Article

Steve Feldstein, Jodi Vittori

To protect their assets for the long term, some countries invest resources and wealth into sovereign wealth funds, which manage a diversified portfolio. But without adequate transparency requirements, these vehicles can be ripe for corruption and other governance risks.

Sovereign wealth funds (SWFs) have existed for more than a century, typically as state-sponsored financial institutions to manage a country’s budgetary surplus, accrue profit, and protect a country’s wealth for future generations. Yet, for economies of the Organisation of Economic Co-operation and Development (OECD), SWFs only burst into public consciousness in the mid-2000s, when widespread concerns arose that SWFs with large amounts of capital could control strategically important assets and threaten the national security of countries where they deployed their investments.

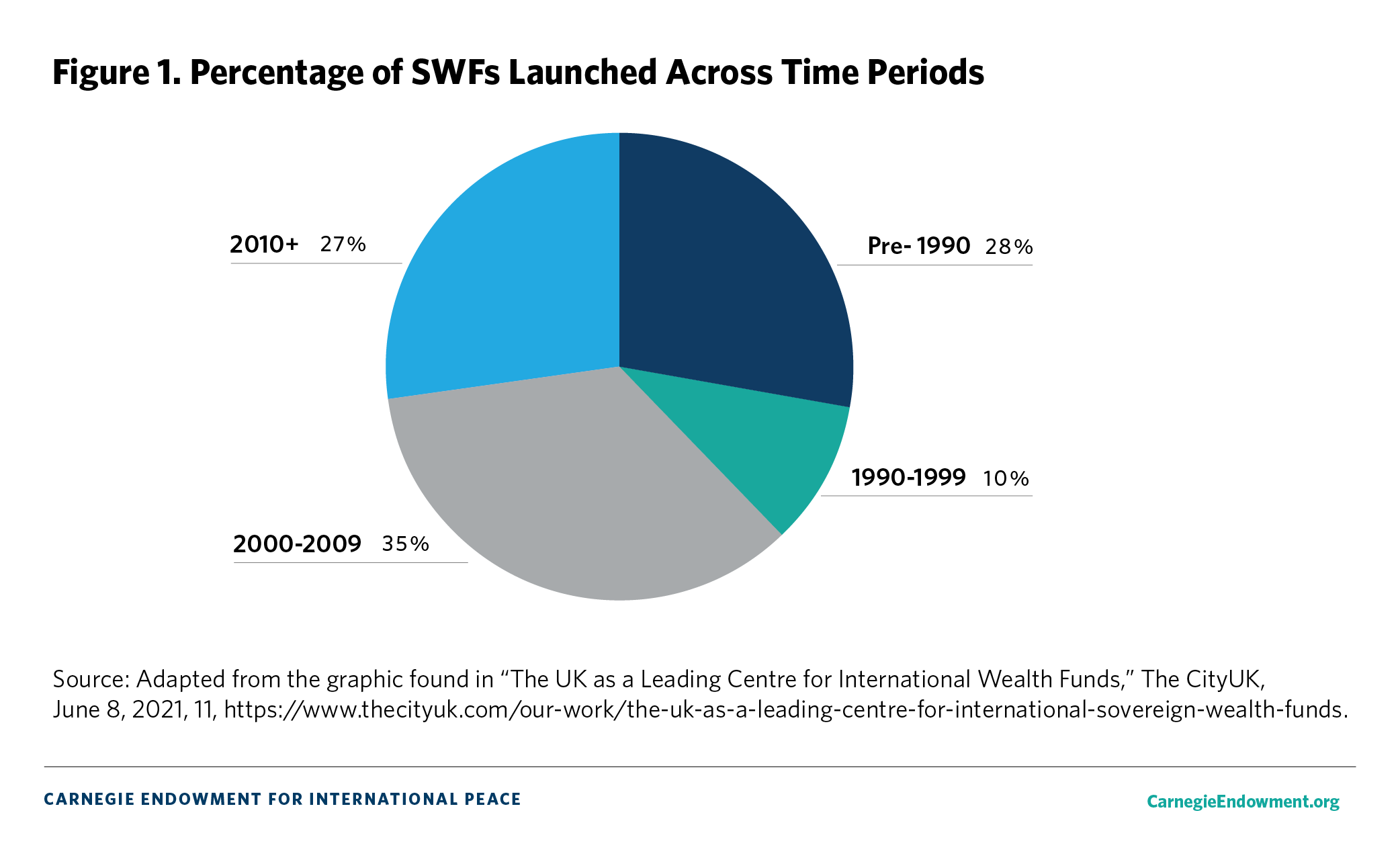

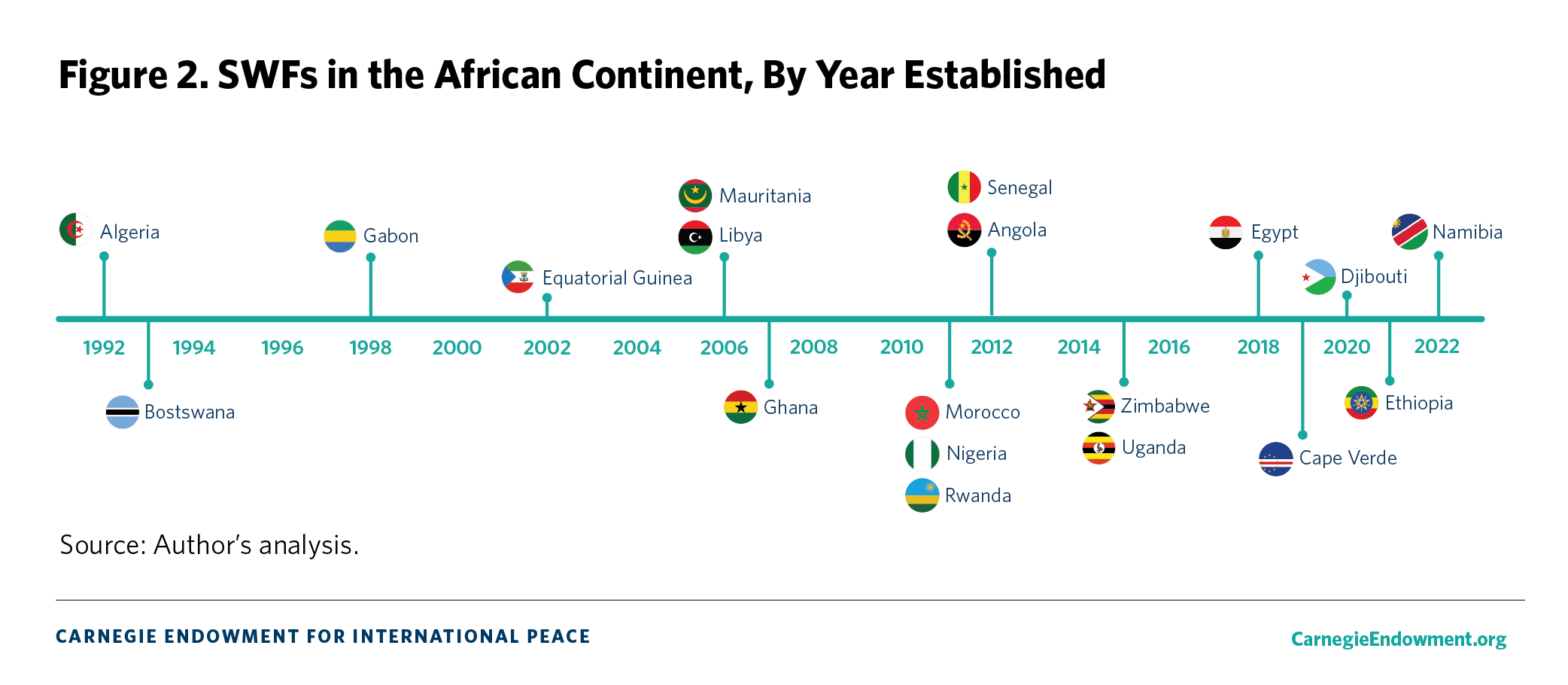

In the 1990s, SWFs held $500 billion in assets, but by 2020, they had more than $7.5 trillion in assets under management (AUM), equal to about 7 percent of the global AUM of $111.2 trillion. Globally, prior to 2010, there were only fifty-eight SWFs. Today, however, SWFs have become an increasingly fashionable type of state-owned entity to set up, and there are currently 118 operating or prospective SWFs. In the African continent alone, prior to 2000, there were only two SWFs. Since 2000, sixteen new SWFs have been set up.

What is particularly concerning about this dramatic growth is that SWFs have been established not just in countries with strong rule of law and civil liberty protections but also in countries marked by high corruption risks, insecurity, violence, and weak or absent rule of law. The chapters that follow include case studies of SWFs from Africa, Asia, Europe, and the Middle East to demonstrate that there are systemic governance issues and regulatory gaps that can enable SWFs to act as conduits of corruption, money laundering, and other illicit activities. This compilation also provides a compelling narrative that highlights the need for clear policies on the management of SWFs, lending weight to the recommendations included in the closing chapter. For SWFs to achieve their full potential, this compilation urges reform not only at the institutional level of the SWF but also across the variety of entities and jurisdictions that make up the supply chain of SWF activity.

As explained in chapter 2, the current SWF data landscape offers only selective, fragmented visibility into SWFs, and little is known about the investments, operations, or internal management of the vast majority of funds around the world. This gap creates opportunities for bad actors to abuse funds for their own interests.

As state-owned entities, SWFs in some ways are set apart from the private investment fund industry, which includes hedge funds, venture capital, and private equity. Notably, an SWF’s mission can go beyond maximizing investment returns to include achieving macroeconomic stability or realizing economic development initiatives domestically. Since they do not have fiduciary duties to private investors and clients, SWFs are completely beholden to the governments that endow them.

Yet even though their home governments can exert influence over their operations, SWFs in practice behave very similarly to certain types of private investment funds. SWFs are often set up identically to private equity funds, with capital committed to the fund managed by an external general partner. In contrast to popular perception, many SWF investments do not end up in publicly traded companies that have strictly regulated transparency obligations and fiduciary responsibilities. Just like their counterparts in the venture capital, private equity, and hedge fund industries, SWFs often purchase minority stakes in unlisted, privately held companies. And because most countries require little if any transparency about fund transactions made outside of public markets, records of SWF investments in unlisted assets, whether in a private company or a real estate project, are rarely made publicly available. In the wake of the 2007–2008 global financial crisis, SWFs have even begun accruing substantial debt and using leverage to fund some investments, another trademark strategy of the private equity industry. SWFs also often act as co-investors with massive private equity funds. Furthermore, many have adopted their own arcane corporate structures called sub-funds to coordinate sectoral investments.

There are also large segments of some SWF portfolios that are almost completely absent from public view, whether it be full lists of nongovernmental investors (foreign and domestic), management fees paid to private investment funds, executive compensation, key relationships with intermediary brokers, or corporate structures facilitating investments (especially through offshore companies). Leaked documents provide perhaps the only window on these attributes. Worse, private, third-party SWF data aggregators are significantly dependent on SWFs sharing their underlying data, and access to this data is often prohibitively expensive for most researchers.

As a result, regulators, journalists, civil society activists, academics, and investors alike are left with regrettably little information about how many SWFs operate. Without detailed financial and operational information, the door is left wide open for rapacious managers and political elites to misappropriate investment earnings. Not only can this lack of transparency make SWFs susceptible to corrupt uses, but at the macroeconomic level, it also raises the specter of real destabilization risks if funds were to fail, be mismanaged, or rapidly withdraw funding from target markets. The lack of oversight into SWFs’ substantial investments could also inflate dangerous equity price bubbles.

Surprisingly, the enormous rise of cross-border SWF investments has not sparked the creation of a centralized international regulatory body to oversee the industry. The closest global institution is the International Forum of Sovereign Wealth Funds (IFSWF), which set forth twenty-four voluntary principles known as the Santiago Principles. These principles aim to improve transparency and governance, but the IFSWF has no power to enforce its own standards, and naming and shaming efforts by other nongovernmental organizations have been mostly absent. As a result, only a select number of SWFs fully adhere to these basic good governance standards, while others are free to invest trillions abroad but disclose little, if any, comprehensive information on their activities to the public.

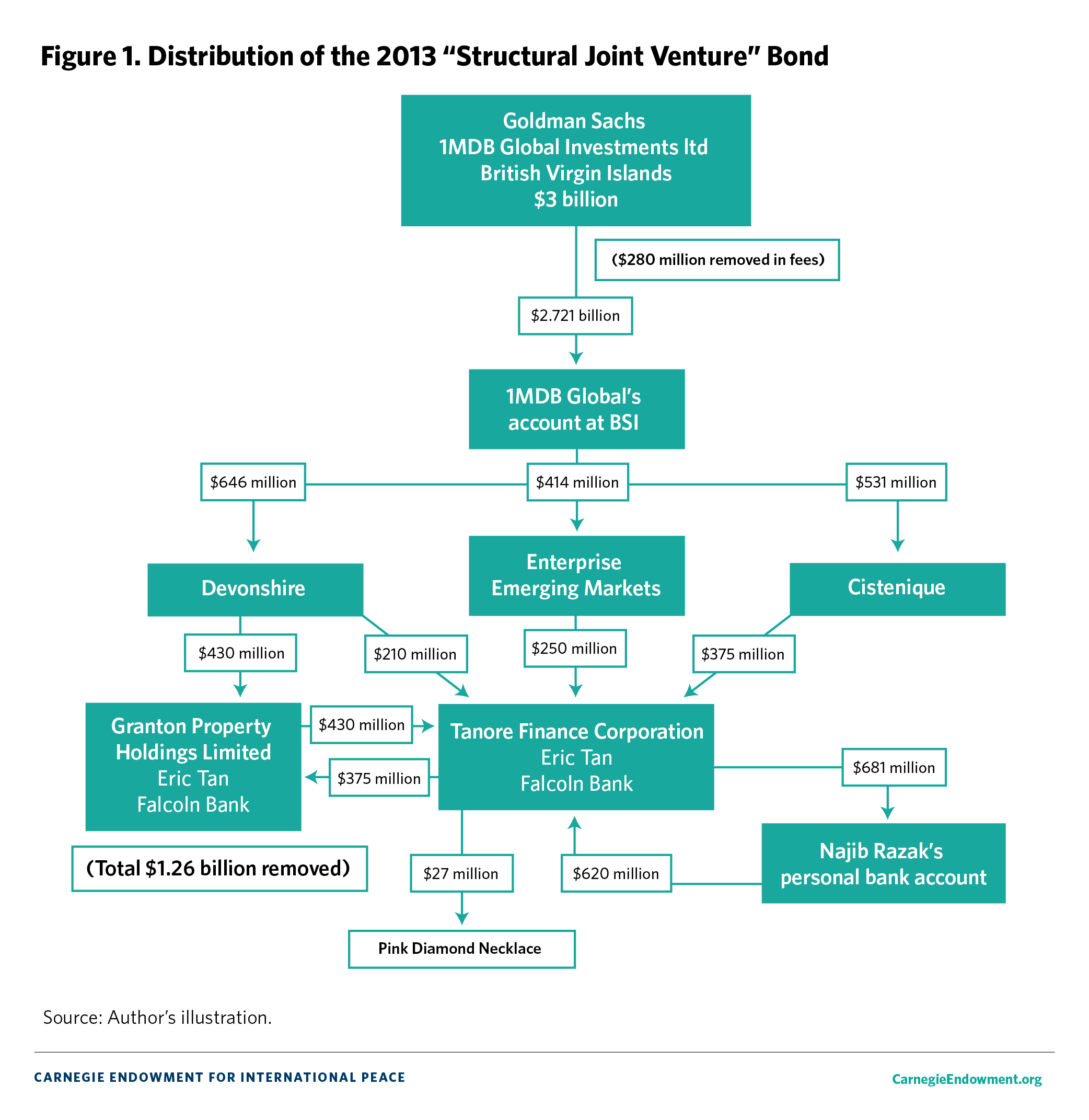

Corruption in Malaysia’s 1MDB sovereign fund led to what the July 2016 original U.S. Department of Justice (DOJ) indictment called the “largest kleptocracy case to date.”1 That indictment noted, “As alleged in the complaints, the members of the conspiracy—which included officials at 1MDB, their relatives and other associates—allegedly diverted more than $3.5 billion in 1MDB funds. Using fraudulent documents and representations, the co-conspirators allegedly laundered the funds through a series of complex transactions and fraudulent shell companies with bank accounts located in Singapore, Switzerland, Luxembourg and the United States.”2

The final tally of diverted funds ultimately came to $4.5 billion. Per the same DOJ indictment, the laundered assets of 1MDB “included high-end real estate and hotel properties in New York and Los Angeles, a $35 million jet aircraft, works of art by Vincent Van Gogh and Claude Monet, an interest in the music publishing rights of EMI Music and the production of the 2013 film The Wolf of Wall Street.”3 Over $1 billion went into then Malaysian prime minister Najib Razak’s personal bank accounts alone.

