Commentary

As the monarchy appears to question its grandest projects, the state could do with more critical debate than rote cheerleading.

Andrew Leber

{

"authors": [

"Yukon Huang",

"Jeremy Smith"

],

"type": "legacyinthemedia",

"centerAffiliationAll": "dc",

"centers": [

"Carnegie Endowment for International Peace"

],

"collections": [],

"englishNewsletterAll": "asia",

"nonEnglishNewsletterAll": "",

"primaryCenter": "Carnegie Endowment for International Peace",

"programAffiliation": "AP",

"programs": [

"Asia"

],

"projects": [],

"regions": [

"North America",

"United States",

"East Asia",

"China"

],

"topics": [

"Economy",

"Trade",

"Foreign Policy"

]

}

Source: Getty

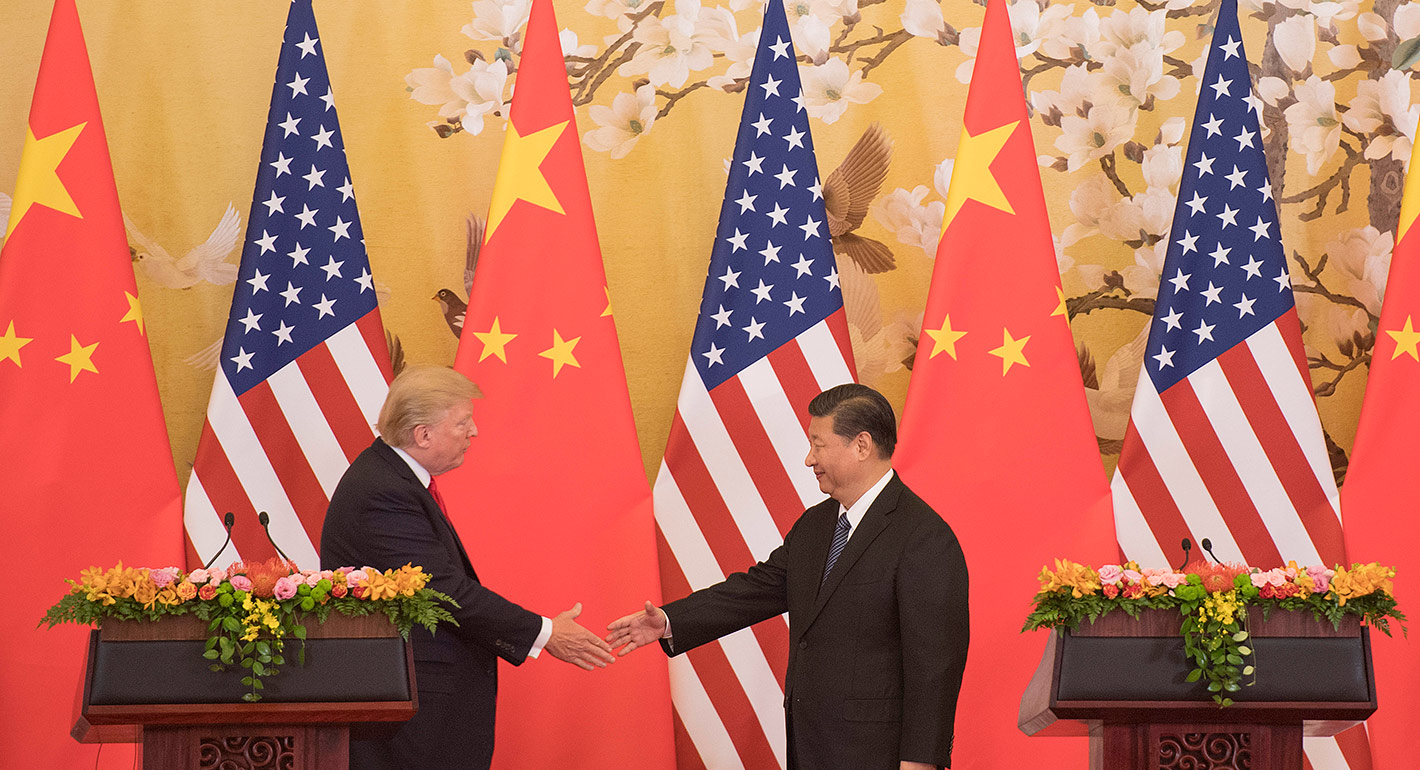

The U.S.-China trade deal undermines the interests of the broader global community in favor of the arbitrary whims of great powers. When it all falls apart—and takes out remaining parts of the current trade order with it—even Trump may find that the United States is worse off.

Source: Foreign Policy

Soon after U.S. President Donald Trump and Chinese leader Xi Jinping announced a phase one U.S.-Chinese trade deal in late December 2019, relief was palpable. Pundits looked forward to the return of some semblance of stability and quickly jumped on who had won and who had lost. And the winners seemed plentiful enough; the global business community generally welcomed a “truce” that moderates tariff-based uncertainties, keeps stock markets at historic highs, and promises reforms in China’s foreign investment regime. The agreement also appeared to meet the near-term political needs of Trump, who faces an upcoming election, and those of Xi, who wants to moderate economic risks while trying to strengthen the role of the Communist Party.

Yet in the long term, the deal may have more losers than meets the eye. Any violation of the agreement’s commitments would trigger an unusual dispute resolution mechanism that might ultimately destroy the rules-based international trading system created and nurtured by the United States over the past century.

Some skeptical observers have noted that the deal leaves in place most of the trade-war tariffs that continue to burden both consumers and producers. There are also concerns that major issues in the trade relationship, such as the role that state enterprises and subsidies play in China’s economy, are being pushed off for future discussions. But a more fundamental problem is that the framework for this deal is conceptually flawed, which will result in unrealistic expectations and unfulfilled commitments.

