Commentary

Sergey Vakulenko

{

"authors": [

"Sergey Vakulenko"

],

"type": "commentary",

"blog": "Carnegie Politika",

"centerAffiliationAll": "",

"centers": [

"Carnegie Endowment for International Peace",

"Carnegie Russia Eurasia Center"

],

"englishNewsletterAll": "",

"nonEnglishNewsletterAll": "",

"primaryCenter": "Carnegie Russia Eurasia Center",

"programAffiliation": "",

"programs": [],

"projects": [],

"regions": [

"Russia"

],

"topics": [

"Trade",

"Energy",

"Economy",

"Climate Change"

]

}

Source: Getty

Vostok Oil is touted as a major greenfield oil project, but it has—so far—focused on building an Arctic port, and a pipeline from the aging Vankor cluster.

Russia’s oil industry enjoyed a renaissance between 2008 and 2018 when about 30 new oil fields came online, significantly boosting production. Almost all the fields were discovered in the Soviet period, but they could not be profitably developed because drilling technology was not sufficiently advanced, and it was too complicated to ship the oil out of such isolated areas.

Now, there is only one project left in Russia that could theoretically offer a significant increase in production: state-owned Rosneft’s Vostok Oil. What does this project involve, how much oil could it produce, and over what timeframe?

Between 2019 and 2021, Rosneft shouted from the rooftops about Vostok Oil, including at international conferences, in publications for shareholders, and in press releases about meetings between company head Igor Sechin and Russian President Vladimir Putin. In company documents, Vostok Oil was said to contain 6 million tonnes (45 billion barrels) of oil, and production was envisaged to be 115 million tonnes a year by 2033 (in other words, 2.3 million barrels a day). As early as 2024, it was supposed to produce 30 million tonnes a year.

A slide from a presentation by Igor Sechin at the XII Eurasian Economic Forum in Verona, Italy, on 24 October 2019, p. 19

Vostok Oil consists of several elements: (i) the Vankor oil field cluster; (ii) a 770-kilometer pipeline heading northeast from the cluster to the the Kara Sea; (iii) the Payakha, Baikalovskoye, and Irkinskoye oil fields on the right bank of the Yenisei River in the south-west of the Taymyr Peninsula; (iv) an under-construction oil terminal at Bukhta Sever (North Bay) on the right bank of the mouth of the Yenisei not far from the town of Dudinka; (v) and areas undergoing geological exploration in eastern Taymyr near Khatanga.

The Vankor cluster is a group of fields in the north-west of Krasnoyarsk krai about 150 kilometers from the town of Igarka. These include the flagship Vankor field, launched in 2009, and the Suzun, Tagul and Lodochnoye fields acquired by Rosneft when it purchased oil major TNK-BP. To bring oil from the Vankor cluster to the market, Rosneft built the Vankor–Purpe pipeline, which goes south-west for about 550 kilometers to link up with state-owned Transneft’s network. From there, it can go to ports on the Baltic, Black Sea and Pacific Ocean.

Vankor reached peak production—22 million tonnes a year (440,000 barrels per day)—in 2016. Since then, production has fallen. Between 2016 and 2022, production began at the Suzun, Tagul and Lodochnoye fields. But, together, the four sites produced just 14.8 million tonnes (about 300,000 barrels per day) in 2023.

In Rosneft company documents, this cluster is now referred to as part of the “new Vostok Oil project”—even though we’re talking about old sites that have long been included in Russia’s official reserves, its production figures, and forecasts for the oil market. There are few other publicly-available details about Vostok Oil, but satellite data gives some sense of its scope. In particular, there is a lot of activity at Bukhta Sever, where images show port buildings, jetties, berths and a tank farm at an advanced stage of construction.

The port’s 16 oil storage tanks each have a capacity of 30,000 cubic meters, which means the average daily loading capacity could be up to 70,000 tonnes (assuming the standard requirement of 7 days of loading storage). In other words, the terminal is being built to have an annual capacity of 25 million tonnes of oil (or 500,000 barrels a day). Company statements, and the pace of construction, suggest oil shipments could start in the summer of 2026.

