Commentary

As we close out another season of Strategic Europe, it is worth taking stock of the deep shifts underway.

Rym Momtaz

Source: Getty

Europe’s industrial supply chains leave it vulnerable to global shocks. The EU needs a pragmatic green industrial strategy that balances durable partnerships and bolsters homegrown clean tech without sacrificing low-carbon ambition.

Europe needs a pragmatic clean industrial strategy and external action to match. In an era of fuel shocks, supply chain chokepoints, and brute transactionalism, business-as-usual frameworks built on climate altruism or free-trader assumptions are no longer sufficient. A realist approach to industrial and foreign policy need not come at the expense of low-carbon ambitions or durable cooperation with partners, but it does require a coherent, focused agenda to stimulate exports where feasible, secure the most vulnerable supply chains, and bolster European clean technology at home and abroad. This paper draws on a year of internal analysis and workshops with European policy planners, diplomats, and European Commission officials. It assesses Europe’s industrial base across clean tech and industrial supply chains, evaluates past diplomatic efforts by the European Union (EU) and its member states on climate and clean tech, and prescribes policy ideas that balance development and decarbonization with the imperatives of security and competitiveness.

Europe’s energy and foreign policies are not yet suited to today’s harsh geopolitical environment. Since the 2019 European Green Deal, the European Union (EU) has cut emissions by reducing fossil fuel consumption. But it has created new dependencies by swapping them for energy technologies and imported fuels.1 The rise of China—and now the United States—as competing state-capitalist poles has challenged the EU’s free market–based energy and industrial models.2 Europe now sits between two energy hegemons, consuming over half of U.S. liquefied natural gas (LNG) exports and Chinese clean technology exports (see figure 1). These dependencies pose distinct risks: LNG exposure is immediate and vulnerable to shocks, while clean tech dependence is long term and carries risks of industrial coercion and cyber vulnerabilities.3 The remedies to both, however, point in the same direction: electrify as much of the European economy as possible using clean energy produced from secure and, where necessary, domestic inputs.4

Europe will need a clear vision of its own clean industrial ambitions, including an attractive external offering to counter the U.S.-Chinese power competition. China is now an established actor in the Global South, deploying finance at scale, while the United States has adopted a transactional approach to secure resources.5 In the past, Europe has projected its values of sustainable stewardship on third countries and, in the context of energy policy, primarily focused on assisting in the reduction of carbon emissions.6 While this should remain an aim of its Global South engagement, the EU might take a new approach that better serves and aligns with its own priorities: insulating itself from hydrocarbon shocks and carving niches in value-add alternatives for clean tech production. What Europe can and should offer third countries are focused, concrete opportunities to access its remaining electrification equipment (especially the power grid), develop mutually beneficial supply chains, and collaborate on innovation for low-carbon breakthroughs with competitiveness and security dividends. Doing so will ensure that Europe’s low-carbon industry remains fruitful—an essential development for a durable, long-term energy transition.

Europe’s outlook includes notable vulnerabilities and legacy strengths. To gauge this, domestic manufacturing capacity potential for 2030 is harmonized against projected demand in what should be viewed as a best-case scenario where new projects with established start dates are actualized, those without closure dates remain online, and demand remains within the bounds of consensus growth (see figure 2). The UK, Norway, and Switzerland are included alongside the twenty-seven member states of the EU. In this scenario, Europe can domestically produce about 25 percent of permanent magnet materials—essential to electric vehicles (EVs) and offshore wind turbines—and 65 percent of battery cells, but far fewer cathodes and just 5 percent of the anodes it requires. Solar photovoltaic (PV) production remains limited at about 10 percent of core inputs, while offshore wind is slightly undersupplied from domestic production, and onshore wind remains a strong industrial base capable of meeting demand with potential exports. Similarly, grid tech—solar inverters, transformers, switchgears, and cables—will remain well supplied with the continued potential for some exports. Nuclear fuels are likely to come close to self-sufficiency, while geothermal turbine production will yield a comically large supply-demand ratio of 1,485 percent because Europe is the world’s leading supplier with inconsequential demand. Lastly, if heat pump and electrolyzer factories are developed at pace, they risk oversupply due to weak or unclear domestic demand.