Chapter 3 provides a comprehensive look at what happened to the Malaysian 1MDB fund between 2009 and 2015 to provide the reader a better understanding of how sovereign wealth funds can be used for gross corruption. It examines how Najib Razak, his proxy Jho Low, advisers from Goldman Sachs bank, and other willing professionals exploited overcentralized power, weak governance, and poor accountability over Malaysian public funds to steal billions for themselves and their collaborators. It also describes how, to increase its influence in Malaysia, the Chinese government was able to use Najib Razak’s need to resolve the scandal and fund his reelection bid. The corruption was likewise exploited by other foreign actors, including royal figures and businessmen in the Persian Gulf to siphon billions for themselves in return for providing cover. The 1MDB case thus provides a useful foundation for making sense of the other cases in this compilation, and it underlines the transparency and accountability reforms required to minimize similar future abuse of citizens’ financial security by their elites.

Chapters 4 and 5 examine the mechanisms for elite capture and pathways for reform by examining evidence from two of Africa’s sovereign wealth funds: Angola’s Fundo Soberano de Angola (FSDEA) and Equatorial Guinea’s Fund for Future Generations (FFG).

As described in chapter 4, Angola’s FSDEA sovereign wealth fund—the African continent’s second-largest SWF—was established in 2012 under former president Eduardo dos Santos, with an initial allocation of $5 billion. The fund was created with the country’s oil revenues with a dual mandate: to invest oil revenues back into the domestic economy and to act as a savings fund to preserve Angola’s oil wealth for future generations.

Conflict of interest concerns were raised when the president appointed his son, José Filomeno dos Santos (also known as Zenu), as chairman of the board, but concerns were assuaged when the fund made a remarkable forty-two-point jump (out of one hundred possible points) in the Peterson Institute’s SWF Scorecard on good governance in a mere three years, plus a good score on another key SWF index. The FSDEA soon became embroiled in reports of a scandal following allegations of questionable corporate governance and investment practices, however. Media reports beginning in 2017, followed by a 2019 report by the International Monetary Fund (IMF), found that billions of dollars were illegally withdrawn from the FSDEA by an asset manager (and business partner of Zenu) using sophisticated financial transactions that were channeled through offshore financial centers and invested in projects and sectors of personal interest. That the fund gave an outward appearance of good SWF governance despite significant corruption highlights the flawed nature of the current SWF assessment tools, especially those based primarily on self-assessments.

The case in Angola can also exemplify that reform of SWFs is possible, even in fragile states. Following a change in the presidency and as a result of the scandal, the FSDEA has rolled out a number of corporate governance and regulatory reforms that better reflect international best practices to try to reposition the fund as a credible state-owned investor.

Another oil-rich African country with an SWF and a regime that international reports have found to be mired in elite capture and corruption is Equatorial Guinea. As described in chapter 5, the country had one of Africa’s highest GDPs per capita at $14,600, but its level of poverty remains one of the highest in the continent, estimated at 67 percent as of 2020.

Equatorial Guinea’s FFG was established in 2002 with a government commitment to deposit 0.5 percent of annual oil revenue into the fund, but it is considered to be one of the least transparent SWFs in Africa with very limited (and in most cases nonexistent) publicly available information. The FFG has no public disclosure of its objectives or mandate, no website, no publicly disclosed governance and institutional framework, no published annual reports, no publicly available information on its board of directors and management, and no publicly disclosed information on asset allocation, investment policy, or fiscal withdrawal rules. Moreover, the leadership of the country exhibits a very high degree of nepotism, and some of the country’s most senior leaders have been convicted of grand corruption. Additionally, oil production long ago peaked there, and the IMF predicts the oil could run out as soon as 2030, making transparency and good governance of the fund an especially time-sensitive priority.

Sovereign wealth funds have especially entered the public consciousness lately due to their nexus with sports, and few countries and their SWFs are so intertwined with sport as Saudi Arabia’s Public Investment Fund (PIF). As described in chapter 6, the emphasis placed on soccer by the PIF since 2016, coupled with the ecstatic local reception of its purchase of the English Premier League’s (EPL) Newcastle United soccer team and subsequent welcome in the city, shine a spotlight on the unconventional returns on investment from such approaches, especially for autocracies like Saudi Arabia. The recent pact between the PIF’s LIV Golf Invitational Series, the European (DP World) Tour sponsored by the United Arab Emirates (UAE), and the Professional Golf Association (PGA) tour has only heightened “sports-washing” concerns.

“Sports-washing” is a nebulous term that emerged in the 2010s as authoritarian regimes began to actively engage more in the infrastructure and ecosystem of global sports. Regimes engaged in sports-washing may be able to enhance their popularity through their association with ownership of sports teams or sponsoring major sporting events while de-emphasizing in the minds of the public their involvement in authoritarianism, human rights abuses, organized crime, and corruption.

SWFs are supposed to help generate economic investment at home, but owning sports clubs overseas does little to generate job creation or technology transfer in the investing country. Indeed, many sports institutions, such as the EPL, rarely post any profit, and hosting sports events is often a net financial loss. This reality suggests that financial rates of return were not necessarily uppermost in PIF considerations for its substantial sports investments. Hence, the PIF’s acquisition presents a study of how an SWF may be used for purposes other than economic diversification and national development.

Emergency situations like the COVID-19 pandemic can also lead to activities by SWFs and their intermediaries that raise red flags for conflicts of interest or corruption. Chapter 7 describes the Russian Direct Investment Fund (RDIF) and its role in the creation, production, and marketing of the Sputnik V vaccine. The RDIF has been sanctioned by the U.S. Treasury Department and the European Union; the U.S. Treasury labeled the RDIF “a symbol of Russian kleptocracy” and states that it is widely considered a “slush fund for President Vladimir Putin.”4 It was established in 2011 by order of the then president of Russia, Dmitry Medvedev, and Putin, who was serving as prime minister. It is an unusual form of SWF: rather than investing the proceeds from domestic oil or other natural resources outside of Russia to help diversify the economy, as SWFs normally do, the RDIF focuses on establishing joint ventures with foreign firms and funds for investments within Russia.

The supply chain for countries to purchase the Sputnik V vaccine ran through the RDIF and a company the fund had established called Human Vaccine. Some countries, such as European Union members Slovakia and Hungary, were able to make direct deals with the RDIF’s Human Vaccine subsidiary to buy Sputnik V doses for $20 for the two-dose regimen. Other countries, however, such as Ghana, Guyana, Lebanon, and Pakistan, had to go through another step in the supply chain because Human Vaccine had appointed Dubai-based Aurugulf Health Investments as the exclusive seller and distributor of Sputnik V for countries in Africa and Asia. Aurugulf was registered in October 2020, just two months after Sputnik V was authorized in Russia, and per the company’s website, Sputnik V appears to be its only product. Aurugulf sold the two-shot regime at $38 per two-dose regimen, or almost double the factory price.

The transparency and accountability of funds associated with Sputnik V vaccine-related expenditures decreased when the expenditures were moved off-budget to the RDIF. This move is especially concerning given the kleptocracy associated with the inner circle of the Putin regime. The backgrounds of intermediaries involved in vaccine distribution only heighten concerns about the risks of corruption. The COVID-19 pandemic has revealed an urgent need to improve governance associated with public health—especially during emergency situations and when governance is outsourced to sovereign wealth funds.

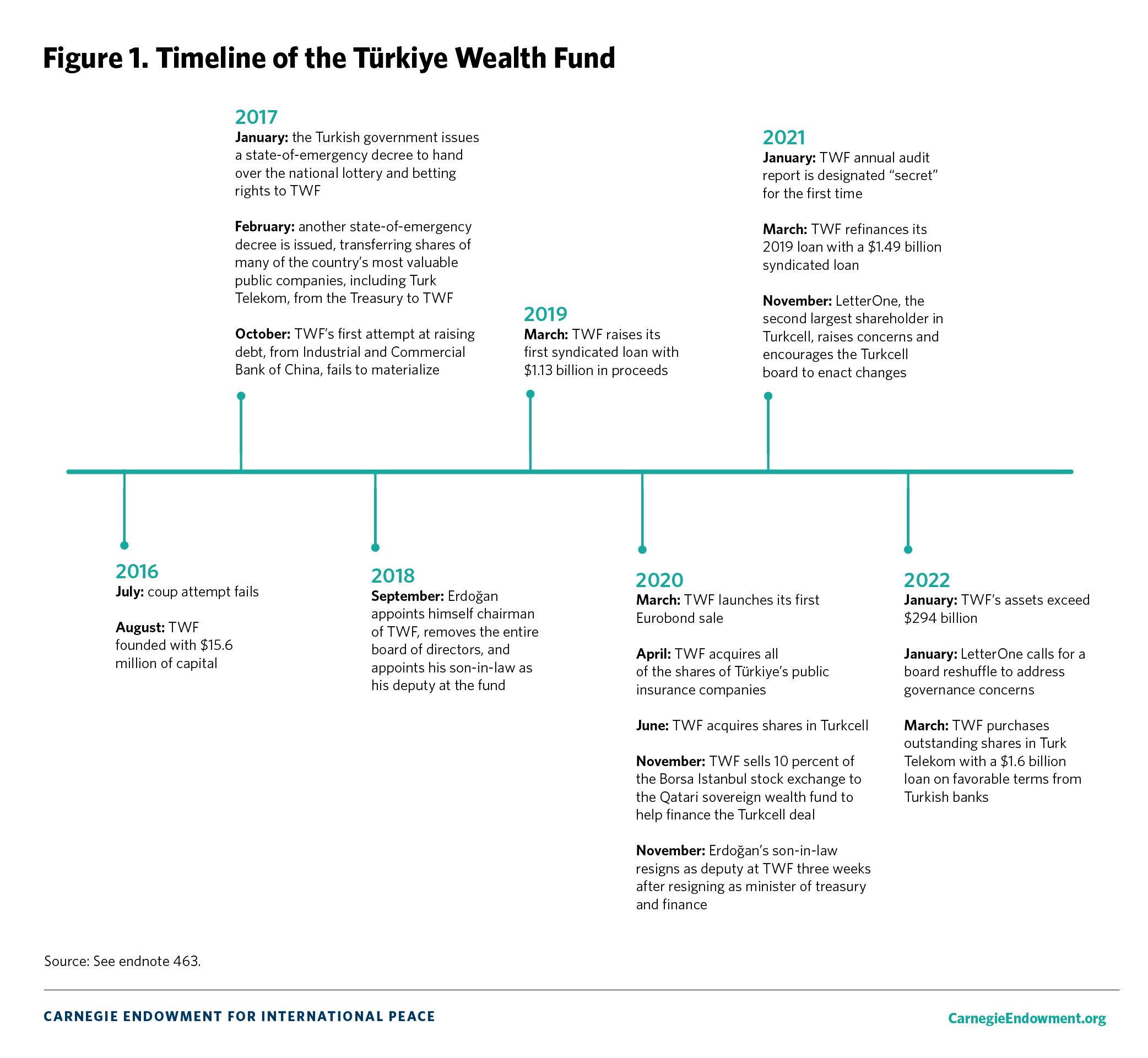

SWFs are most commonly used as a means to invest excess funds from the proceeds of natural resource exports, as evidenced by the SWFs in Angola, Equatorial Guinea, Saudi Arabia, and Russia. But for the Türkiye Wealth Fund (TWF), the term “sovereign wealth fund” may be a misnomer: the country is chronically short of sovereign wealth because it holds no significant hydrocarbon or mineral deposits and suffers from persistent budget and current account deficits. Instead, TWF acts more like a state-owned holding fund that holds shares in state-owned enterprises (as explained in chapter 8).

When TWF started its operations in 2016 with a founding capital of merely $17 million, critics claimed that the fund would function as a “parallel budget” that the Turkish government could exploit to carry out economic and financial transactions outside of parliamentary oversight and public audits.5 Seven years on, Turkish President Recep Tayyip Erdoğan has used it to reward individual and institutional clients, settle political scores, consolidate economic and political power, and shield his economic and financial policies from parliamentary oversight and public audits. This misuse has further deepened the country’s acute governance deficit and contributed to the economy’s underperformance.

In the absence of any viable revenue stream, the Turkish government transferred state-owned enterprises and assets to TWF, but the fund has failed to demonstrate any value-added through these asset transfers. In January 2017, the government issued a state-of-emergency decree to hand over the national lottery and betting rights to the fund. The Turkish Treasury’s stakes in the country’s two largest public lenders, Ziraat Bank and Halkbank; the state oil company Turkish Petroleum Corporation; the flagship carrier Turkish Airlines; and the former state telecommunications monopoly Turk Telekom were also transferred to TWF shortly thereafter with another state of emergency decree. In 2020, TWF acquired a majority stake in the country’s largest mobile phone operator, Turkcell, through a deal involving questionable offshore deals, conflicts of interest, and irregular transactions. As a result, according to the Sovereign Wealth Fund Institute, the fund’s assets exceeded $279 billion as of 2023.

Meanwhile, the Turkish government turned TWF into a collateral instrument to take out additional loans in an economy with an already sizable debt burden of around $450 billion; there was a need to refinance $170 billion in mainly dollar-denominated loans in 2022 alone. In seeking loans, the fund competes not only with the Turkish Treasury but also with private corporations to access local and international capital markets.

