Paper

Milo McBride

Source: Getty

Chinese companies are dominating the production of technologies essential for a clean energy future. The United States should embrace innovation to preserve its future energy security.

The following working paper is in support of the Carnegie Endowment for International Peace’s U.S. Foreign Policy for Clean Energy Taskforce, a nonpartisan working group seeking to bolster U.S. clean industrial goals with cooperative decarbonization abroad.

Over a decade ago, U.S. policymakers lamented a new kind of Sputnik dilemma: Chinese companies could dominate the production of technologies essential for a clean energy future, leaving U.S. industry playing catchup.1 Today, such alarms ring loudly. Chinese firms produce nearly 60 percent of electric vehicles (EVs), 70 percent of wind turbine nacelles, and 80 percent of solar modules, battery cells, and key processed minerals, and they have a significant lead on new nuclear power and green hydrogen.2 This degree of geographic concentration surpasses modern analogs: even at the height of the Organization of the Petroleum Exporting Countries, the oil cartel supplied just over half of the global crude market.3 And yet China’s deployment of these technologies is promising news for the objectives of wrangling carbon emissions by narrowing some global manufacturing gaps to reach net-zero goals and of prompting the world’s largest net emitter to potentially plateau emissions in 2024, six years ahead of Beijing’s stated plans.4 But in the long term, Chinese products flooding the global market risk rendering the United States a hydrocarbon superpower in an era moving toward minerals, machinery, and electrons.5 Clean energy systems are not merely keys to a stable climate; they are geostrategic products that will define the future of industrial and technological power.

While the United States has responded to this challenge with unprecedented industrial policy, many of these policy incentives have sought to recreate the vast supply chains that Chinese firms continue to dominate; since the launch of Western green industrial efforts, some of Beijing’s mineral and clean tech lead has only increased.6 Building on this industrial strategy, the United States—in conjunction with its allies—should concentrate on accelerating leapfrog technologies capable of circumventing present supply vulnerabilities and drive cost-competitive alternatives in less saturated sectors. While Washington’s unleashing of subsidies and tariff hikes could arguably be necessary first steps to incubating a domestic industrial base, they risk technological complacency and do not guarantee that U.S. firms will innovate, let alone leap ahead. Recent innovation policy developments are a clear step in the right direction, but going forward, they should be prioritized and accelerated. If the United States is to genuinely embrace industrial policy as its direction of travel, then innovation should be a central tenet—not a peripheral consideration. To do so would preserve the United States’ role in future energy security while fostering a U.S.-China relationship more beneficial to climate mitigation: one of competitive cooperation in lieu of industrial mercantilism.

The United States is well-positioned to rise to the challenge. The nation already hosts a rising new industrial base in sectors including advanced batteries, geothermal energy, grid and storage technologies, as well as low-carbon heavy industry. Across these industries, start-ups are raising institutional investment and leveraging domestic know-how in areas like nanotechnology and oil and gas drilling to advance new processes that could put U.S. industry at the frontier of some clean energy markets. Future policy should capitalize on these strengths and focus on technologies that offer scalability with existing labor forces, material reduction with resilience implications, and opportunities of comparative strength to develop globally competitive, low-carbon industries. But many of these technologies will not leap into the market on their own: they will require further efforts to derisk investment and drive next-generation advancements to compete with established products—both at home and abroad. The rest of this piece examines the strategic value of emerging energy systems and industrial processes and then investigates domestic and international incentives for their deployment.