However, for shipments to continue year-round, the port would require a fleet of Arc7 ice-class tankers. Given that a return trip to the port of Murmansk takes 15-16 days, the port would need 15 tankers with a deadweight tonnage of 70,000 (the size of the largest Arctic-class tankers currently serving Russian Arctic projects) each to operate at full capacity. Russia does not have that sort of fleet, and only a few Arc7 ice-class tankers are scheduled to be built in the next few years.

But will such a tanker fleet actually be necessary? Rosneft is planning to send oil from the Vankor cluster northwards to Bukhta Sever. But, even in a best-case scenario, the cluster can only provide about half of the port’s 25 million tonne annual capacity. The rest is supposed to come from new fields yet to be brought online: Payakha, Baikalovskoye, and Irkinskoye.

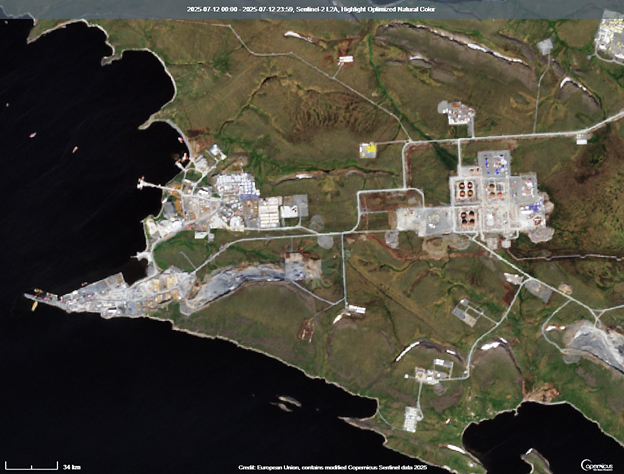

Although Rosneft has not released many details about these sites, satellite data allows us to draw some conclusions. There are four oil fields—Baikalovskoye (located next to the village of Baykalovsk), Payakha, Irkinskoye and West-Irkinskoye—which are likely all part of the same geological structure extending under the Yenisei River near the villages of Mungui, Karaul, and Polikarpovsk. Baikalovskoye used to belong to Yermak Neftegaz, a joint venture between Rosneft and oil major BP that BP exited in 2016. Rosneft acquired Payakha, and Irkinskoye, in 2020 from Independent Oil and Gas Company controlled by former Rosneft head Eduard Khudainatov.

Satellite images suggest that three well pads were built in the summer of 2023 in the Baikalovskoye oil field—but, since then, there has been little progress. This looks like appraisal activity—not early stage development drilling. The situation is similar at Payakha—you can see a few well pads, a site likely slated for an oil processing facility, and some trailers for workers.

Photographs from satellite Sentinel-2 from 13 July, 2025. Copernicus Sentinel data 2025

There is no observable construction activity when it comes to oil processing facilities, which are required to pump crude oil into the pipelines, at either Baikalovskoye, Payakha, or Irkinskoye. It usually takes two to three years to build such facilities even after the equipment and materials are in place. As a reference point, one can look at satellite images of the East-Messoyakhskoe oil-and-gas field in summer 2014, and summer 2017 when it entered production.

East-Messoyakha is an example of oil field development in a period when Russian oil companies had unfettered access to labor, capital and equipment—much different to today when there are problems caused by the war in Ukraine and Western sanctions. Given all this, it is unlikely that any meaningful production could start at the Payakha earlier than 2028.

At the present, Vostok Oil has effectively been reduced to the construction of a transport system to ship oil from the Vankor cluster via a port on the Kara Sea. But there’s actually no need for such a transport network: existing pipelines already allow for oil to be moved out of the Vankor cluster (and there’s no chance of production growth, or these pipeline’s having their capacity restricted).