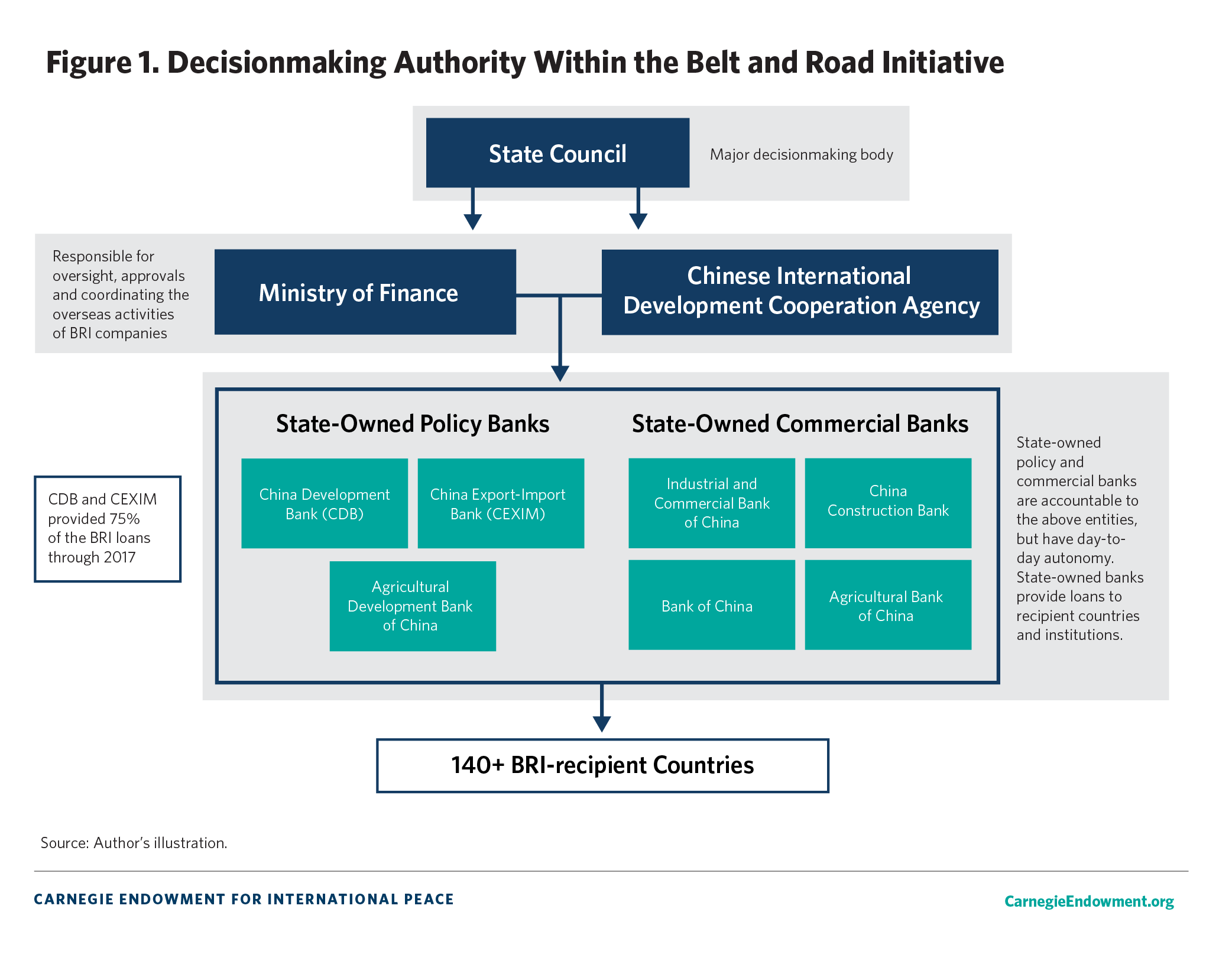

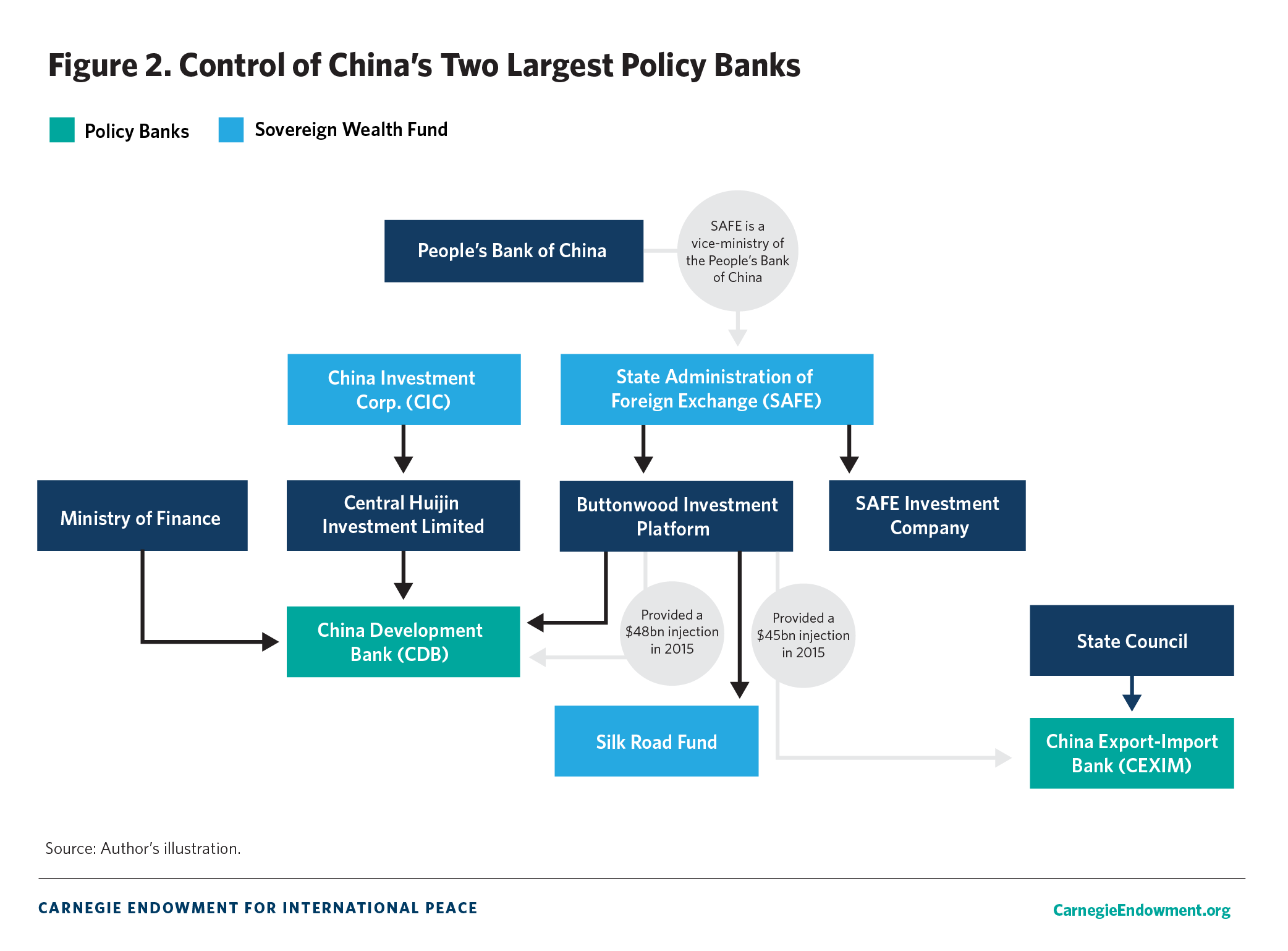

Chapter 9 describes the role that China’s SWFs play in underwriting China’s Belt and Road Initiative (BRI), which has not only supercharged infrastructure investment worldwide but also brought long-standing questions about corruption and political influence to the fore. One key investment sector for SWFs is infrastructure. Infrastructure investment is expected to reach $79 trillion globally by 2040, but alongside extractive industries such as oil and gas, it is the economic sector that remains most strongly associated with corruption risks given that an estimated 20–30 percent of infrastructure project value is lost through corruption.

While China’s policy banks and state-owned commercial banks are the front-end lenders in BRI financing of infrastructure projects, China’s State Administration for Foreign Exchange (SAFE) and its associated China Investment Corporation (CIC) sovereign wealth fund have provided much of the capital, as well as the financial intermediation tools and financial management to move funds from China’s foreign exchange reserves to the BRI’s projects and to help oversee use of the funds.

China’s SWFs have raised some corruption concerns in their own right. A 2016 probe by the Communist Party’s powerful anti-graft body, the Central Commission for Discipline Inspection, reported of CIC that “there were wrongdoings in policymaking and severe problems in the tunneling of interests” and that problems of discipline “occurred frequently.”6 Both SAFE and CIC were reexamined by the commission in early 2022 as part of a broader crackdown on financial sector excess. However, these pronouncements should be treated cautiously given the politicized nature of the anti-corruption campaign.

Instead, the opacity associated with the BRI overall and the way that its financing is disbursed can both be at risk for corruption and conflicts of interest. There is no formal BRI national membership process or structure, with participation in the BRI most often signified through non–legally binding memorandums of understanding (MOUs) or other, less formal cooperation agreements between China and recipient governments. There is no official list of all BRI projects, nor are there consistent standards, certification schemes, or even branding efforts that signify individual Chinese-backed overseas infrastructure projects as being formally part of the BRI (unless they are explicitly mentioned in MOUs). Estimates of the value of BRI total investment and contract costs range from roughly $965 billion by the American Enterprise Institute as of mid-2023 to $8 trillion by the Center for Global Development as of 2018.

A major BRI corruption concern is that associated with infrastructure projects in BRI recipient countries and so-called debt-trap diplomacy. AidData found that 69 percent of official lending by China between 2000 and 2017 went to countries whose credit ratings scored below the global median and that fully 90 percent of BRI-era official lending went to countries that scored beneath the median of the World Bank’s Control of Corruption index. This problem arises because, in an extension of China’s stated policy of noninterference in other countries’ internal affairs, it generally provides BRI loans with few or no preconditions pertaining to transparency, rule of law, or other factors that shape the wider investment climate.

Moreover, a Peterson Institute study of one hundred bilateral Chinese loans found that all loans since 2014 have included “unusual” and “far-reaching” confidentiality clauses that do not permit borrowers to disclose any of the contract terms or related information.7 This is because, while China’s pre-BRI lending was mostly provided directly to governments, nearly 70 percent is now directed to state-owned companies and banks, special purpose investment vehicles, joint ventures, and private sector firms. These debts, though often substantial, do not appear on the public books—though government liability assurances mean that the public will still be on the hook should something go awry.

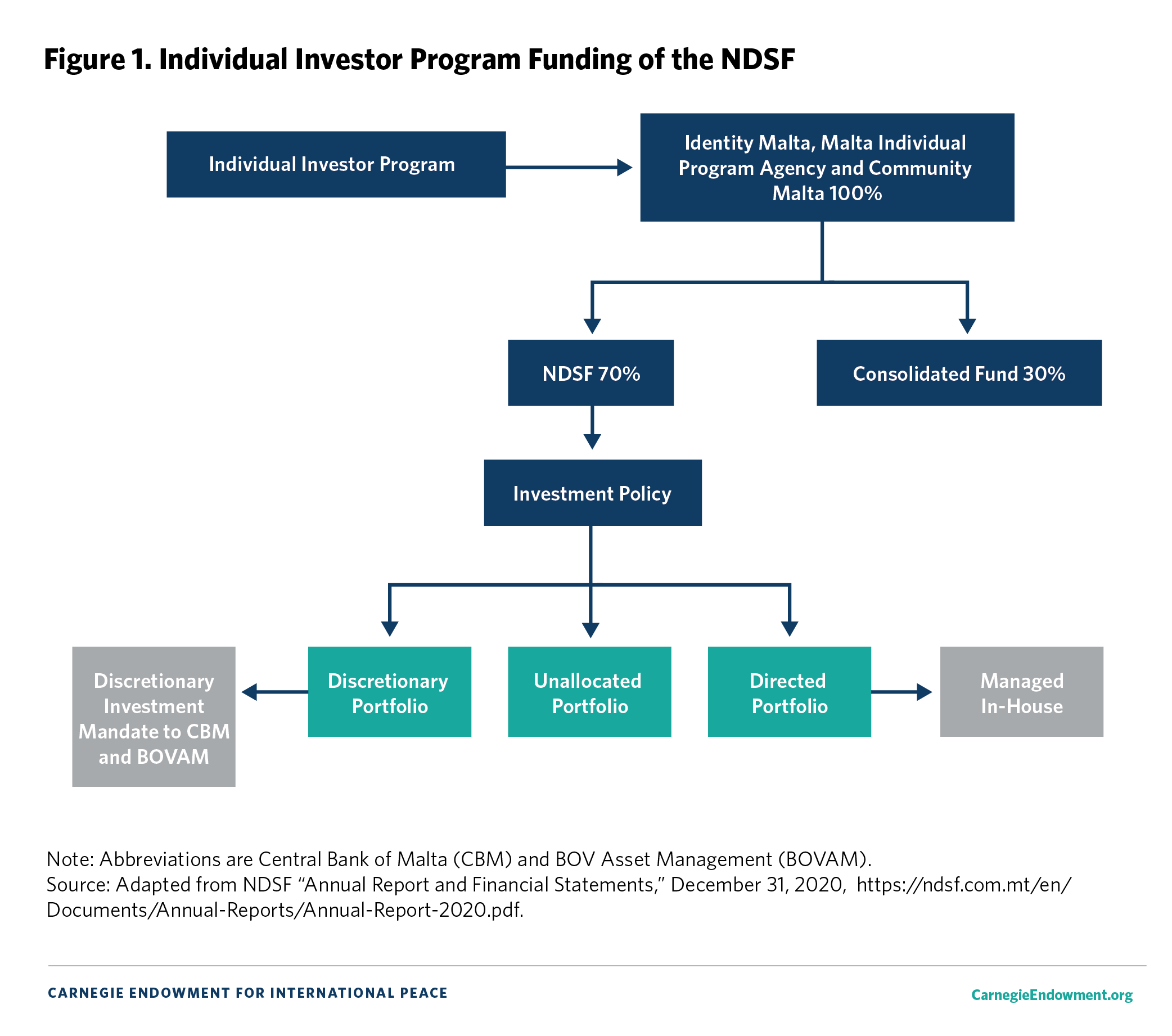

One of the more unique SWF mechanisms is Malta’s National Social and Development Fund (NSDF), which has been funded largely through the country’s Citizenship by Investment (CBI) programs, better known as “golden passport” schemes. As evidenced in chapter 10, CBI programs have long enabled the ultra-wealthy, including the very corrupt, to evade scrutiny for misdeeds, to hide assets, and to acquire international mobility by purchasing citizenship in other countries. An SWF that runs a very high risk of being funded using corrupt, laundered, or ill-gotten wealth strikes at the very heart of what the SWF represents by creating a dependency on potentially ill-gotten gains to fund domestic development. Furthermore, for the Maltese government to use an SWF to invest such proceeds is to benefit from the misdeeds of the corrupt and the criminal. It also allows money that may be ill-gotten to move easily through the financial system under the protection that being part of an SWF entails.

Malta is a small island in the Mediterranean Sea that, despite its European Union (EU) member state status since 2004, one analyst has described as a “corrupting island in a corrupting sea.”8 It has had a “disproportionate role as a hub for transnational illicit flows and criminal activities.”9 Malta has had a variety of CBIs; the 2014 iteration was called the Individual Investment Program (IIP), whereby after payments and investments totalling 1.15 million euros ($1.52 million at the average exchange rate for 2014), an individual could become a full-fledged EU citizen with a passport and all the citizenship and travel opportunities this entails.10 Partially in response to public criticism, in 2020, Malta launched a new CBI program with a higher minimum investment cost and more stringent real estate investment requirements.

CBI applicants are supposed to be fully vetted for security risks. These due diligence checks are vitally important given the fact that Malta is a member of the EU and its Schengen Agreement, affording visa-free travel to up to 182 countries. This travel can allow these new citizens to conduct banking and business under looser standards than would be required under their original passports. They also receive all of the rights to privacy and rule of law and protections against any expropriation that are accorded EU citizens. Moreover, the scheme also provides the potential for golden passport holders to do all of this under a new name, enabling them to bypass security checks or flags on their previous identities.

Despite a four-tier due diligence process established to vet applicants, information leaks revealed that several high-profile Russian individuals obtained citizenship through the IIP between 2016 and 2018. These names are just a few of over 700 Russians who by 2018 were able to purchase Maltese citizenship. The same leaks revealed that citizenship applicants tended to come from countries with a higher risk of money laundering. A plurality of applicants—37 percent—came from Russia, followed by China with 12 percent and Saudi Arabia with 10 percent.