Critical raw materials (CRMs) and industrial products also yield varying strengths (like recycled copper and aluminum) and weaknesses (like graphite and rare earths) (see figure 3). Mined and especially processed lithium represents a potential opportunity with significant projects in the pipeline that could deliver domestic production, including via recycling. However, mined nickel and cobalt remain in very small supply at about 5 to 10 percent of demand with little growth opportunities. Graphite—including flake, synthetic, and processed materials—is a severe vulnerability with few potential projects producing, at best, 5 percent of projected demand. Most concerningly, Europe has zero rare earth mines that can be activated by 2030. That said, a surprising scale of rare earth processing could be developed—even for heavy rare earths—if adequate rare earth mineral inputs can be sourced. Copper and aluminum are bright spots: While only copper is mined in notable but modest quantities, Europe’s recycling capacity for both is immense. It can, in theory, produce nearly 50 percent and 30 percent of aluminum and copper supply, respectively. However, Europe’s scrap is susceptible to export leakage and does not guarantee production.7

Heavy industry presents a unique challenge. Decarbonization of this sector is inflationary and energy intensive—an unfortunate reality as European industry faces a second China shock and an additional energy crisis.8 If all clean steel projects start on time, most of Europe’s steel production will come from low-carbon electric arc furnaces (EAFs) and not coal-based blast furnaces. But this switch will create two obstacles: The first is that Europe will be significantly undersupplied in green iron ore (about an 80 percent deficit). The second is that EAF steel cannot fully substitute the quality of blast furnace steel, especially in strategic applications because of its lower purity.9 Notable progress is possible on green ammonia, which is essential to fertilizer production, including potential imports of clean ammonia. However, most domestic hydrogen production will remain fossil-based and exposed to gas imports. Europe can reach its goal of 6 percent sustainable aviation fuel (SAF) production, but it remains exposed to kerosene imports and might struggle to build SAF production because while much of the pipeline today is cheaper, biofuel-based solutions, this will eventually require far costlier synthetic fuels.10