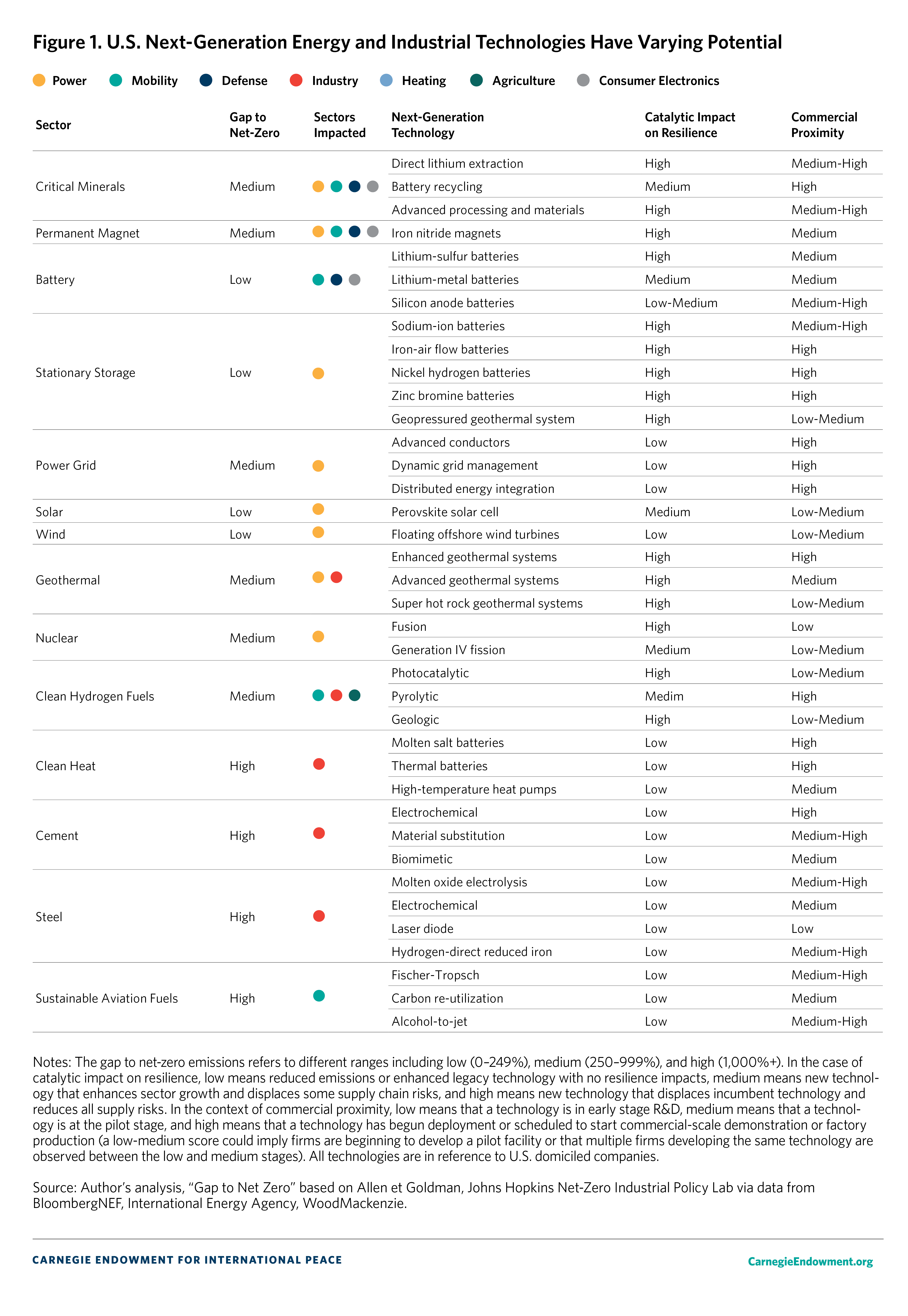

New technologies domiciled in the United States have the potential to alter dynamics in clean energy and traditional industrial sectors (see figure 17). One baseline metric is the gap between a sector’s current production levels and what levels are needed to achieve global net-zero emissions by 2050, where a low gap would imply that goals are within reach and a high gap signifying a significant distance. Of core importance are next-generation systems that can displace an incumbent technology and its supply risks; lesser importance is assigned to technologies that enhance a potential market or simply reduce carbon emissions from an industrial process that can be reliably produced in the United States with conventional fuels. Lastly, the analysis includes an estimate of how close that technology is to being commercialized. All these U.S.-domiciled technologies are being developed by companies that have raised at least series A equity or that are part of a prominent corporation. The list is non-exhaustive and does not include enabling technologies to enhance manufacturing of incumbent systems aside from some in the critical minerals sector that offer impactful breakthroughs for chemical production. Further, this research does not claim that these technologies are destined for commercial viability; however, it maps how and where they could prove leverageable to support domestic resilience and competitiveness, as well as global climate goals.