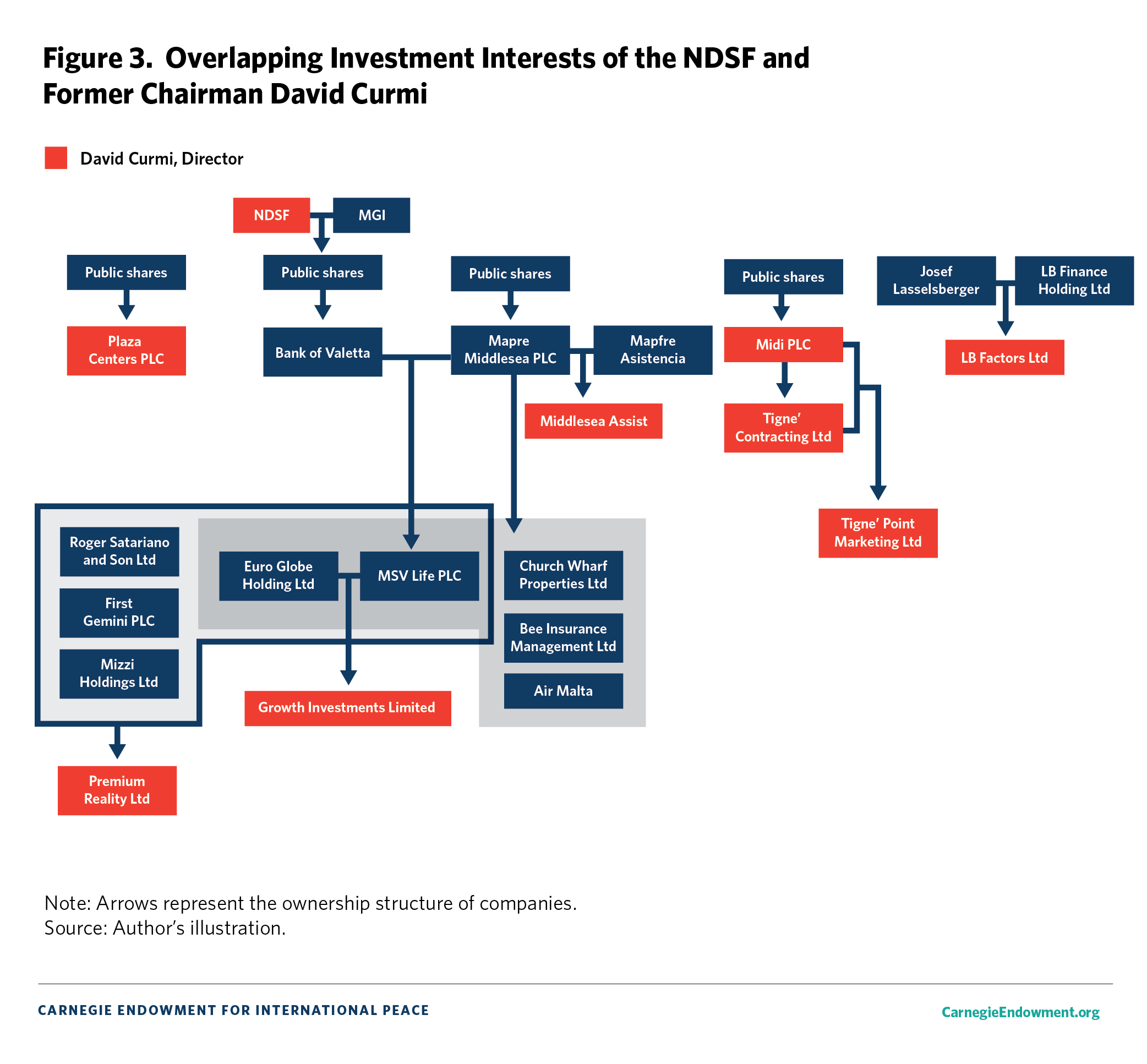

In addition to concerns about who was receiving the passports, there were also concerns about potential conflicts of interest in administering the fund: the chairman of NDSF had individual interests in several companies that the fund also had stakes in.

The sale of passports was profitable for Malta’s SWF, and the country’s budget deficit shrank dramatically following the introduction of its CBI scheme. But funding a state’s SWF through potentially illicit proceeds undermines a country’s rule of law and its citizen trust in democratic institutions. The development associated with such funding mechanisms can also give ruling parties an edge in elections, helping solidify their state capture. Additionally, it can also create perverse incentives whereby states come to rely on illicit funding to stay afloat. These schemes have the potential to facilitate strategic corruption in Western states by making it easy for authoritarians to seed their crony facilitators abroad under the cover of Western residency or citizenship. In turn, these authoritarians can better help their cronies to avoid sanctions and facilitate the laundering of kleptocratic assets that help keep their regimes in power. Their money can then be used to influence Western politicians and other powerbrokers in ways that may undermine larger national security considerations.

The final case study in this report examines the UAE’s use of side contracts associated with arms sales to fund one of its main SWFs, Mubadala, and SWFs associated with Tawazun—a practice that not only increases corruption risks but also risks larger efforts at peace and security worldwide, as described in chapter 11.

The defense sector has long been recognized for its association with corruption. Around the world, the shielding of large amounts of money and equipment under a veil of national security secrecy creates conditions ripe for bribes, kickbacks, and patronage. Especially worrisome to good governance and arms control advocates is a special kind of arms trade contract known as a defense offset agreement, sometimes referred to as “industrial participation” or “countertrade.” These are provisions in arms contracts that promise specific benefits to the contracting country as a condition of that country purchasing defense articles or services from a nondomestic supplier. Offset contracts are a major means for defense companies to improve an arms contract proposal’s standing vis-à-vis other bidders, but they can also be a pathway for kickbacks and patronage, whereby senior officials can direct offsets to their own companies or to underlings in return for loyalty. Based on an analysis of 134 defense companies worldwide by Transparency International, 90 percent of surveyed companies exhibited “limited” to “very low” commitment to combating corruption in defense offset contracts.

Countries can require offset deals to be public and transparent, but a high degree of secrecy is more often the norm. Some countries, including the UAE, declare these contracts to be secret. Others, like the United States, provide only the bare minimum of information. Because so many of these offset deals are extremely complex, even when publicized, tracking the various flows of funds and potential conflicts of interest can be a challenge.

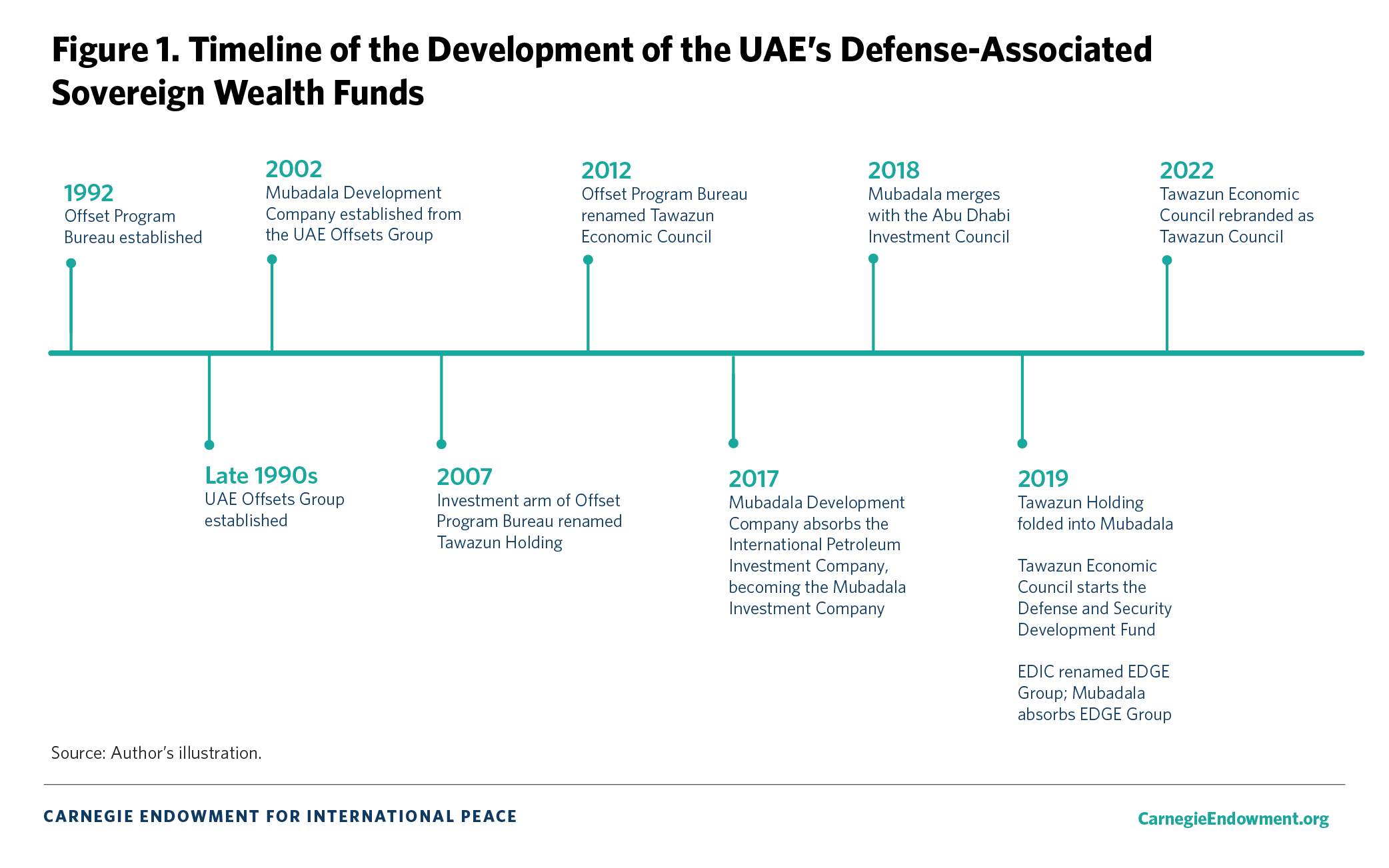

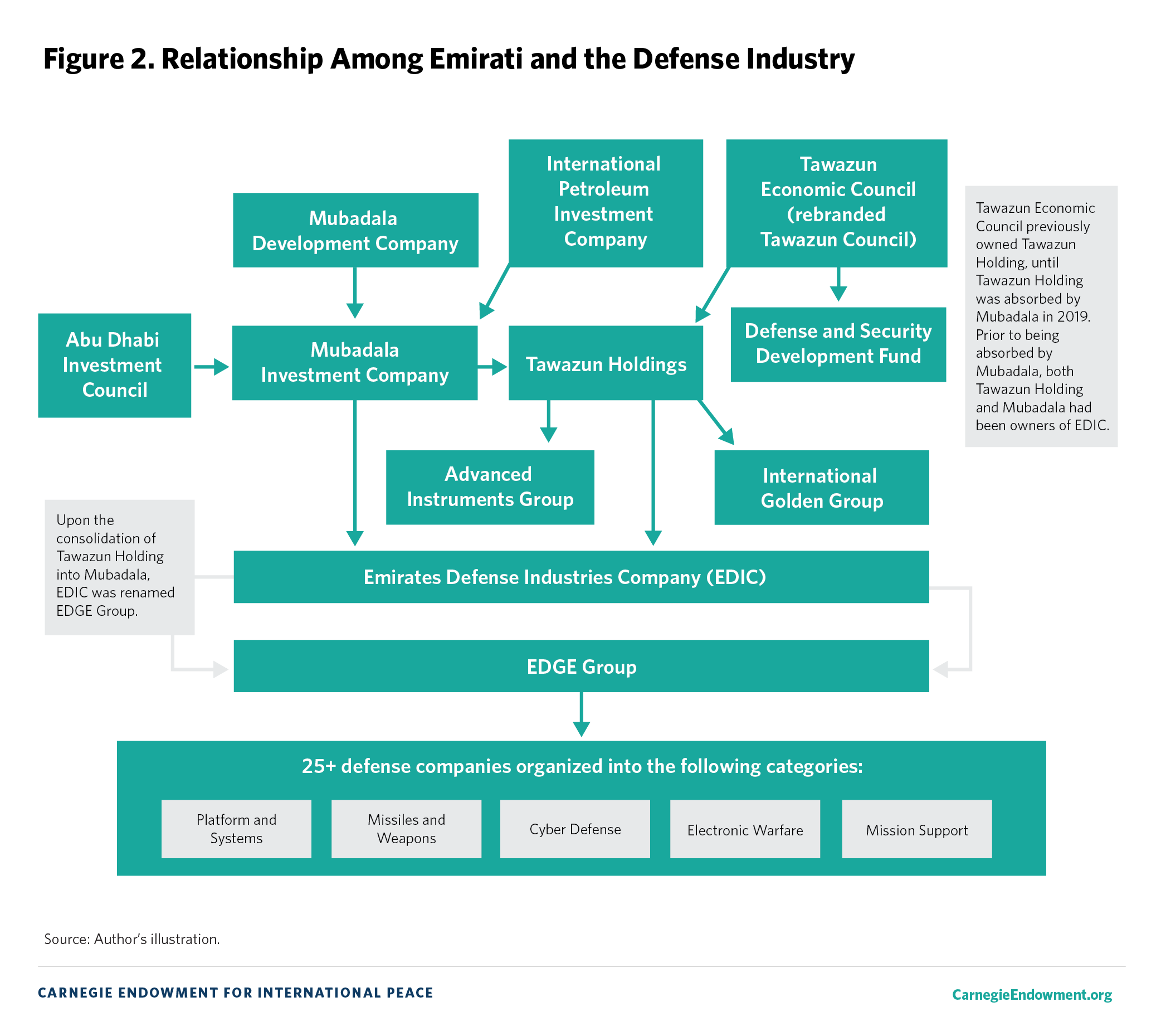

The UAE wraps an additional layer of complexity and opacity around defense procurement arrangements by funneling much of the funds and contracts through Emirati sovereign wealth funds. The UAE is unique in that two of its major SWFs were initially established to funnel proceeds from defense offsets to Emirati companies and citizens, and they remain intimately tied to the Emirati defense industry.

Mubadala, founded in 2002 by the UAE Offsets Group, was created as a civilian adjunct to the overall defense offset program of the Emirate of Abu Dhabi’s military-procurement-focused, high-tech industrial development program. A series of mergers brought its assets to $284 billion in 2018, and it is now the third-largest SWF in the UAE and the thirteenth largest in the world.

Tawazun Council (commonly referred to as Tawazun) was established in 1992 as the Offset Program Bureau. Tawazun oversees the military component of various defense offset agreements. It boasts of creating numerous companies and investment vehicles, including the EDGE Group, which is now the UAE’s main state-owned defense industry conglomerate with more than twenty companies. In 2019, Tawazun’s associated SWF—Tawazun Holding—was absorbed into the Mubadala SWF, and a new $680 million SWF was created under Tawazun called the Defense and Security Development Fund (also called the Strategic Development Fund).

Defense offset funds for Persian Gulf countries are supposed to be used to increase employment opportunities for their nationals, attract new technologies and foreign investment, and reduce their economies’ reliance on oil and gas exports through diversification strategies. In reality, the defense offsets themselves have generally not created many actual jobs, especially compared to the large burden offsets place on state budgets. Moreover, because the purchasing countries front much of the cost of offsets through tax credits and other investment incentives, these programs can be an especially economically inefficient means of generating job growth and facilitating technology transfer.