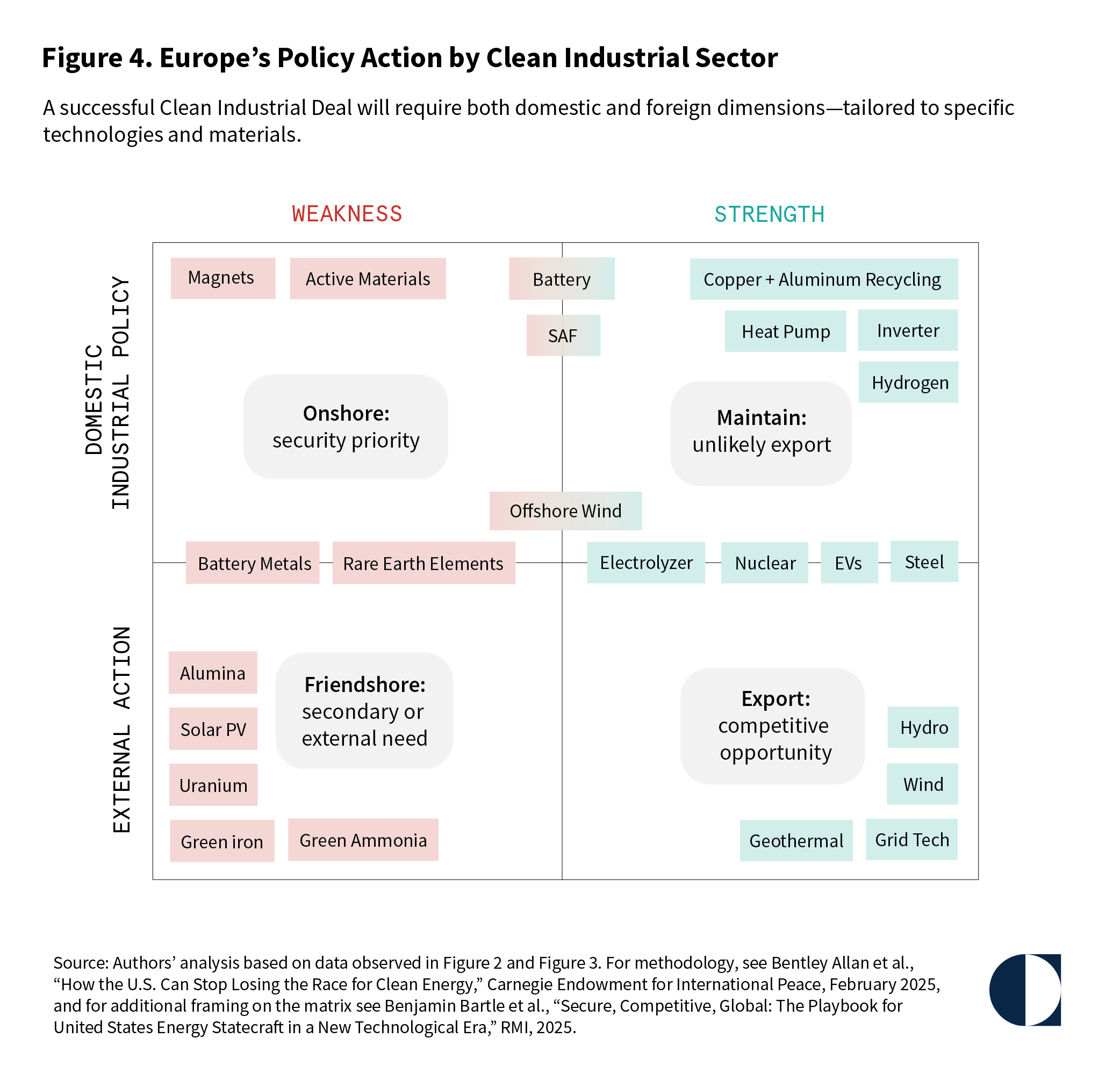

Not all strengths and weaknesses are created equally, however. Some strong sectors pose opportunities for export, while some weakness will require onshoring due to economic security risks (see figure 4). The matrix listed below can help policymakers conceptualize these sectors. Grid tech, geothermal turbines, and wind turbines present clear opportunities for both domestic use and export or foreign operation plays. We emphasize that these technologies—especially grid hardware—are strengths that Europe should double down on. Conversely, rare earth magnets and lithium-ion batteries will, at least to some extent, require onshoring due to their dual-use applications.11 Similarly, jet fuel and power electronics carry security risks, pointing to domestic production.12 CRMs, on the other hand, will require both onshoring and friendshoring (bringing production to trusted partner countries) because of limitations to mining in Europe. Other sectors that pose unlikely export opportunities—like heat pumps and hydrogen—can be left to maintain, while electrolyzers, steel, and electric vehicles all have some export potential but face fierce competition against Chinese products.13 Some components (like green iron ore) or hardware (like solar panels) do not pose immediate security risks and might be friendshored or traded freely.14

The EU needs a policy ecosystem that incubates and protects domestic industry where necessary. As demonstrated in the previous section, Europe has a strong pipeline of projects, but many will struggle to scale up and reach market without targeted support. The recently tabled Industrial Accelerator Act (IAA) introduces some important tools—its local content provisions are an especially useful starting point—but the current requirements are insufficient to deliver genuine impact, and the broad geographical scope of EU-origin eligibility creates a significant circumvention risk.15 The IAA’s local content requirements include a loophole: if EU products are more costly than a certain price range to foreign products, the requirements don’t apply. These weak and undifferentiated rules send poor investment signals and, more worryingly, may lead to the IAA’s nonapplication across sectors because Chinese firms can dump into the single market to depress prices below this threshold.16 Solutions to this challenge might include increasing the price threshold across the board or designing sector-specific thresholds that preemptively reflect current and future EU-China cost gaps.

Going forward, the EU will need focused and effective state-aid measures. First, Europe’s clean tech sector would benefit from moving from project-level, lump-sum allocations to bankable, output-based support.17 These so-called ramp-up incentives—which might provide time-limited subsidies in early development—can help mines, processing plants, and downstream factories weather initial losses amid cheap Chinese imports.18 Such incentives should be timebound and coordinated by the EU to prevent rent-seeking and intra-EU subsidy races.19 Looking ahead, the next Multiannual Financial Framework and the proposed European Competitiveness Fund will need to scale up and surgically spend resources—including grants, guarantees, and low-interest loans—on strategic clean technologies.20 This funding should focus on closing the gap for private investment. It should prioritize technologies where a strong industrial base is essential for the bloc’s security—namely magnets and batteries—and where Europe can scale competitive industries, like grid tech, turbines, and wind through existing incumbents.

Europe should continue to embrace targeted yet nuanced trade and cyber-related protectionism. Chinese overcapacity is accelerating and could cut further into European production, while Beijing has already weaponized critical chokepoints.21 First, Europe might explore a sequenced trade policy starting with sector-specific safeguards and quotas on some Chinese goods where Europe has an industrial base like wind or metals. This more-calibrated move may limit the potential for retaliation. Second, Europe needs to secure its scrap metals and prevent leakage so that they can be recycled domestically. Exports of some strategic secondary materials have grown sharply in recent years (see figure 5), representing a significant loss of potentially recyclable inputs for European industry. Ensuring that valuable scrap metal and e-waste stay in the single market might require the enforcement of existing EU regulations, but Europe also might explore more aggressive measures like export restrictions and subsidies to scale-up recycling capacity in new areas beyond copper and aluminum (or even fund scrap stockpiles).22 Lastly, as Europe electrifies, it needs to do so with cyber hygiene. European-made power electronics offer a durable long-term solution, and Europe’s domestic base is mature.23 The recent ban on EU funding for Chinese inverters is a meaningful first step but, going forward, more stringent measures might be phased in, like those outlined in the EU’s proposed cybersecurity framework, to sufficiently remediate these risks.24