These technologies have different degrees of importance that indicate where opportunities and strategic gains could emerge. For example, a low gap to net-zero emissions, as seen with solar technologies and batteries, implies that Chinese production capacity is already highly saturated, meaning that correlated leapfrog opportunities would prioritize domestic supply resilience, not necessarily climate goals (although both advanced batteries and solar could yield positive and unforeseen energy transition impacts). Other sectors like hydrogen, nuclear power, geothermal, permanent magnets, and critical minerals have moderate gaps to net-zero production but also yield varying degrees of high potential to displace legacy systems and unlock new sources of clean power, heat, fuels, and products. The hard-to-abate sectors like cement, steel, and aviation fuel present high gaps to net-zero goals but with low implications for resilience. US domiciled technologies that have a higher proximity to commercialization—such as advanced grid, storage, heavy industry, mineral processing, and some geothermal—require market incentives to help their pathway to adoption. Those that rank low to medium on proximity to commercialization—including advanced solar cells, nuclear reactors, and some next-generation hydrogen and geothermal techniques—will require policies like funding for R&D and piloting.

Batteries and magnetic motors are decisive technological frontiers for energy security. They are key demand drivers for critical minerals and essential elements of products like EVs, consumer electronics, robotics, and defense systems. Given these widespread applications, they are the most consequential energy transition technology for macroeconomic stability and national security, but both come with severe U.S. supply chain risks. Magnetic motors require rare earth oxides and lithium-ion batteries require spherical graphite, China’s most significant mineral choke points and targets of Beijing’s export controls.8