In the UAE, the defense procurement that feeds into these offset contracts and their associated SWFs is especially susceptible to possible corruption risks. According to Transparency International’s Government Defence Integrity (GDI) Index, which assesses the comprehensiveness of anti-corruption measures in national defense institutions, the UAE is considered a “very high risk” country for defense sector corruption: procurement processes are opaque, underregulated, and lack public oversight. Based on research conducted in 2019, the GDI found no laws or regulations that address the UAE’s defense procurement process. Instead, acquisitions are guided by a secret strategy derived by a small team of Emirati officials and foreign consultants. The UAE has no official reporting mechanisms regarding defense acquisitions except for occasional disclosures to defense industry journalists and experts. While some basic internal auditing practices are in place, there are no external oversight bodies that can monitor the administration of the UAE’s defense purchases.

Moreover, while Mubadala has signed onto the IFSWF and its Santiago Principles and has received good overall ratings by the Peterson Institute’s SWF Scorecard, Tawazun’s SWF has not been rated by the Peterson Institute and is not a member of the IFSWF or a signatory to its Santiago Principles.

In addition to corruption concerns, there can be an especially troubling nexus with conflict and state fragility. For example, the UAE’s Horizon Flight Training Academy was founded via defense offset contracts and is under the EDGE Group umbrella. The majority of its pilots go to the Emirati military, where they have flown in highly controversial military operations in Yemen. This arrangement points to how the funding of SWFs associated with the arms trade can also undermine other global security goals.

The cases in this compilation highlight the need for substantial reform in global SWF governance. For reform to be effective, it must follow along three simultaneous, parallel paths.

When used appropriately, SWFs can help diversify economies, save resources for future generations, help smooth potential swings in the budgets of natural-resource-based economies, and help address budget deficits, especially in hard times. The case studies in this compilation have documented, however, that there can be significant gaps in how SWFs are governed, in both the states that create the SWFs and the countries where SWFs are invested.

One significant problem is the lack of laws and regulations that mandate oversight of SWF investments. What oversight exists is almost exclusively focused on national security concerns in the countries where the investments occur, and little attention is paid to assessing and addressing corruption, money laundering, and other associated governance risks.

In the United States, for instance, federal laws do not specifically restrict SWF investments but rather look to scrutinize or restrict foreign investments that pose a national security risk. These laws operate in conjunction with sector-specific restrictions in areas like telecommunications, energy, and other specific laws that restrict foreign investment. But outside of these generalized restrictions, there appears to be no publicly available guidance on how to address or conduct anti–money laundering due diligence on SWFs.

Other countries, such as the United Kingdom, have partial, directed guidance on how to address anti–money laundering and counter threat finance (AML/CFT) risks in SWFs. To address SWF corruption, money laundering, and other associated governance risks, national governments and private sector actors must first recognize the enabling role they have in facilitating red flag behavior and then address the governance and regulatory gaps that allow this behavior.

The following policy recommendations could help address these gaps:

Fortunately, substantive work has already been done to identify the key reforms needed to ensure that states create robust accountability mechanisms. But the absence of global assessments or enforcement mechanisms, such as through civil society or investigative journalist mechanisms, has limited the broad-based uptake of these suggested reforms. Leading experts in the field have identified four internal reform efforts that are critical to addressing SWF-related governance, corruption, and money laundering challenges. Every SWF should:

Since their creation, the Santiago Principles have remained entirely voluntary and have not been reviewed or updated. The fact that they are voluntary helps make the case that SWFs are ill-equipped to address and enforce the governance challenges of SWFs and the security concerns of the countries where they invest.

While the Santiago Principles have long provided clear context for studying and regulating SWFs’ impact, nowhere in the drafting language is there explicit reference to the potential for abuse. Because the principles have remained static, they do not account for changes in how SWFs are used and operated.

Critics of the Santiago Principles also note that there is no explicit acknowledgment of the significant increase in “novel forms of partnership and collaboration” in “sovereign-private arrangements.”11Explicitly recognizing this increase and enhancing disclosure requirements of these arrangements would alleviate concerns around both national security and corruption risks.

Additionally, there is no requirement to publish audited statements or send them to an international organization that can act as an independent third-party verifier of information. Other international mechanisms such as the Extractive Industry Transparency Initiative—which sets best practices for oil, gas, and mining governance—include this requirement.

The IFSWF also lacks any legal authority to enforce its standards, and unlike with money laundering and tax evasion, international organizations and civil society have shied away from naming and shaming as a way of ensuring compliance.

Self-regulation is ineffective because it is simply not in the interest of the SWFs to critically examine their frameworks. Therefore, the overhaul of international standards must involve greater dialogue and guidance from both the OECD and IMF; SWF reform will not trickle down at the country level unless there are measurable international standards against which SWFs are compared.

The following policy recommendations may help address these gaps:

The intention of this compilation is not to undermine the tremendous value that a well-governed SWF can provide for a country and its citizens for generations to come. Valuable lessons abound from the experience of countries that have successfully transitioned from natural-resource-dependent economies to economic diversification. At the same time, this compilation and the reforms suggested serve to highlight the need for more critical study around the governance risks of SWFs. Failure to understand these risks will lead to SWFs failing to deliver on their promise of economic security and generational citizen wealth.

Note: Citations are used only for direct quotes in this summary; all material used in this summary is fully sourced throughout the compilation.

1 “U.S. Seeks to Recover $1 Billion in Largest Kleptocracy Case to Date,” press release, Federal Bureau of Investigation, accessed February 6, 2022, https://www.fbi.gov/news/stories/us-seeks-to-recover-1-billion-in-largest-kleptocracy-case-to-date.

2 “United States Seeks to Recover More Than $1 Billion Obtained From Corruption Involving Malaysian Sovereign Wealth Fund” (The United States Department of Justice, July 20, 2016), https://www.justice.gov/opa/pr/united-states-seeks-recover-more-1-billion-obtained-corruption-involving-malaysian-sovereign.

3 “United States Seeks to Recover More Than $1 Billion Obtained from Corruption Involving Malaysian Sovereign Wealth Fund.”

4 “Treasury Prohibits Transactions With Central Bank of Russia and Imposes Sanctions on Key Sources of Russia’s Wealth,” press release, U.S. Department of the Treasury, February 28, 2022, https://home.treasury.gov/news/press-releases/jy0612.

5 Mustafa Sonmez, “Under Financial Strains, Turkey Designs ‘Parallel Budget’,” Al-Monitor, November 10, 2016, https://www.al-monitor.com/originals/2016/11/turkey-financial-strains-designs-parallel-budget.html.

6 Wendy Wu, “China’s Financial Giants Hammered in Discipline Review,” South China Morning Post, February 5, 2016, https://www.scmp.com/news/china/policies-politics/article/1909938/chinas-financial-giants-hammered-corruption-review.

7 Anna Gelpern, Sebastian Horn, Scott Morris, Brad Parks, and Christoph Trebesch, “How China Lends: A Rare Look Into 100 Debt Contracts with Foreign Governments,” Peterson Institute for International Economics, May 2021, 5, https://www.piie.com/sites/default/files/documents/wp21-7.pdf.

8 Luca Ranieri, “The Malta Connection: A Corrupting Island in a ‘Corrupting Sea’?,” The European Review of Organized Crime 5, no. 1 (2019): 10–35; 1.

9 Ranieri, “The Malta Connection," 2.

10 Christopher Giles, “Malta’s ‘Golden Passports’: Why Do the Super-Rich Want Them?,” BBC News, December 4, 2019, https://www.bbc.com/news/world-europe-50633820.

11 Adam D. Dixon and Imogen T. Liu, “Santiago Principles 2.0: Advancing the Agenda,” International Forum of Sovereign Wealth Funds, https://archive.ifswfreview.org/2018/our-partners/santiago-principles-20-advancing-agenda.

12 However, this process should ensure that developing country SWFs are not unfairly targeted, as this has potential consequences for de-risking. There has been criticism around global listing processes. For more information, see “When Banks Leave: The Impacts of De-Risking on the Caribbean and Strategies for Ensuring Financial Access,” Statement of The Honorable Mia Amor Mottley, Prime Minister of Barbados, Minister of Finance, Economic Affairs and Investment and Minister of National Security and Civil Service at the Hearing of the United States Representatives Committee on Financial Services, September 14, 2022, https://democrats-financialservices.house.gov/uploadedfiles/hmtg-117-ba00-wstate-mottleym-20220914.pdf.

Sovereign wealth funds (SWFs) have existed for more than a century, typically as state-sponsored financial institutions that manage a country’s budgetary surplus, accrue profit, and protect a country’s wealth for future generations.1 Yet, for the economies in the Organisation for Economic Co-operation and Development (OECD), SWFs only burst into public consciousness in the mid-2000s, when widespread concerns arose that SWFs with large amounts of capital could control strategically important assets and threaten the national security of countries where they deployed their investments.2

The term SWF itself refers to money that is invested by a country in order to protect it from economic shocks or to save it for future generations. The institutions featured in this paper have been included and classified as SWFs if they are members of the International Forum of Sovereign Wealth Funds (IFSWF), if leading investor subscription services like the Sovereign Wealth Fund Institute have categorized them as SWFs, or if cases or investigations have referenced them as SWFs. Only vehicles owned by a country’s national government have been included.

Early SWFs were set up in countries whose economies were reliant on exporting natural resources like oil, phosphate, and copper (for example, Chile, Kiribati, Kuwait, and Norway). Governments wanted to create a mechanism by which excess revenues generated when commodity prices were high could act as a buffer when there was an economic downturn. SWF investments also helped smooth out budgets, as the prices of those exports could rise and fall on international markets. SWF funding sources have expanded to include any surplus from foreign reserves, budgets, a country’s central bank reserves, public-private partnerships, or citizenship-by-investment schemes.

In the 1990s, SWFs held merely $500 billion in assets,3 but by 2020, they had more than $7.5 trillion in assets under management (AUM), equal to about 7 percent of the global AUM of $111.2 trillion.4 This exponential growth in SWF investments has seemingly ignored many potential systemic corruption and other governance challenges. As outlined in this chapter and those that follow, SWFs are often found in countries with high risks of corruption and significant governance challenges including poor rule of law. And because SWFs are usually completely under the control of governments, they can be used to pursue purely political goals. Moreover, SWFs often have no fiduciary responsibilities or minimal reporting obligations, making it difficult to understand where a country’s money is invested. Despite SWFs being publicly financed entities, they are not subject to rigorous international financial disclosure and accountability mechanisms that would check for issues such as corruption. There is also a substantial network of intermediaries (financial experts and professionals) that help SWFs invest, which, as this paper documents, can raise the risk of corruption and other governance challenges, if there is poor oversight and accountability. Basically, SWFs are only subject to voluntary self-regulation, and so far, as of 2021 twenty-nine SWFs—which account for roughly 80 percent of all SWF assets—are only in partial compliance with the self-assessment standards set out by IFSWF.5

Public consciousness of SWFs, their roles in economies, and their potential political impact grew during the 2007–2008 global financial crisis. Some SWFs played a “white knight” role to several Western financial institutions, providing large capital infusions to banks facing bankruptcy.6 In the first six months of 2008, SWFs injected more than $80 billion into Barclays, Merrill Lynch, Morgan Stanley, and UBS, stabilizing the global credit market.7 At the same time, however, these large investments drew much more public scrutiny to SWFs. Yet, most of the international, government, and academic discourse since then has centered around the impact of SWFs on corporate governance, financial market stability, and national security risks—with corruption risks rarely being discussed.

The potential for SWFs to be used for grand corruption and kleptocracy first gained widespread attention in the early 2010s due to a scandal involving a Malaysian SWF called 1Malaysia Development Berhad (1MDB), which is described in detail in chapter 3. Under former Malaysian prime minister Najib Razak and a financier named Jho Low, a series of con artists, bankers, Malaysian elites, and even Hollywood movie stars benefited from the diversion of more than $4 billion in funds from Malaysia’s 1MDB SWF.8 As media reports began to highlight troubling issues with the fund and as the U.S. Department of Justice launched an investigation, 1MDB found it difficult to use the international banking system. However, elites from Saudi Arabia and the United Arab Emirates came to the rescue, using their personal reputations and their own SWFs to help 1MDB continue to launder funds.

In the wake of that headline-grabbing corruption scandal, the question that remains unanswered is whether current research, government regulation, and international standards can adequately deal with the corruption and other governance risks that SWFs present. Using case studies of SWFs from Africa, Asia, Europe, and the Middle East, the chapters in this compilation demonstrate that enduring systemic governance issues and regulatory gaps have enabled SWFs to act as conduits of corruption, money laundering, and other illicit activities. For SWFs to achieve their full potential, reform is needed not only at the institutional level of the SWF but also across the variety of actors and jurisdictions that make up the supply chain of SWF activity.

This introductory chapter is intended to help set the scene for what is a complex topic. The chapter presents an overview of SWFs, the potential risks of corruption and rent-seeking activities, and the impact these behaviors can have on a country’s citizens. The chapter also demonstrates how SWFs have evolved, how they are funded, where and how they invest, and the current international and domestic regulatory landscape. Finally, it summarizes the different SWFs examined and the recommendations for helping them reach their potential.

Any discussion of SWFs is incomplete without addressing an ever-present definitional conundrum. Though recognized SWFs like the Kuwait Investment Authority (KIA) have been around since the 1950s,9 the term “sovereign wealth fund” emerged only in 2005,10 when it was coined by financial analyst Andrew Rozanov as a way to differentiate SWFs from other institutional investors.11 Since then, however, international organizations, governments, and academics have all created and employed slightly different definitions of the term SWF.12 The lack of a clear, single definition makes monitoring SWFs for money laundering, corruption, and other rent-seeking especially challenging because there is no uniform way to provide guidance on potential risks and to identify what financial behavior should be monitored and assessed. The differences in SWF definitions have also prevented states from maximizing their combined efforts in countering illicit acts.

Perhaps the best-recognized definition is the one contained in the Generally Accepted Principles and Practices (GAPP) that govern SWFs, otherwise known as the Santiago Principles. Drafted by the International Working Group on SWFs, the Santiago Principles define SWFs as “special-purpose investment funds or arrangements that are owned by the general government.”13 Created for macroeconomic purposes, SWFs hold, manage, or administer assets to achieve financial objectives and employ a set of investment strategies that include investing in foreign financial assets. SWFs are commonly established out of balance-of-payments surpluses, official foreign currency operations, the proceeds of privatizations, fiscal surpluses, and/or receipts resulting from commodity exports.

The Santiago Principles are considered global foundational standards under which SWFs have committed themselves to operate. A key element of the SWF definition is that the fund must be owned by a national or subregional government. For example, a fund owned by the state of Alaska would qualify as an SWF because it was owned by a state government within the United States. The next criterion is that the vehicle’s investments must include foreign investments. Therefore, any fund with a mandate to invest all its money domestically would not be considered an SWF. By that measure, the Türkiye Wealth Fund (discussed in chapter 8 of this compilation) would not usually be considered a SWF, as it has a purely domestic mandate. But to ensure consistency across the cases presented here, entities treated as SWFs in practice, such as the Turkish fund, are also included. Appendix A provides a more detailed discussion of various SWF definitions.

Charting the story of SWF growth provides important evidence for why so many SWFs appear to have serious corruption, money laundering, and other governance risks. Globally, prior to 2010, there were only fifty-eight SWFs.14 Today, however, SWFs have become an increasingly “fashionable” type of state-owned entity (see figure 1), and there are currently 118 operating or prospective SWFs.15 In the African continent alone, prior to 2000, there were only two SWFs. Since 2000, sixteen new SWFs have been set up (see figure 2). This increase in the number of SWFs has also meant a dramatic increase in the value of the assets that they own or control.