The problem begins with Trump’s ill-advised obsession with trade deficits. The United States runs deficits with over 100 countries, but China accounts for the biggest share. A key aspect of the deal is China’s obligation to increase purchases of U.S. goods and services to $200 billion above 2017 levels over the next two years (a 92 percent increase in covered products). Fulfilling this pledge will rely on state-managed purchases—in violation of globally accepted practices, which stipulate imports and exports should be primarily shaped by the market-based decisions of firms and consumers.

Beyond that, the countries’ bilateral import commitments ignore the fact that trade outcomes really rest on multilateral relationships. The agreed targets for increased purchases of agricultural products, for example, suggest that China might have to buy considerably less agricultural products from Brazil. Others indicate that it might have to purchase far fewer planes from Airbus than under normal market conditions. Such arbitrary adjustments will distort global markets. The deal may lower the United States’ trade deficit with China, but it will largely be offset by higher deficits with other countries. The diversion also contravenes World Trade Organization (WTO) guidelines and will inevitably drag affected parties into a complex litigation process that in all likelihood will lead to the deal being abandoned.

Another problem underlying the agreement is the assumption that technology transfer and intellectual property protections are the basis for U.S.-Chinese great-power competition, when in reality they are global developmental issues. There is no dispute, of course, that practices bordering on outright theft of intellectual property should be eliminated, and the agreement does include provisions outlawing China’s requirement of technology transfer as a precondition for market access. Foreign investors have long found this demand to be onerous, but it has come under harsher scrutiny recently as a result of raging technological competition between the United States and China. U.S.-Chinese tech tensions have distracted from the fact that foreign direct investment has long been a key conduit for technology transfer to developing countries.

In China, the primary vehicle for such transfers has been the requirement that foreign investors form a joint venture with a domestic company as a condition for accessing the Chinese market. China is by no means unique in this regard, and it generally supports the principle that such arrangements should occur “on voluntary, market based terms” as stated in the text of the agreement. Yet just because such requirements are not limited to China does not mean that they are permissible, but it does mean that the issue should be settled in multilateral venues rather than through ad hoc bilateral agreements.