The Payakha cluster is approximately halfway between the Suzun field, which is the northernmost field of the Vankor cluster (meaning it is connected to the existing pipeline network), and the newly-built oil terminal at Bukhta Sever in the far north. The network including the Arctic port has apparently been designed to accommodate additional oil volumes from the Payakha cluster—but construction has fallen seriously behind the schedule that was announced 5 years ago.

But why does Rosneft need to connect Payakha to the terminal? Why does it need the terminal? Why couldn’t Rosneft just build a pipeline connecting the Payakha and Vankor clusters, and ship Payakha’s oil south into Transneft’s network? The answer is not immediately obvious.

In fact, what we have is something of a paradox. Generally, developing fields presents no challenges for Russian oil companies—it was moving crude out of remote areas that often posed problems. Thus, the current plans for the development of the Payakha cluster make little sense. While oil export infrastructure is being built at full speed, basic infrastructure at the drilling sites is lacking.

There are several possible explanations. Firstly, Rosneft may be under financial pressures that mean it has to develop the project sequentially. However, if that’s the case, it would be logical to create a temporary export route via Vankor, start producing via Vankor—and only then complete the northern route.

Secondly, it could be that geological exploration after the fanfare of the initial announcement of the project yielded disappointing results—and a major development began to look loss-making.

Thirdly, perhaps the main purpose of the project was always to establish an oil export facility on the Arctic Ocean. Amid the stand-off between Russia and the West after the full-scale invasion of Ukraine—and the risks that Russian oil could be blocked from moving out of both the Baltic Sea and the Black Sea—there is an some strategic rationale for such an undertaking. However, the value of Bukhta Sever as an oil export outlet is limited because Russia only has a few of the ice-class tankers capable of transporting the oil all year round.

There is one final possible explanation, which has nothing to do with business or strategy, but is rooted in the Byzantine nature of Kremlin politics: the dynamic between Sechin, and the head of Transneft, Nikolai Tokarev. Both men are close to Putin, and they have a difficult—if not openly hostile—relationship that is reflected in the relationship between their two companies. So, Rosneft’s desire to deprive Transneft of oil volumes might be the reason for the peculiar way in which Vostok Oil is being developed.

Either way, we can confidently state that Vostok Oil will not be producing any significant new quantities of oil over the next five years. Judging from the pace of construction, and the scale of the work at Bukhta Sever, even at its peak, production from the Payakha cluster will likely be less than 15 million tonnes a year (300,000 barrels a day). And such a production level could only be reached between five and seven years after full-scale development got underway. It’s clear that the initial plans for Vostok Oil were vastly over-ambitious.

Senior Fellow, Carnegie Russia Eurasia Center

Sergey Vakulenko is a senior fellow at the Carnegie Russia Eurasia Center.

Recent Work

Sergey Vakulenko

Sergey Vakulenko

Carnegie does not take institutional positions on public policy issues; the views represented herein are those of the author(s) and do not necessarily reflect the views of Carnegie, its staff, or its trustees.

Andrey Melnichenko’s essay offers no answer to the fundamental question of how, under any kind of negotiated settlement, Europe can protect itself from the Russian ressentiment that is inevitable in all scenarios except for an outright victory for Putin.

Leonid Bershidsky

Despite unhappiness on the ground, Moscow is determined to use both carrot and stick to ensure there is record support for United Russia in occupied Ukraine.

Konstantin Skorkin

Medvedev’s defeat in the battle for the position of speaker appears to signal that the long process of his marginalization in Russian politics has passed the point of no return.

Andrey Pertsev

The recent damage inflicted by Ukrainian drones and missiles on Russia has made Belarus aware of its own vulnerabilities—and surprisingly amenable to Kyiv’s demands.

Artyom Shraibman

With its scattershot approach to enforcing internet censorship, the Russian regime risks losing a battle against the many Russians who have learned to evade online restrictions.

Maria Kolomychenko