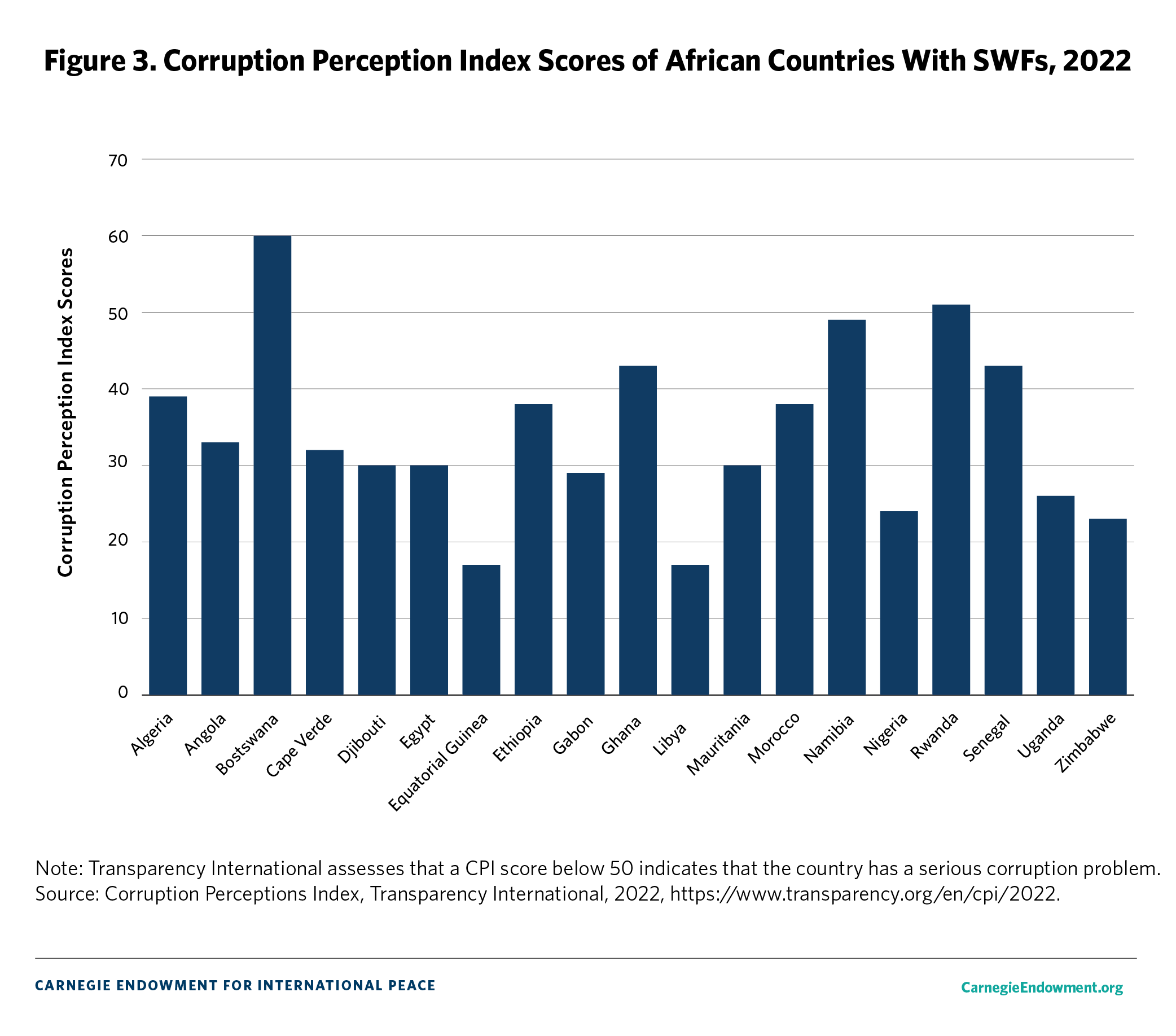

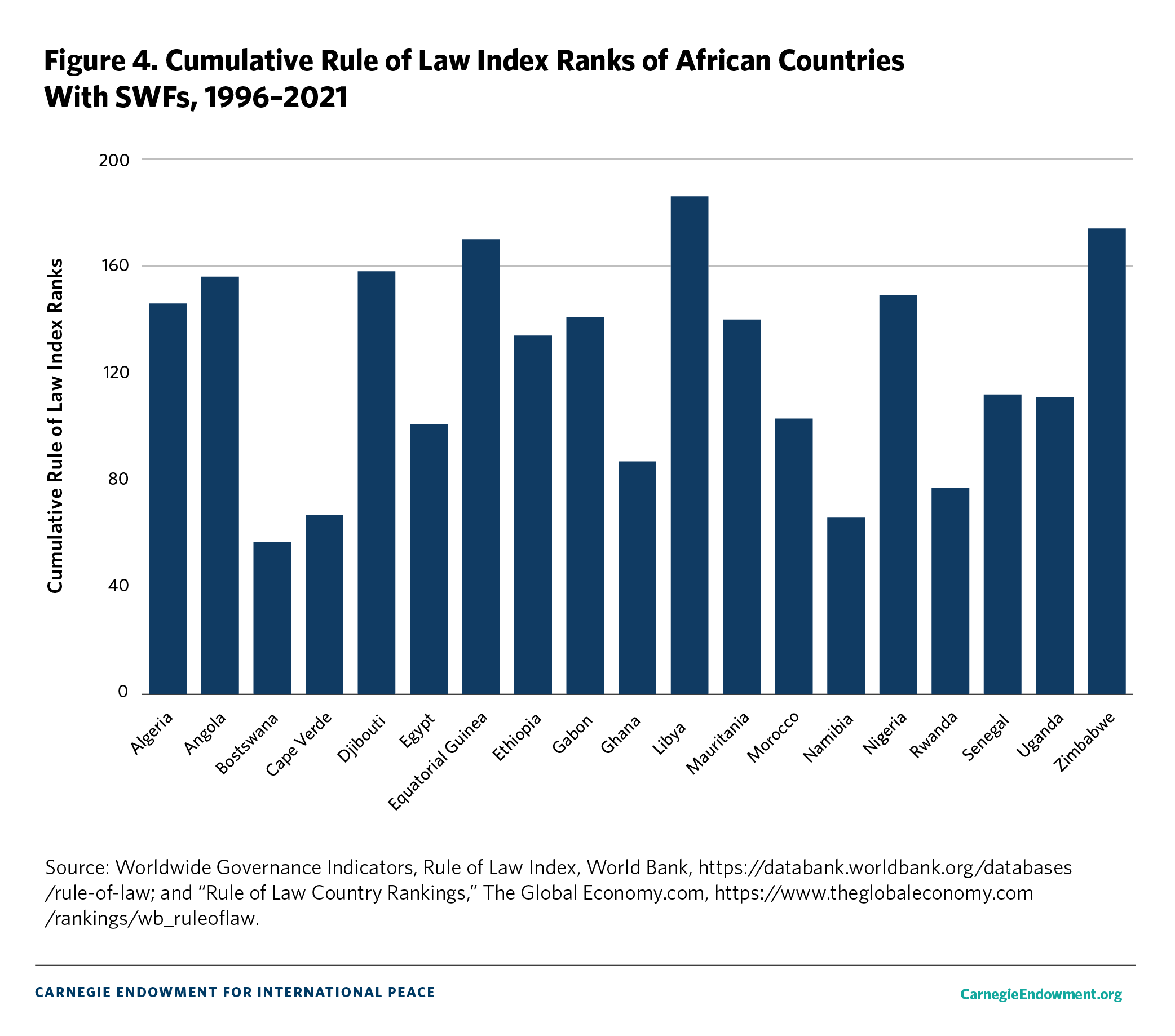

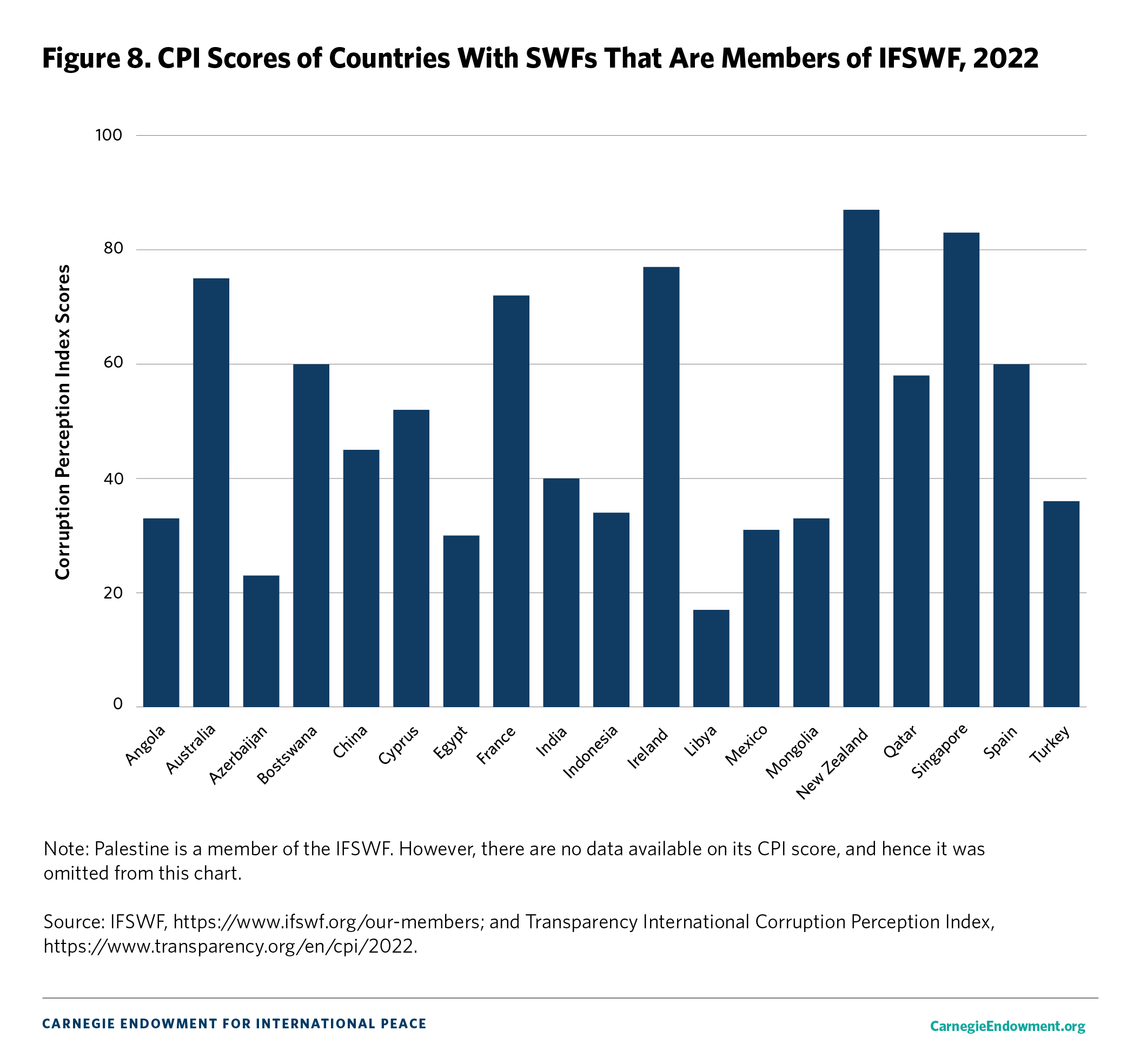

This dramatic growth in SWFs is concerning because they have been established not just in countries with strong rule of law and civil liberty protections but also in countries marked by high corruption risks, insecurity, violence, and weak or absent rule of law. For example, in 1999, the State Oil Fund of the Republic of Azerbaijan was set up, and as of April 2023, it reportedly had $53.4 billion in AUM.16 Meanwhile, in 2022, Transparency International’s (TI) Corruption Perceptions Index (CPI) gave Azerbaijan a failing score of 23 out of 100, ranking the country 157 out of 180 countries; in 2021, the World Bank’s Rule of Law Index (ROLI) ranked the country 131 out of 192 countries.17 In another example, in 2002, Equatorial Guinea’s Fund for Future Generations was set up (see chapter 4), and now it reportedly has $165 million in AUM.18 Yet the CPI gave Equatorial Guinea a failing score of 17 out of 100, ranking the country 171 out of 180 countries; the ROLI ranked the country 175 out of 192 countries.19 Figures 3 and 4 demonstrate the CPI and ROLI index scores of African countries where SWFs have been established.20 With few exceptions, like Botswana and Namibia, the vast majority of countries on the continent that have or plan to set up SWFs have significant corruption risks and weak rule of law systems. Can SWFs that are meant to safeguard wealth for future generations successfully operate in a corruption-rich environment? The evidence that unfolds in the following chapters raises serious concerns about the state of play of existing governance norms and enforcement efforts. It also provides a compelling narrative on the need for clear policies related to the management of SWFs and lends weight to the recommendations included at the end of this compilation.

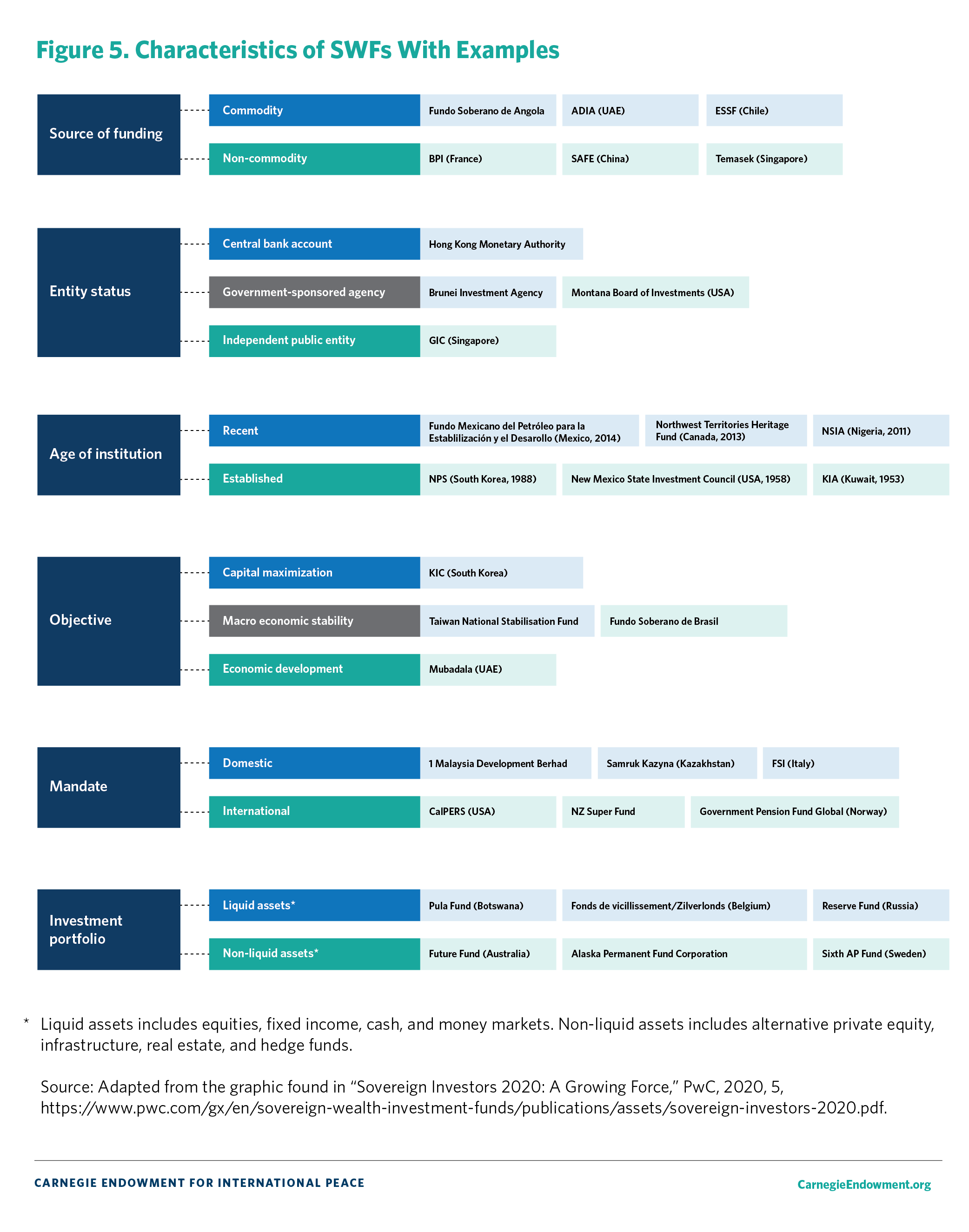

This dramatic growth in SWFs is also concerning because the sources of funding, objectives, mandates, investment portfolios, and the legal mechanisms through which SWFs have been set up vary significantly, making it more difficult to monitor and assess SWF behavior. Early SWFs could be broadly divided into three categories based on their unique objectives: (1) stabilization funds established to insulate a country’s economy from both internal and external shocks; (2) capital maximization funds established to transform natural resource revenues into longer-term wealth for future generations; and (3) strategic development funds established to help create jobs, improve infrastructure and development within the country, and ultimately help diversify the economy by moving it away from reliance on a particular sector or natural resource. Today, SWFs often have multiple objectives and mandates, and governments can alter the objectives based on changing priorities.