On intellectual property, the trade agreement mandates that China issue an “Action Plan” within 30 working days enumerating “measures that China will take to implement its obligations … and the date by which each measure will go into effect.” For U.S. negotiators, this commitment is meant to foil any plans for China to “[steal] its way up the economic ladder” at the United States’ expense. Curbing China’s prolific intellectual property theft would be a welcome change, but, as we have argued previously, a country’s stance on intellectual property protections is a product of its domestic innovative capacity and overall developmental stage. Emerging economies seek to promote the inflow of knowledge through a variety of means, while developed economies argue for safeguarding the incentive to innovate. These trade-offs apply to everyone, and general principles for best practices are already enshrined in the TRIPS Agreement, which China consented to follow as part of its 2001 WTO accession.

Many observers point out that China has failed to honor its previous commitments and use this as justification for Trump’s more punitive measures. Others raise doubts about the implementation of China’s new Foreign Investment Law, which in principle already banned forced technology transfer and strengthened intellectual property protections. For this reason, the key to the phase one deal is its dispute resolution framework, which U.S. Trade Representative Robert Lighthizer promised would have “real teeth.” This framework is also crucial given the virtual inevitability of a violation, which would most likely result from China’s failure to meet such ambitious purchasing targets.

Yet under the terms of the appeals process, any decision is quickly elevated to Lighthizer, who has stated that “the only arbitrator I trust is myself.” If he and the Chinese vice premier, who would handle disputes on the Chinese side, cannot come to terms, the United States is allowed to adopt “a remedial measure”—likely tariffs. If China judges such measures to be “taken in bad faith,” its only recourse will be to withdraw from the agreement.

If an infraction occurs, the greatest hope for the agreement’s survival would be a political calculation by Trump that triggering a withdrawal would risk his deal being exposed as a failure too close to the election. Senate Minority Leader Chuck Schumer has loudly criticized the agreement for being too weak, and Trump will not want to give that view any credence.

This is a deal uniquely of Trump’s design: It represents a complete rejection of an international arbitration process in favor of concentrating bargaining power and judicial authority in the hands of his closest advisors. Trump’s brand of economic statecraft—one in which unilateral tariffs and sanctions supersede established global norms and principles—has dealt a damaging blow to the global trading and foreign investment system. His latest move reinforces the White House’s ongoing efforts to weaken the WTO by refusing to staff its appellate body, which arbitrates disputes. Meanwhile, the phase one deal prescribes state-managed trade over market forces, discourages international knowledge and technology flows, and hinges on a bilateral dispute resolution process that will likely be the deal’s undoing.

This deal undermines the interests of the broader global community in favor of the arbitrary whims of great powers. When it all falls apart—and takes out remaining parts of the current trade order with it—even Trump may find that the United States is worse off.

Senior Fellow, Asia Program

Huang is a senior fellow in the Carnegie Asia Program where his research focuses on China’s economy and its regional and global impact.

Jeremy Smith

Former James C. Gaither Junior Fellow, Asia Program

Jeremy Smith was a James C. Gaither Junior Fellow with the Asia Program.

Carnegie does not take institutional positions on public policy issues; the views represented herein are those of the author(s) and do not necessarily reflect the views of Carnegie, its staff, or its trustees.

As the monarchy appears to question its grandest projects, the state could do with more critical debate than rote cheerleading.

Andrew Leber

After spending much of 2025 trying to placate Donald Trump, some European leaders are starting to change posture. But is even a hostile Washington still so important to Europe that the U.S. president’s outbursts are worth putting up with?

Rym Momtaz, ed.

Instead, governments should adopt climate-friendly measures to address the impact of rising prices.

Henok Asmelash

If U.S. policymakers continue down the path of restricting China’s access to frontier AI, they will eventually have to implement some sort of restriction on cloud access.

Noah Tan

European leaders have now not only lost faith in Donald Trump’s U.S. presidency, but also in America’s hegemony as a whole. But short-term challenges make an immediate divorce unwise.

Rym Momtaz