Simultaneously, the EU has begun to spur efforts to internationalize green industrial policy, as evidenced by specific projects under the Global Gateway, the promise of preferential purchasing by the forthcoming CRM Centre, and the first-of-its-kind Clean Trade and Investment Partnership (CTIP) agreement with South Africa.25 However, critical questions remain about whether Europe has the tools necessary to invest in strategic projects abroad. As the United States has begun investing government equity into projects and offering price floors, the EU should actively pursue how it might replicate such powerful forms of foreign project finance that help provide investor confidence, regardless of mineral market volatility.26 Its partnership with the Japan Organization for Metals and Energy Security (JOGMEC) is a welcome first step toward developing similar tools and transferring such knowledge, but this will take time.27 Finally, the European Investment Bank’s (EIB’s) new global strategy goes in the right direction by committing to increase capital efficiency, leveraging EU companies, and proposing to support European export credit agencies. How this will translate into benefits for EU clean tech competitiveness, however, remains to be seen.28

Over the past decades, the European External Action Service (EEAS) and member state missions have built out partnerships and pacts that center around climate and clean energy.29 However, the ethos of such partnerships is both generally broad in scope and, when focused, more tailored to joint goals of capacity building—not market shaping.30 Going forward, Europe will need to embrace a more utilitarian and business-oriented external posture, prioritizing projects that serve both partners’ development priorities and the EU’s industrial or resilience goals (ideally both). Fortunately, much of the initial diplomatic architecture has already been built through myriad memorandums of understanding (MOUs), green pacts, and broader bilateral and minilateral agreements (including member state cooperation through Team Europe Initiatives). Europe should take stock of these feats and transform past diplomatic success into future industrial action.

Europe’s clean tech external action spans over sixty countries and nearly 300 pacts. Publicly available data shows EU and member state engagements ranging from broad clean energy partnerships (for example, Energy Partnerships and Just Energy Transition Partnerships) to sector-specific agreements on minerals, renewables, hydrogen, and nuclear. These engagements are particularly concentrated in Morocco, India, Canada, and the UK (see figure 6). Other highly engaged partners include Australia, Tunisia, South Africa, Japan, Norway, and Egypt, as well as several Eurasian countries including Kazakhstan and Uzbekistan. These markets are strong candidates for deeper cooperation given existing diplomatic inroads. The analysis also reflects bilateral initiatives by key member states. Germany’s footprint is by far the largest, rivaling the EU’s at about eighty agreements. France, Italy, and Denmark have each entered into roughly thirty agreements. Germany is heavily focused on hydrogen (largely though its Federal Foreign Office’s H2-diplo program), while Denmark has emphasized renewables and France has prioritized nuclear and minerals.

In past years, Europe’s external action for clean tech supply chains has overwhelmingly focused, for better or worse, on CRMs and hydrogen. On the bright side, diplomatic overtures for raw materials are a necessary bet—Europe’s domestic mining outlook is bearish, recycling is ultra long-term, and the hegemons in Beijing and Washington are scrambling for CRM access.31 So far, the EU and member states have sealed sixty-five CRM-related pacts with about thirty countries—notably Canada (including Quebec), Norway, India, Australia, Uzbekistan, and Chile (see figure 7). The EU currently has backed twelve CRM projects at very preliminary stages of development in some of these countries. Other highly engaged nations that do not have specifically government-backed projects—like India, Australia, and Chile—present new opportunity. Most interesting is the development of enabling infrastructure to activate CRM flows, like the Trans-Caspian International Transport Route from Southeast Asia and China, the Lobito Corridor in Central Africa, or port-side export terminals in Namibia.

These CRM infrastructure projects would, in varying degrees, help secure Europe’s supplies and should be prioritized (see figure 8). It is essential that the EU and especially its member states with active foreign development finance institutions act quickly on supporting these projects to market. When including potential friendshored CRMs in analysis of projected 2030 supply-demand, the security of supply outlook for graphite and rare earths notably increases. Although none of these foreign projects are likely to come online by this time and they remain significantly behind domestic mines and processing facilities, this benchmarking helps gauge the scale of their impact. Most important is South Africa’s rare earth extraction and processing facility, which could fulfill about one-fifth of European demand (including for heavy rare earths). Graphite plays in Madagascar, Kazakhstan, and Greenland could contribute 19 percent of demand (another project in Ukraine remains frozen until Russia’s aggression ends). Nickel production in Brazil and Canada—as well as cobalt production in the latter—are important diversification bases to build from, but their contribution will be marginal.

