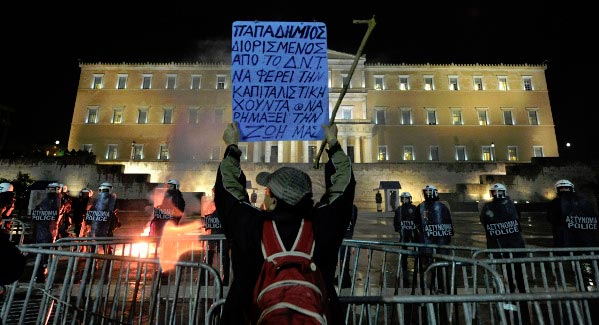

As the Euro crisis continues to play out in Greece and other weak Euro area members, the time has come for policy makers to consider moderately raising their inflation targets.

Source: Financial Times

What happens in Greece will not stay in Greece. Even though the country accounts for only 0.5 per cent of the world's economy, the crash of that profligate nation will have global consequences. The financial irradiation from Greece may be the biggest threat so far to the euro and, indeed, to the European project.

Too much spending, too little tax-collecting and book-cooking are at the core of Greece's troubles. But this is not the entire story: Spain and Ireland are in trouble even though their public debt as a percentage of gross domestic product is much smaller than that of Germany. Italy, also in the financial markets' crosshairs, has high public debt but a lower deficit than the eurozone's average. Good fiscal management did not inoculate Spain against mass unemployment.

At the root of these countries' problems is the fact that their prices and wages have risen much faster than those of Germany and other eurozone members. This loss of competitiveness can no longer be compensated for by currency devaluation. Property bubbles in Ireland and Spain contributed to the troubles. Wage pressure and rigid labour laws across most of these countries did not help either.

IMGXYZ4385IMGZYXSince abandoning the euro looks, at least for now, unthinkable, these countries risk years of wage and budget cuts with anaemic growth, high unemployment and deflation.

There are ways to mitigate the pain. For example, Germany and other countries could adopt more expansionary fiscal policies for a while. Or, more powerfully, the wider euro area could adopt more expansionary monetary policies for several years. Today, this second option is anathema as the "inflation fundamentalists" will have none of it. This elite of central bankers, top economic officials, politicians, academics and journalists maintains the risks of allowing inflation to climb above 2 per cent are unacceptable.

Their view is informed by the disastrous experience with hyperinflation in Germany in the 1930s and stagflation in industrial countries in the 1970s and 1980s. Undoubtedly, moderate inflation can creep up to become high inflation. But, like many good ideas that take on the mantle of a cult, inflation fundamentalism can hurt. There is little if any empirical evidence that moderate inflation that stays moderate hurts growth. In most countries, cutting actual wages is politically difficult if not altogether impossible. But, to regain competitiveness and balance the books, real wage adjustments are sometimes inevitable. A slightly higher level of inflation allows for this painful adjustment with a lower level of political conflict.

Ultra-low inflation, on the other hand, can easily become deflation in a recession. Falling prices encourage people to defer spending, which makes things worse and erodes tax payments, impairing a government's ability to service debt, which in turn increases the debt's size and costs.

The harms of inflation fundamentalism do not stop there. A single-minded focus on inflation makes it easy for policymakers to lose sight of the broader picture - asset prices, growth and employment. Policy can become too tight or too loose - as in the run-up to the crisis in the US when low inflation was seen as a comforting sign that things were in order.

Very low inflation also reduces the effectiveness of monetary policy when growth slows since interest rates cannot go below zero. In the current crisis, governments were forced to rely too much on fiscal stimulus, and central banks to buy securities directly, taking on more risk themselves, and distorting financial markets.

The crisis in the euro area underscores the need for a more open-minded discussion of the merits and costs of ultra-low inflation, and Olivier Blanchard, the IMF's chief economist, has just called for consideration of a more moderate (4 per cent) inflation target. This took courage. Coming from what was once the temple of inflation fundamentalism, it is akin to the chief rabbi calling for reconsideration of kosher laws.

The reaction of members of the European Central Bank council to Mr Blanchard's proposal? "Playing with fire", "extremely unhelpful" and even "a satanic error". The euro crisis and the dismissive reaction to a proposal from a respected source are sure signs that the time for serious scrutiny of inflation fundamentalism has come.

Uri Dadush is a senior associate in and the director of Carnegie’s International Economics Program. Moises Naim is the editor-in-chief of Foreign Policy magazine.

Former Senior Associate, International Economics Program

Dadush was a senior associate at the Carnegie Endowment for International Peace. He focuses on trends in the global economy and is currently tracking developments in the eurozone crisis.

Distinguished Fellow

Moisés Naím is a distinguished fellow at the Carnegie Endowment for International Peace, a best-selling author, and an internationally syndicated columnist.

Carnegie does not take institutional positions on public policy issues; the views represented herein are those of the author(s) and do not necessarily reflect the views of Carnegie, its staff, or its trustees.

In the latest Five-Year Plan, the Chinese president cements the shift to an innovation-driven economy over a consumption-driven one.

Damien Ma

Rather than climate ambitions, compatibility with investment and exports is why China supports both green and high-emission technologies.

Mathias Larsen

“Involution” is a new word for an old problem, and without a very different set of policies to rein it in, it is a problem that is likely to persist.

Michael Pettis

While China's investment story seems contradictory from the outside, the real answers to Beijing's high-quality growth ambitions are hiding in plain sight across the nation's cities.

Yuhan Zhang

China's stimulus addiction cannot go on forever. Beijing still has policy space to clean up the country's massive debt issue, but time is running short.

Michael Pettis