For instance, the KIA was set up in 1953 with the objective to invest Kuwait’s excess oil revenues and preserve the country’s oil wealth for future generations, and its mission has not changed.21 Similar to the KIA, the Revenue Equalization Reserve Fund of Kiribati was created in 1956 to act as a store of wealth for the country’s earnings from phosphate mining.22 Early funds of this type were conservative in their investment strategies, primarily focused on investing in a mix of money market instruments.23

However, later SWFs—such as Bpifrance, Singapore’s GIC, the Türkiye Wealth Fund, and the Maltese National Development and Social Fund—were set up as noncommodity funds financed through the respective country’s foreign reserves or as existing public equity interests or assets financed through the sale of state-owned assets (or in Malta’s case, through the sale of the country’s passports).24 As the sources of funding have changed, so have the investments, objectives, and mandates of the funds.

According to the case studies in this compilation, SWFs have been used to amass large art collections (see chapter 3); acquire global sports teams and sponsor international sporting events (chapter 4); fund the development of, and manage the profits from, a national COVID-19 vaccine program (chapter 7); and route payments for defense contracts (chapter 11). All these investments are supposed to further the SWF’s stated goals of capital maximization, macroeconomic stability, or economic development. However, in reality, they are commonly linked to an array of potentially unlawful activities. And as each of the case studies in this compilation highlight, one need not probe far to reveal a pattern of troubling behavior. But, as this compilation will also lay out, domestic and international standards lack the language necessary to identify risks that lead to this behavior. Additionally, the discussion around SWF risks is seemingly divorced from the wider discourse on anti-corruption, anti–money laundering, and other norms associated with other types of state-owned entities.

Figure 5 illustrates that SWFs exist across a range of categories. Coupled with the aforementioned definitional issue, these variations in type make identifying atypical SWF behavior or SWFs at risk for corruption and money laundering all the more challenging.

In addition to the aforementioned factors, how an SWF’s objectives are fulfilled can contribute to governance and illicit finance risks. The mechanics of these investments and the network of actors and jurisdictions that facilitate these investments provide additional context on why corruption and broader governance risks of SWFs are allowed to thrive. As complex investment vehicles, SWFs and their investment strategies can be mapped in myriad ways; however, because the intention of this compilation is to address the corruption and money laundering pathways of SWFs, this paper will focus on answering three questions: How do SWFs invest? Who helps SWFs invest? And where do SWFs invest?

The purpose and objective of a fund determine how its investments are directed. For instance, capital maximization funds like the KIA—which tend to be the most “risk-seeking”—invest in hedge funds, real estate, private equity, and infrastructure (known collectively as “alternatives”) and other so-called yield-generating assets to meet their objectives. These assets aim to bring an investor short-to-medium-term returns by paying out dividends, providing an interest, or generating similar financial income.

Stabilization funds like the Mexico Oil Revenues Stabilization Fund have short investment time horizons and tend to be very liquid. As a result, they are looking for investment opportunities, such as bonds, treasury bills, and guaranteed investment certificates, otherwise known as long-term fixed income securities.25 Finally, sitting in the middle, economic development funds like Mubadala in the United Arab Emirates (UAE) invest in alternatives and other safer assets—such as short-term fixed income securities—to ensure a stable stream of lower-risk financing and to provide the SWF with consistent returns (see figure 5).26

These neat demarcations are useful in categorizing the overall mode of operations of SWFs, but they do not reflect all the ways in which a country uses an SWF or how the SWF’s priorities can shift over time.27 Stabilization funds, which tend to be the most risk averse, invest their money in cash, shares listed on a stock exchange, or investments that will provide a fixed income to the SWF through the life cycle of the investment.

For instance, the Malaysian 1MDB fund was set up as an economic development fund, and its investments were apparently intended to further the country’s development goals. But as chapter 3 discusses, these investments were merely a front to divert $4.5 billion with the assistance of numerous individuals, including government officials from Malaysia, Saudi Arabia, and the UAE. The investment mechanism was seemingly legitimate—involving financial institutions with world-class reputations, such as Goldman Sachs—but, in reality, it was laundering stolen money to fund the individuals’ lavish lifestyles.

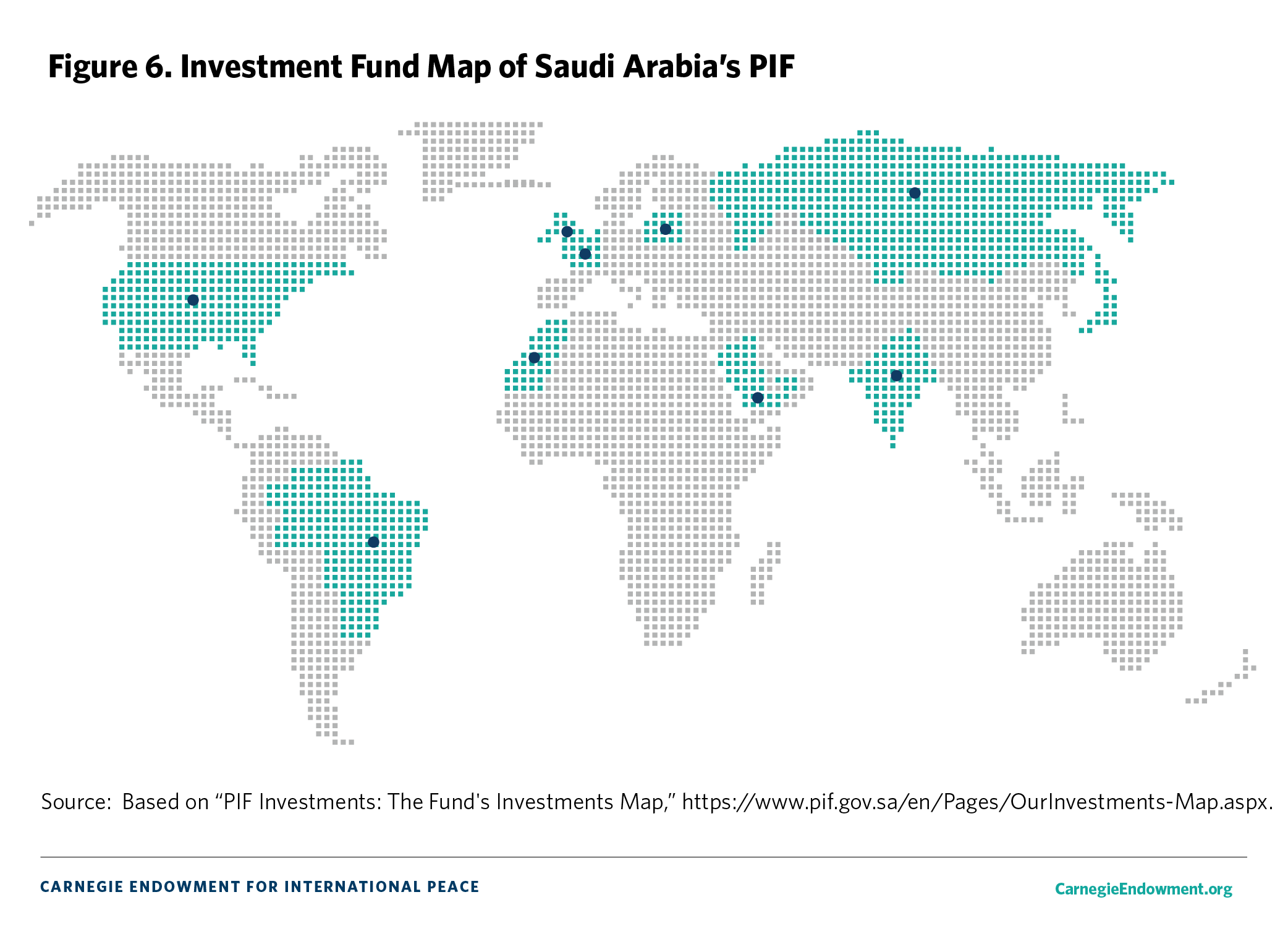

Saudi Arabia’s Public Investment Fund (PIF) has a similar global footprint and now supposedly has about $700 billion in AUM (see chapter 6 and figure 6).28 However, officials within the PIF have reportedly voiced concerns about the riskiness of PIF’s $2 billion investment into Affinity Partners, a private equity fund owned and operated by Jared Kushner.29 Investments like this and the recent pact between Saudi Arabia’s LIV golf tournament with the Professional Golf Association (PGA) Tour blur the line between pursuing economic development and purchasing economic or political influence, thus making assessments around corruption and other governance risks more challenging.

The way these SWF investments are carried out presents another difficulty in tracking them. SWF investment methods broadly fall into three types:

Each investment method has an impact on profitability and its own corruption, money laundering, and governance risks. On the face of it, direct SWF investment may appear the easiest to track and therefore the easiest for public oversight and for authorities to check for money laundering or corruption risks. However, financial institutions and government agencies still need to explicitly evaluate and differentiate these risks based on the SWF’s location and the governance and transparency levels within the fund. With much of the discourse focused on the national security risks of SWFs, there appears to be little scrutiny of a variety of other types of risks. For instance, a lawsuit filed in Massachusetts alleges that $3.5 billion was stolen from the Saudi PIF and some of it was used to purchase eight condos in Boston.34 Yet prior to the lawsuit filed by the Saudi government, the transaction did not raise any red flags from financial institutions within the United States.

Still, indirect SWF investment may be more challenging to track and monitor. SWFs can often invest in a private equity fund and then use the private equity fund to make further purchases. This obscures the SWF’s identity and creates corruption, money laundering, and national security risks. For instance, a 2018 report from the U.S. Department of Defense stated that through such investment strategies, the Chinese government has been able to gain access to numerous cutting-edge, sensitive technologies from U.S. companies, which the department called “the crown jewels of U.S. innovation.”35 Similarly, another report from leading anti-corruption and financial transparency advocacy groups highlighted how municipal governments in China funded numerous Chinese venture capital firms that were then able to invest in sensitive U.S. technology sectors without drawing attention to their government connections.36

Finally, SWF and partner co-investment may present even more of a challenge. The deal in 2016 between the QIA and Glencore helped the two institutions together secure a 19.5 percent stake in Russian oil giant Rosneft for $11.3 billion.37 This investment was designed to give Russia a much-needed cash infusion in response to U.S. and European sanctions on Russia following its 2014 invasion of Crimea, which left the Russian economy and national budget struggling.38 The deal explicitly allowed Rosneft to repurchase the shares and allowed Glencore to purchase 220,000 barrels of oil a day from Rosneft; furthermore, the deal was primarily financed through Russian banks due to the ongoing U.S. and European sanctions.39 In 2017, Glencore and Rosneft sold 14.16 percent of the shares to China’s CEFC energy conglomerate. At the time, the Jamestown Foundation, a leading defense policy think tank, posited that this complex structuring would give China the opportunity to extend its influence over Rosneft, obtain a reliable oil supply that could not be “interdicted by foreign maritime powers,” and strengthen the credibility of the Belt and Road Initiative (BRI).40

The foundation also argued that the deal would give China “a functional (and opaque) way to essentially ‘bribe’ high-level Russian officials with cash that Moscow desperately needs.” Regarding Russia, it further stated that the deal would allow Rosneft, which has close to ties to Putin, to create “shady privatization schemes and what essentially amounts to a sophisticated version of money laundering via VTB.”41 Additionally, it said that the deal would allow Russia and President Vladimir Putin to create close relationships with “opaque business entities that enjoy state support in the Gulf and China.”

SWFs require an army of people to help guide and inform their investment strategies. For example, Norway’s Government Pension Fund–Global, one of the world’s largest SWFs, has a direct staff of more than 500 people from thirty-five countries and operates out of offices in Oslo, London, New York, Singapore, and Shanghai.42 Other smaller or less experienced SWFs may appoint an external investment manager. The chain of actors that help SWFs make investment decisions include the staff of the SWF, financial institutions, various private equity funds, consultants that provide expertise on sector-specific investments, external fund managers, and various other intermediaries vying for a lucrative piece of the SWF pie.

Many worrying patterns of behavior that repeatedly emerge when examining instances of SWF malfeasance and corruption come from weak governance norms that surround these external relationships, such as when private sector entities are either looking to gain the SWF as a client or are responsible for managing the SWF’s investment portfolio. In reading this compilation, the problematic nature of these relationships quickly becomes evident. In the case of the Angolan SWF (see chapter 4), the fund’s asset manager, Jean-Claude Bastos de Morais, advised the SWF to invest in at least four different opportunities where Bastos himself held an interest.43 In another case, the French bank Société Générale agreed to a settlement of 963 million euros ($1.05 billion) with the Libyan Investment Authority (LIA) for allegedly bribing Libyan officials for the chance to manage the LIA’s investments.44

The case studies in this compilation demonstrate that a troubling relationship can exist between corrupt political regimes and private sector institutions that seek to maximize profit or personal gain but may give little consideration to what happens to citizens if the SWF’s resources are lost. However, all of this is not to suggest that external advisers should be disallowed; rather, stronger governance rules both within SWFs and private sector entities are necessary for SWFs to actually benefit from robust, external financial sector expertise.