Compared to CRMs, the EU and its member states have nearly twice as many hydrogen pacts with even more countries. This is an inefficient use of diplomatic capital given the relative nicheness of clean hydrogen applications.32 Although many of these pacts have not yielded tangible projects, some important industrial successes are emerging, including green ammonia and iron in Brazil and Namibia (see figure 9). Other markets with numerous European hydrogen pacts—such as India, Oman, and Saudi Arabia—are developing clean ammonia corridor projects that are gaining momentum organically, although the EU has not yet matched their efforts with funding.33 In several cases, European corporates (and ports) have acted as first movers, providing offtake agreements or project finance to signal commitment to buying and building hydrogen projects.34 Still, despite these advances, the clean hydrogen market faces headwinds from high costs.35 The EU and its member states should be more selective going forward: Not every country needs hydrogen, and some analysis suggests Europe’s push for electrolytic buildout across Africa risks absorbing scarce clean electrons in energy-poor regions.36 Where green molecules do make sense, European hardware is essential—and could help absorb potential oversupply if a domestic electrolyzer glut materializes.

Going forward, Europe will need to update its priorities and tools to shape partner goals to its best interests.37 This section breaks down an external action framework into four specific parts: an external strategy for exports and supporting European factories abroad where the EU has technical leadership; bilateral priorities for supply chain cooperation; third-country access to the single market; and science diplomacy as a tool for developing collaborative innovation efforts. These are not exhaustive pillars of a realist—yet decarbonized—external industrial agenda, but they are achievable and can be realized in tandem with the bloc’s commitment to global development.

The EU and its member states should consider tailoring foreign projects to bolster European products. This would include those promoted under the Global Gateway to specify that they are developed by European-based firms and procure European-made hardware, whether through exports or manufacturing hubs in the region. This might entail focusing the Global Gateway, the upcoming Global Europe instrument, and Team Europe Initiatives on projects that procure European grid technologies and electrolyzers, as well as wind, hydro, and geothermal turbines. Projects also using European steel for construction would be welcome. Doing so will limit the scope and scale of what is feasible, but it is an important demand-pull to ensure that European external action and development finance operates in the best interest of industry amid an ever-growing flood of Chinese exports and competition across all energy tech sectors.

So far, Europe’s clean energy project development in the Global Gateway has prioritized solar over wind, negates geothermal projects, and has a sizeable grid base to build from (see figure 10). Twenty-six significant projects include solar PV, while just sixteen projects include wind power. Some include both. While hydro and wind power projects remain at parity with each other, geothermal projects are almost negligible—just one in Kenya and one in Ethiopia. While there are more than thirty-three grid-related projects, just eighteen are grid specific. The others are co-located with large solar or wind farms. Many of these projects include the modernization and expansion of large regional or national transmission lines, including with the high-voltage direct current system that has been mastered by EU industry. This is the case in, for example, West and Central Africa as well as interconnections through the Mediterranean. The number of hydrogen projects—largely backed by Germany, which has emphasized this vertical—is similar to wind and hydro.

A global grid initiative—through which Europe accelerates electricity infrastructure abroad—would be a powerful central political offering. It would advance the bloc’s development commitments, project Europe’s model as an electro-state, and support core clean tech strength. Here, the Global Gateway offers a strong foundation to expand upon including supporting the development of European-owned grid tech factories in countries facing or nearing high, long-term growth in power demand. Conversely, Europe’s concentration on solar PV, while practical given the low cost and ease of construction, risks directly benefitting Chinese rather than European industry.38 The global solar trade is essentially cornered by China, whose firms can increasingly self-finance or rely on private development funds. (One exception might be maintaining support for microgrids in least-developed nations, where solar PV is an essential lifeline to electricity.)39 The EU should reprioritize its utility-scale solar project resources to wind, where its edge is slipping, and to defend European industry, especially in Mercosur countries (Argentina, Brazil, Paraguay, Uruguay, and Bolivia) and potentially India, against Chinese competition.

While the EU and its member states should continue financing hydro, they should shift some of their attention to geothermal. Its growth market is potentially larger, and Europe retains an industrial niche worth defending.40 That will require internationalizing innovative financing tools to de-risk drilling, perhaps similar to models already used by Germany’s state-owned development bank (KfW) and reinsurance sector.41 The EU should also build on France’s recent pact with Kenya to expand geothermal developments into Zambia and other neighboring countries like Tanzania.42 Lastly, Europe should remain active—but realist—in green hydrogen, focusing on viable projects and high-value derivatives, especially ammonia-based fertilizers, which can strengthen food security in an era of price shocks and record El Niño weather.43 Other projects might specify green methanol or iron to help jurisdictions with existing industrial demand decarbonize.

Reforming the EIB’s tendering process and developing greater levels of European diplomacy for its business interests might help fully activate this external agenda. EIB procurement procedures are open to all bidders, awarded to the most economically advantageous tender, and largely aligned with member state development banks.44 However, given the significant and increasing cost advantage, there is a high risk that contracts will be awarded to Chinese clean tech hardware—even in strengths like wind or grid tech.45 Reforming the bank’s procurement rules can help ensure that European public funds do not finance competing companies. Concurrently, the EIB has committed to supporting Europe’s private sector, notably by financing international bids through guarantees as well as exploring support for export credit agencies.46 These are important tools that can also aid European industries abroad and, coupled with tendering procedures that include an option for European preference, would help bolster Europe’s exports.

One optimal strategy might be to find projects where European energy hardware can be deployed to enable local economic development and produce strategic inputs for European industrial needs—a win-win situation. Today, CRM-rich developing countries rightly seek midstream industry, but refining minerals into battery-grade chemicals is energy and water intensive, can cause environmental issues, and offers little price advantage over processed concentrate, which might mostly remain the priority to Europe (especially in third countries with weak governance standards).47 Even so, mining and beneficiation will still require electricity and Europe should target power infrastructure in its partnership offers. For example, the EIB and the French Development Agency have backed a project in San Juan, Argentina, to build out the regional grid near the site of a French mining company’s lithium production.48 If this project was built with European hardware, it would check all the necessary boxes: bringing power to the region, supporting diversified CRMs, and buying European goods in the process.

The EU can also fund niches of clean tech manufacturing, as it has been doing with hydrogen facilities, in countries optimal for de-risking. The administration of U.S. president Joe Biden began financing Indian solar factories as a way to de-risk from China—but also to empower India’s green industrial base.49 As part of the global grid initiative idea, Europe might also support its grid hardware companies to develop manufacturing hubs in third countries near high electricity growth. This would both offer jobs abroad and increase the market share of European firms, which will need to expand their capacity amid surging power demand and booked-out orders.50 Similarly, much attention has been given to so-called powershoring, wherein green iron might be produced in countries like Brazil or Namibia to feed European steel production.51 In an era of more precarious global trade, policymakers might consider nearshoring some of these more strategic products in countries like Turkey or Morocco to ensure that a force majeure event would not risk these supplies.52

In the medium term, Europe might find itself with additional solutions that it can offer third countries. Its foreign policy must be ready to adapt. One critical area might be the decarbonization of industrial heat. European firms are leading on myriad solutions like thermal energy storage, high-capacity heat pumps, waste heat use, and direct-use geothermal.53 Given today’s fuel precarity, this vertical may emerge as a new offering that Europe can share with partners, especially fellow fossil-fuel importers interested in electrifying and insulating their industries. Similarly, Europe’s offshore wind sector might be an area to support once it recovers from the chaos of the United States’ shifting policies. Future markets could include Brazil, Japan, South Korea, and potentially Australia.54

Europe needs a focused, tailored approach to bolstering key niches of interest with partner countries. Future diplomatic engagement, including bilateral discussions between leadership, should be ultra clear and selective about key pillars of focus. Instead of an MOU for CRMs, the dialogue might specify, for example, graphite. The more specific it is, the clearer the expectations will be on both sides. For example, French President Emanuel Macron went to Mongolia in 2023 to advocate for a uranium mine; two years later, the two sides reached an investment agreement.55 A broader template for this was outlined in the novel CTIP agreement with South Africa.56 CTIPs seek to streamline intra-ministerial pacts under one roof and offer a menu of clean energy sectors for governments and industry to jointly develop.57 That said, discussions with policymakers revealed that cumbersome intra-EU dynamics are a challenge to the promise of timely movement. Written six months since the first CTIP was announced with no sign of follow-up, the European Commission should focus on seeing the South Africa agreement through before expanding the pact to other nations.

Based on analysis of Europe’s supply chain and country pacts, there are clear potential updates to existing partnerships that would identify critical opportunities for export promotion, supply chain incubation, and strategic investment inflows (see figure 11). India, for example, is a priority given the free-trade agreement (FTA) negotiations and existing pacts with Europe, its de-risking value vis-à-vis China, and its outsized role in global emissions.58 The EU and its member states should use this moment to strengthen European wind industry by mandating that the remaining original equipment manufacturers power EU-backed clean industrial projects. Those projects also offer a platform to promote Europe’s emerging industrial electrification solutions.59 On supply chains, Europe could support India’s solar manufacturing base, which is on track to become second to China but is hampered by missing inputs like ingots and wafers currently dominated by Chinese firms. Bolstering this would help diversify supply of the world’s fastest-growing energy source.60 Finally, while India has begun developing green ammonia corridors into Europe, this momentum could be leveraged for green iron projects that simultaneously decarbonize India’s steel sector and secure European access to low-carbon inputs.61