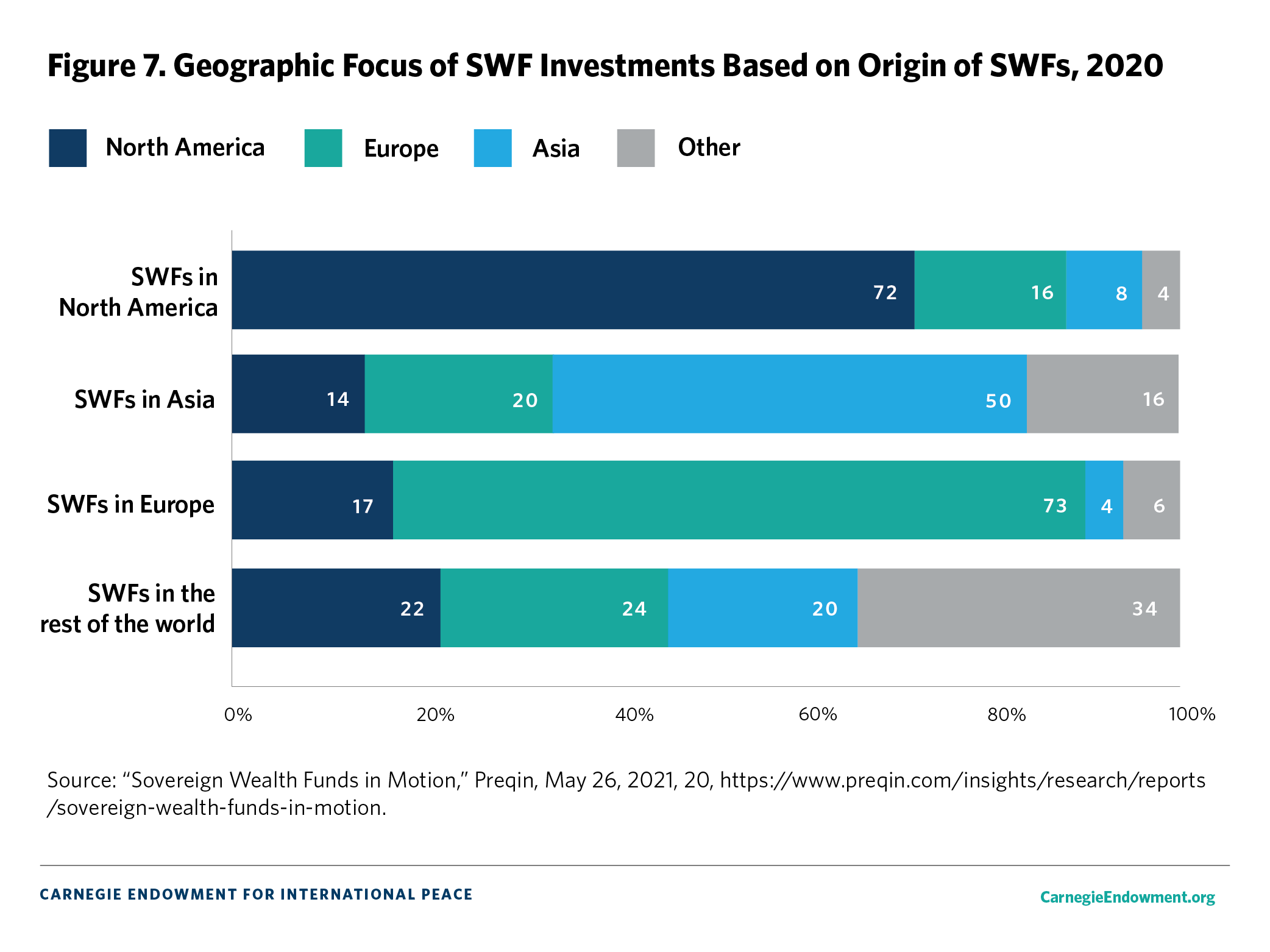

The illicit finance and governance risks within SWFs do not exist in a silo. Almost always, SWFs invest outside their home country. Therefore, understanding where SWFs invest can be valuable in determining how best to address potential governance risks, including risks of corruption and money laundering. A 2021 analysis of a sample of SWF investment patterns found that in 2020–2021, the United States, India, China, the United Kingdom, Singapore, Russia, and Brazil collectively represented the destination for 73 percent of all direct investments. The United States accounted for the largest direct SWF investment at 28.8 percent, followed by India at 14.7 percent and China at 10.5 percent.45

This pattern of investment, however, is only true of direct SWF investments. When including indirect investments, the amount invested in the United States, while significant, is not as large as the investment in the geographic region where the SWF is based. For instance, SWFs based in North America make 72 percent of their investments there, while SWFs in Asia make 50 percent of their investments in Asia and only 14 percent of their investments in North America (see figure 7).

These patterns of investment mean that countries serious about preventing their economies from being used as a conduit or safe haven for the proceeds of corruption and money laundering are in a prime position to scrutinize SWF investments for such risks.

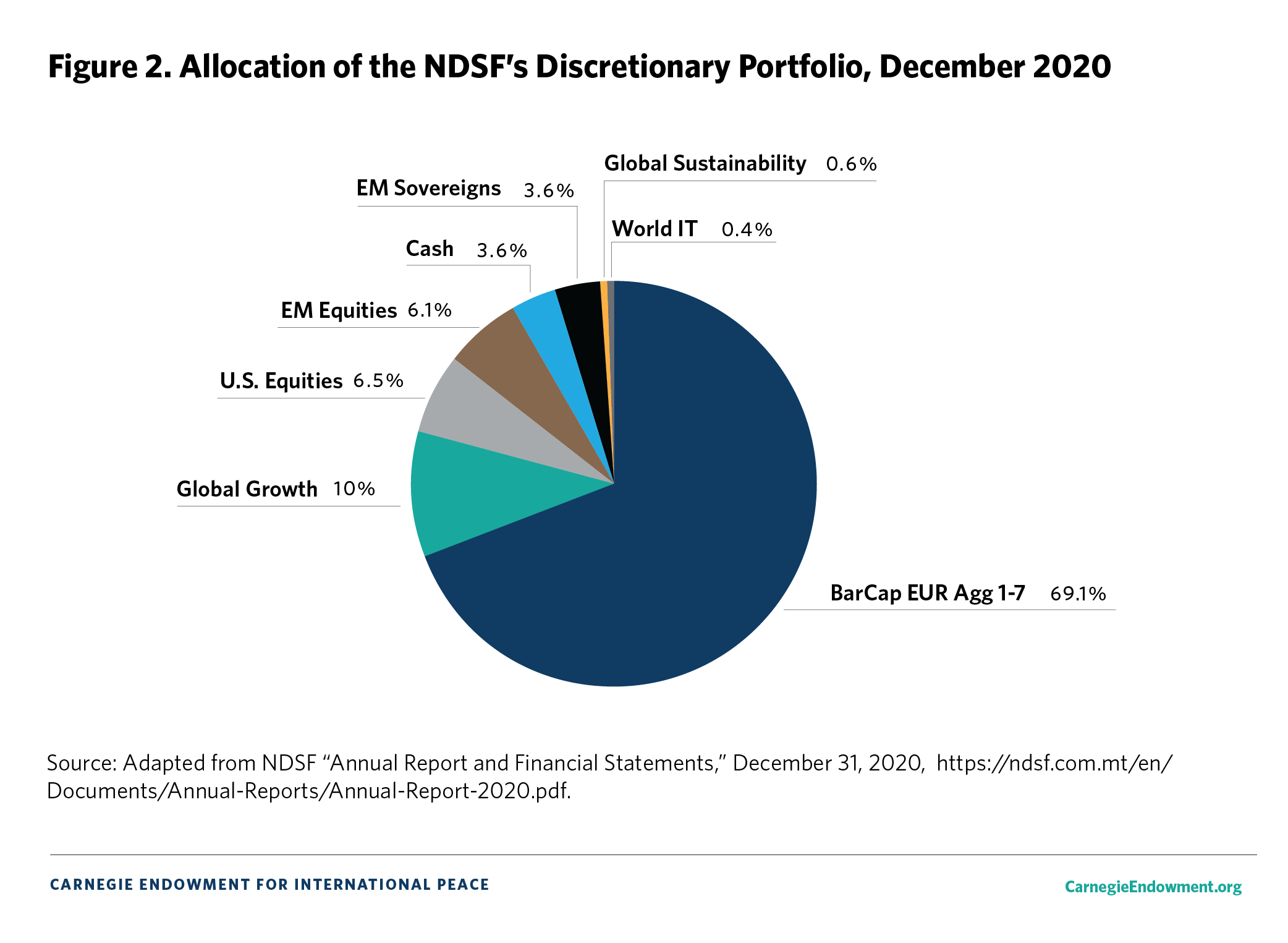

Yet the case studies in this compilation show that despite the corruption, money laundering, and other governance risks associated with this significant pool of capital, SWFs or the legal structures through which SWFs invest appear to face minimal oversight when traversing the international financial system. For instance, as described in chapter 9, there appears to be little scrutiny of the Maltese SWF’s equity and bond investments in the United States as well as in emerging markets, even though that SWF is funded primarily through a controversial citizenship-by-investment program. Likewise, the 1MDB fund discussed in chapter 3 was able to invest in real estate, art, and movies in the United States with minimal scrutiny.

Understanding the nature of existing international standards applicable to SWFs provides much-needed context on how corruption, illicit finance, and other governance risks within SWFs have emerged. The International Working Group of SWFs established the Santiago Principles in 2008 as a result of the tension between maintaining open investment policies in developed economies and protecting against the national security risks that SWF investments bring. The goal was to ensure the “domestic and international legitimacy” of SWFs.46 Today, the group’s successor, the International Forum of SWFs (IFSWF), champions the principles that specifically require SWFs to be transparent, accountable, independent, and commercially oriented.47 While laudable, the principles are not binding and only serve as guiding norms for SWF governance. Moreover, they do not acknowledge that many SWFs operate in environments with high corruption risks and weak rule of law, and they therefore fail to provide any guidance on how best to operate an SWF in such environments.48

The OECD has also provided several guidance documents on SWFs.49 However, to date, all of the documents have been designed to help countries where SWFs invest their funds address the national security concerns that first brought SWFs to prominence.50 These documents and those written by other international organizations such as the World Bank conspicuously shy away from using the term “corruption” in matters relating to SWFs. This is in sharp contrast to their guidance documents on state-owned enterprises—which explicitly address the issue of corruption.51

This fixation with national security has trickled down into domestic legislation. Across both the United States and Europe, numerous laws limit or scrutinize SWF investments for potential national or economic security risks but not for corruption and money laundering risks. A 2009 report from the U.S. Government Accountability Office laid out the various national security restrictions in place across sectors, including transportation, technology, communications, national security, and energy (including nuclear energy). However, neither the report nor any subsequent public U.S. government agency report has dealt with the danger that SWFs could use the United States as a money laundering conduit or a destination for corrupt funds.52

In the absence of binding international standards, greater transparency through public information disclosure would help ensure accountability and reduce the risks of corruption and other types of illicit finance. This is a model particularly favored by the extractives sector to reduce corruption and associated money laundering risks. In many countries, foreign aid and investment into the extractives sector is contingent on meeting standards set forth by the Extractives Industries Transparency Initiative, the Open Contracting Partnership, and other similar efforts.53 However, SWFs have thus far largely succeeded in keeping their operations and investments shrouded in secrecy. Exceptions like Norway’s Government Pension Fund, which has robust transparency and disclosure practices, have not shifted the overall SWF culture toward transparency. Gaps in transparency and data limit the ability of researchers and governments to better capture and track corruption and money laundering in SWFs (see chapters 2 and 12).

Finally, in the absence of clear regulations, industries often set up self-regulatory bodies to ensure standards and good governance. The IFSWF is the closest organization that exists to fulfilling that role for sovereign wealth funds. The organization was incorporated in 2014 to strengthen the SWF “community through dialogue, research and self-assessment.”54 The IFSWF model permits members to self-assess the robustness of their governance standards. Needless to say, this has not created the necessary incentives for SWFs to critically examine their operations. Several funds mentioned in this report are IFSWF members and have given themselves strong self-assessment scores despite the publication of news stories that raise legitimate concerns about the operations of these funds. An analysis of IFSWF members’ and associate members’ CPI scores reveals that a significant number of SWFs operate in corruption-rich environments (see figure 8). It thus remains an open question whether IFSWF membership provides some of these funds, whose behavior may raise red flags, a reputational benefit and added credibility.

Against this backdrop, the eleven chapters in this compilation examine specific cases that demonstrate SWFs’ susceptibility to corruption, money laundering, and other governance issues and the enabling environment that stymies efforts at detection and public oversight.

Chapter 2 further describes the potential corruption risks associated with SWFs, including how the current voluntary standards fall short. It also documents how the lack of free, publicly available data on SWFs prevents oversight and accountability by governments, civil society, and the media. It notes that the opacity of SWFs can lead to fears that funds are being used for political goals or being co-opted, rather than being used for their stated purpose.

Chapter 3 describes one of the most famous and egregious examples of corruption associated with SWFs: the so-called 1MDB scandal. 1MDB was a sovereign development fund intended to improve the infrastructure and investment environment of Malaysia. Instead, $4.5 billion was siphoned off by senior Malaysian elites, politically connected individuals, and bankers to purchase everything from yachts to art to real estate. This case thus provides a model for how SWF-associated corruption and money laundering schemes can work and how their financial complexity can enable corruption and other malfeasance to continue for years largely undetected.

As noted in this introduction chapter, states have traditionally used SWFs to diversify the proceeds from natural resources and ensure that the proceeds can be saved for future generations. Chapters 4 and 5 highlight potential governance risks associated with natural-resource-based funds. In the case of Angola in chapter 4, a highly autocratic regime used its control over the government to divert oil funds to relatives and friends of the president, even though at the time it was ranked as having relatively good SWF governance by various indices. The Angola case also highlights how reforms can create cleaner and more resilient SWFs.

The case of Equatorial Guinea in chapter 5 then describes how an extreme lack of available information about SWF activity increases the risks that money will be illegally diverted. The well-documented grand corruption associated with the country and the fact that the oil—upon which the country’s export revenue depends—is due to begin to run out within a decade heighten the need for the highest levels of transparency and good governance of the SWF to be instituted in a most timely manner.

Chapter 6 further describes Saudi Arabia’s PIF, one of the world’s largest SWFs. The PIF, and especially its associated Vision 2030 fund, has been used to acquire world-famous sports teams and even establish an entirely new golf franchise through its pact with the PGA, giving Saudi Arabia significant control over the elite-level tournaments associated with an entire sport. Such investments provide a means for authoritarian leaders such as Saudi Crown Prince Mohammed bin Salman to launder their reputations through sports using the proceeds of their country’s natural resources.

Even SWF funds disbursed to help in an emergency like the coronavirus pandemic are not immune from allegations of diversion and corruption. Chapter 7 describes how Russia’s leadership gave the funding for and marketing of Russia’s Sputnik V COVID-19 vaccines to the Russian Direct Investment Fund (RDIF), an unusual form of SWF. The chapter describes how the RDIF forced some countries to purchase Sputnik V vaccines through a series of shell companies that eventually raised the price to double what it should have been.55

SWFs are usually established to invest and diversify a country’s natural resource wealth, but some countries establish their SWF via loans or taxpayer funds from the state budget instead. This means that such funds can become a parallel budget that is out of reach of oversight by parliaments and citizens, as illustrated by the case of Türkiye’s SWF in chapter 8.

Scholars and policymakers have long worried that China’s BRI is a mechanism for opaque deals designed to help China further its global ambitions, especially through so-called debt-trap diplomacy. Chapter 9 describes how Chinese SWFs undergird the BRI, providing funds to help enable the BRI’s overseas investments.

One of the more unusual means of funding a state’s SWF is covered in chapter 10 and features Malta’s SWF. The country uses the proceeds from the sale of Maltese visas and citizenship—so-called golden visas and golden passports—to fund its SWF. Numerous investigations by the European Union (EU) and investigative journalists have documented that this has enabled some corrupt and criminal actors to receive EU residency and/or citizenship and the benefits that go with it. Such funding can create a conflict of interest for Malta because tightening its residency and citizenship requirements could undermine its SWF.

A few countries use the international arms trade to help fund their SWFs, most notably the UAE. One of its most famous SWFs, Mubadala, was founded with money from side contracts for arms purchases from Western defense firms. The arms sector is notoriously fraught with corruption, and the extreme opacity of defense procurement contracts carried out through the veil of sovereign wealth funds makes accountability even more difficult. Because these SWFs are associated with the arms trade, their activities can also have larger ramifications for peace and security, as chapter 11 describes.