Other countries call for different types of agreements. Japan and South Korea are energy- and mineral-poor but host some of the only corporate capacity outside China that can produce sintered permanent magnets and battery active materials.62 Given the extreme vulnerabilities in both supply chains, encouraging these countries to support their firms to manufacture within Europe is a sound bet. Similarly, nuclear-friendly member states might join forces on opportunities, especially with Canada, to partner on more CANDU reactors in Europe (which do not require more enrichment and thus simplify Europe’s fuel security).63 Brazil and Canada already host EU-backed nickel-cobalt projects, but this scope should expand to rare earths and graphite alongside downstream processing—both countries have large hydro-based renewable capacity and there is high need to diversify anode material and purify heavy rare earths outside of Europe due to nuclear residuals.64 Finally, an EU-level partnership with Kenya to promote geothermal power across East and Southern Africa would be an enormous win-win—provided it can support European-made turbines.65

This menu is not exhaustive. Some countries may have unique, one-off opportunities. For example, Europe should pursue a geothermal partnership with the United States, where a new drilling revolution is unlocking geothermal as a global power source, with high potential for diffusion in Europe. (Even before that can happen, U.S. geothermal growth will require European turbines.)66 Countries such as Chile, Egypt, Norway, the UK, and Vietnam have already been the focus of notable clean energy pacts and might be explored in a similar fashion. Upstream, this analysis omits some inputs like electrolyzer membranes, heat pump compressors, grain-oriented electrical steel for transformers, gear boxes for wind turbines, and battery cell separators. These are essential but underappreciated chokepoints that merit further de-risking analysis. Research from the Clean Technology Partnerships Initiative offers a deeper dive into potential projects and cost structures.67

Partnerships aimed at sending minerals, materials, or hardware to the EU might benefit from preferential access to European state aid. Project finance alone may not be enough; projects require offtake and, likely, stricter measures to persuade buyers to lock into potentially more expensive supplies. The IAA, which is under negotiation, could be useful if applied bluntly. As drafted, the act grants EU-origin eligibility to third countries with free trade or customs agreements and, for public procurement, to parties to the World Trade Organization Agreement on Government Procurement (see figure 12).68 But with more than eighty active trade agreements, this policy could be exploited by Chinese producers that build in qualifying countries to access the single market without transferring technology to European firms, a core and important IAA goal. The likelihood of this risk is high as the United States experienced similar re-routing maneuvers in Morocco under the Inflation Reduction Act, but it should not deter from market access being used as a diplomatic offering and potent de-risking tool.69

For the IAA to work—and for Europe to avoid exploitation—Brussels will need to set strict rules in the act’s final form and in future delegated acts specifying which third countries qualify for preferential treatment. Under the current proposal, the European Commission can continuously reassess eligible third countries for EU-origin status based on reciprocity and economic security, a powerful lever. It allows the EU to ensure that partner countries genuinely contribute to European value chains rather than serve as transshipment points for Chinese goods. Many countries are at high risk of becoming hotspots for FTA friction due to the preexisting presence of Chinese clean tech manufacturing (see figure 13). To close that loophole, the IAA could require projects in third countries to meet ownership criteria like those applied in the single market, including majority ownership by a European firm. It could also treat companies domiciled in dominant market-share countries—namely China—as equivalent to those countries for the purposes of eligibility. Essentially, this would mean nationality of ownership, not only manufacturing location, would be the determinant.

Preferential public support access could be handled on a case-by-case basis, with eligibility for specific sectors negotiated individually and potentially tied to an investment arrangement to stimulate trade flows. Instead of including all FTA countries by default and only excluding them for lack of reciprocity or supply security risk, the IAA could flip the logic: exclude all non-EU/European Economic Area countries by default, and then grant EU-origin status selectively on either a project- or country-level—for instance, to those that genuinely grant similar market access to EU companies—with the overarching goal of contributing to the EU’s resilience goals. This offering might be wielded as a bargaining chip and provide impetus for corporates to develop these projects.

Europe needs a similarly realist policy on clean energy innovation. The goal should be breakthrough innovations with high opportunity to scale in Europe through related incumbent industries or unlocking technologies with long-term security dividends. Emerging verticals like floating offshore wind, solid-state transformers, and compressed CO2 geothermal turbines can be absorbed by European corporates in the wind, grid, and geothermal space, thus preserving their competitive stature.70 Europe might also focus on systems that can abate present and future vulnerabilities, like electric motors that do not require rare earth magnets or breakthroughs in new energy sources that could reduce reliance on foreign fossil fuels (like geologic hydrogen or, perhaps someday, nuclear fusion).71 Alongside these long-term breakthroughs, process innovations should be bracketed under the same goals of bolstering competitiveness—by lowering manufacturing or material costs—or enhancing resilience.

Science diplomacy offers an effective tool for long-term industrial interests. Europe is a global innovation leader, with Horizon Europe serving as a flagship incubator for advanced technologies—including through partnerships with non-EU countries.72 Beyond that, EU member states also maintain their own technology and innovation attachés abroad to help coordinate joint initiatives. Yet discussions with policymakers revealed that these attachés are fragmented and uncoordinated—a gap that a Team Europe–style approach could remedy by pooling resources and aligning efforts on key opportunities. A critical question for European policymakers regarding joint innovation—and scaling up patents more broadly—is how to best protect European innovations and ensure that they can be scaled in the single market.73 Nonetheless, Europe can approach science diplomacy through two pragmatic lenses:

Europe should focus its science diplomacy on countries producing the highest output of clean tech research and on breakthroughs with resilience dividends (see figure 14). South Korea hosts the most important battery producers outside China, and coordinating with its researchers could help Europe develop key emerging technologies—sodium-ion batteries, in particular, are now commercializing in China and require few, if any, CRMs.74 Australia, with its renewables base and legacy mining sector, is well positioned as a clean metals producer; deeper collaboration could help consolidate its role as a reliable supplier.75 Norway’s importance to European energy, its proximity to the EU, and its abundant renewable resources make it a natural candidate to incubate synthetic fuel innovation.76 The UK leads Europe in nuclear fusion, with multiple projects advancing—EU labs have strong incentives to engage closely in case this long–sought after energy source emerges.77 Finally, Japanese research labs are deeply focused on geologic hydrogen—extracting clean, low-cost molecules directly from the earth—which is an area where collaboration could help European researchers unlock their own resources.78

Europe holds a strong position in grid hardware manufacturing, but new developments are on the horizon—superconductors and solid-state transformers among them. EU-Swiss science diplomacy presents an opportune arrangement to explore these types of systems, given Swiss university and lab excellence and the two actors’ shared industrial strength in this space.79 New Zealand, meanwhile, is committed to unlocking supercritical geothermal—essentially geothermal power’s equivalent to the fusion breakthrough—which could make this energy source cheaper than fossil thermal plants.80 Supporting New Zealand’s efforts would benefit Europe’s own security and decarbonization goals in the very long term by unlocking a new clean power source.81 Canadian researchers, for their part, hold a strong edge in mineral prospecting, a skill that could help Europe identify new deposits of strategic minerals.82 Finally, as argued previously, Europe should deploy its leading research labs to support India in scaling solar PV technologies—ingot and wafer production in particular—as well as emerging technologies like perovskite cells.83

The coming years will bring new challenges amid deepening global fractures. Europe’s role is essential. While unfashionable today, its long-term bets on climate and decarbonization will remain critical for decades to come. Europe thus must retain key value-added, low-carbon industries and work with partner countries to keep those ambitions alive. The EU and its member states have the talent, technology, and market to pull this off—what they need now is coordination, consensus, and focus. The goals identified throughout this paper offer some direction: a strategy to pursue, technologies to back, and key partners to engage. Success may no longer resemble what was envisioned years ago, like Europe developing a battery champion or reclaiming its stature as a leading solar manufacturer. Those were appealing but unrealistic goals. What Europe can do going forward is defend its current strengths while nurturing necessary supply chains and joint innovation with trusted partners. Its success could serve as a template for others seeking to wean themselves off imported fossil fuels—an inspiring prospect in an increasingly precarious world.

The authors would like to thank Erik Jones for his peer review of the report, Debbra Goh and Jonas Goldman for their support in analyzing data, as well as Daniel Helmeci for his execution of Figures 2 and 3, which can be observed in greater detail in forthcoming analysis.

Fellow, Sustainability, Climate, and Geopolitics Program

Milo McBride is a fellow in the Sustainability, Climate, and Geopolitics Program at the Carnegie Endowment for International Peace.

Research Assistant, Carnegie Europe

Pauline Gerard is a research assistant at Carnegie Europe, supporting work on clean technologies, industrial policies, and a foreign policy for the Clean Industrial Deal.

Carnegie does not take institutional positions on public policy issues; the views represented herein are those of the author(s) and do not necessarily reflect the views of Carnegie, its staff, or its trustees.

As we close out another season of Strategic Europe, it is worth taking stock of the deep shifts underway.

Rym Momtaz

The hybrid warfare landscape is evolving rapidly, leaving policymakers without clear strategies. To better inform their work in addressing emerging challenges, governments must dig deeper into the underlying dynamics at play.

Raluca Csernatoni, Alicia Wanless

The EU had to compromise to adopt a twenty-first sanctions package against Russia, exposing growing cracks in the union’s resolve. Is this latest, weaker round worth it to keep pressure on Moscow?

Rym Momtaz, ed.

Trump is distracted and Ukraine wants Europe to step up. The continent’s leaders must find their voice and assert it in talks with Russia.

Alissa de Carbonnel

Mounting economic strain and battlefield losses will not necessarily make the Kremlin less dangerous. They could instead push Moscow toward a more aggressive hybrid campaign designed to test NATO’s Eastern flank, exploit allied hesitation, and fracture European resolve.

Maksym Beznosiuk