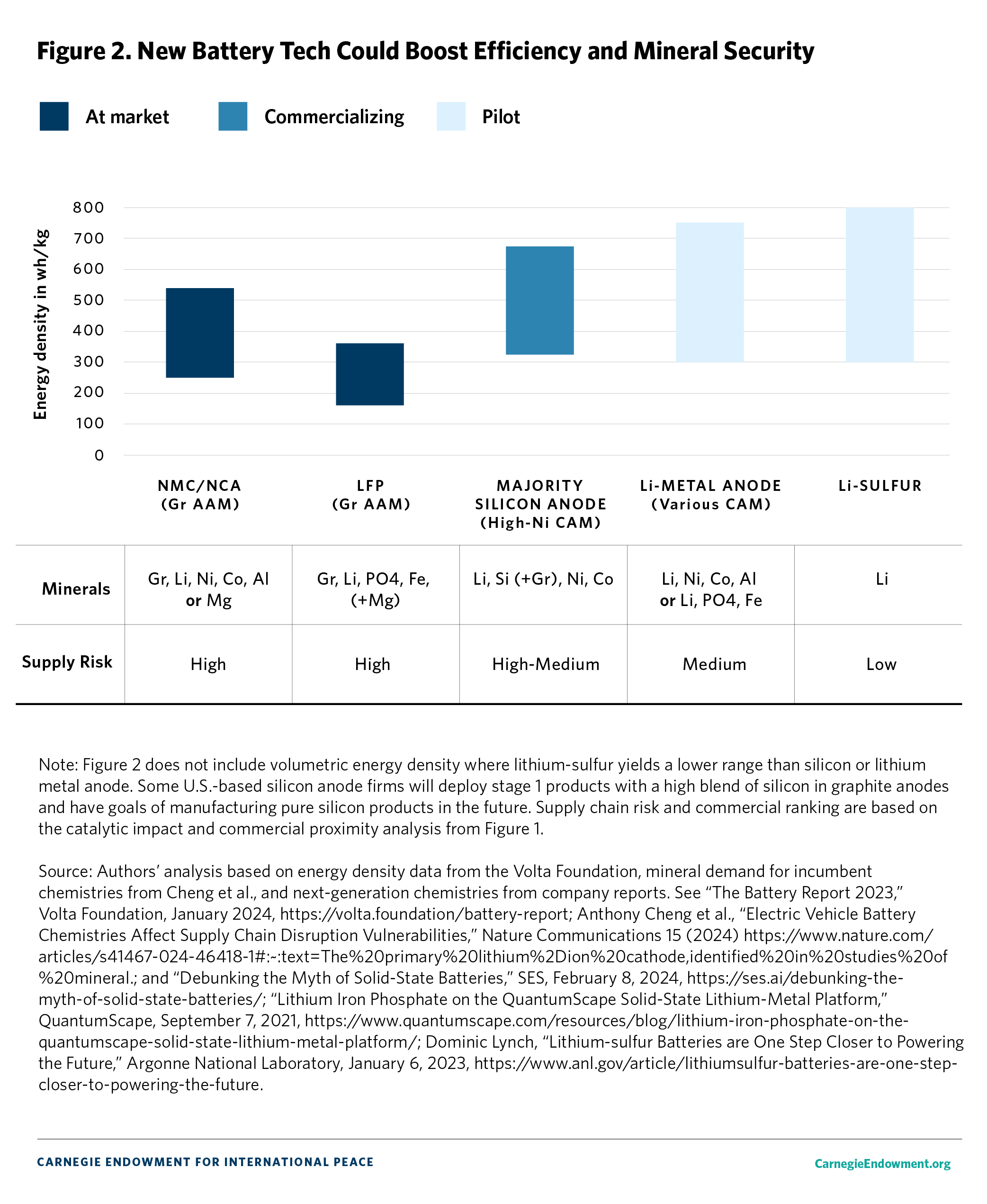

Some U.S. companies are working to circumvent these risks by developing batteries and magnets that do not require these geopolitically precarious minerals. One U.S. company developing magnets without rare earth elements is piloting its technology, while other, earlier-stage start-ups have yet to raise the investment that would qualify for this analysis.9 Multiple battery firms are working to replace graphite from lithium-ion batteries—the largest component by volume of the battery—with more resilient materials that can support a greater driving range.10 Firms using silicon-graphite blends and eventually pure silicon to replace graphite likely lead on commercialization, but those using lithium metal could yield the highest impact on resilience and the greatest cost reductions. In cases like lithium-metal sulfur batteries, lithium is the only critical mineral required which reduces material expenses and geopolitical risks (this specific breakthrough technology is in the early stages of research in Chinese labs and is a unique area of potential U.S. technological advantage).11 In either case, some silicon and lithium-metal designs can utilize existing battery factory machinery that could expedite pathways to commercialization.12

U.S. battery technology is well positioned to leap ahead. By 2030, Chinese industry is expected to retain two-thirds of incumbent battery production but only control one-third of these next-generation technologies - providing an opening to increase US market share of new chemistries.13 These dynamics have not gone unnoticed. Recently, Beijing issued new funding for next-generation batteries while Chinese industry has formed a collaborative between industry, government, and researchers to advance these technologies.14 Such an opportunity and subsequent policy responses from China reinforce why it is important that the United States focus on the next generation of products where its industry stands a chance at competing, especially on batteries that mitigate China’s mineral lead (see figure 2).

This shift toward lithium-metal batteries could be reinforced by the United States’ emerging ability to produce lithium—an example of the types of next-generation technologies in the critical minerals sector, the backbone of the energy transition. The United States is well-positioned as a leader in direct lithium extraction, which efficiently separates lithium from oilfield brines, geothermal plants, and salt flats. With direct lithium extraction in the United States getting underway, some facilities were backed by government funds while others were the result of an industrial synergy between oil and gas, geothermal, downstream chemical, and legacy lithium producers.15 Further downstream, multiple start-ups are pioneering techniques to process minerals and produce materials more effectively without the toxicological and hydrological costs associated with refining. While these systems offer an avenue to leap ahead of China’s mineral processing technology, they are starting to advance from the pilot stage, and some of them are struggling to scale amid challenging financial conditions and a lack of market structures that internalize their sustainable added value.16 The nation is following in China’s footsteps by developing battery recycling hubs, but these systems will only be complementary to the world’s ever-growing mineral demand and will not impact primary supply until the 2040s.17 For many energy transition metals like copper, zinc, silver, and nickel, there is no supply-side, leapfrog solution to supersede mining.

Despite the nation’s lagging deployment of new transmission lines and production for grid equipment like transformers, U.S. industry is well-positioned in technologies for advanced power grids and energy storage that will propel long-term electricity decarbonization and stability.18 An array of companies will soon start mass-producing batteries for grid storage without the aforementioned metals and with significantly higher storage times; conventional lithium-ion batteries can economically store four to six hours of power, while these new systems offer twelve hours—if not days—of storage capacity.19 Some of these storage systems could prove competitive against incumbent lithium-ion technologies in particular markets.20 An impressive roster of firms can enhance the capacity and effectiveness of the power grid itself by upgrading power lines, implementing advanced monitoring systems, and connecting smart-grid software for end users. While these technologies offer low catalytic resilience to replace the incumbent grid system, they promote domestic energy security through grid stability amid increasing climate stress, variable load, and growing power demand. 21 Although Chinese firms are also developing long-duration energy storage and advanced grid systems, U.S. industry’s competitiveness could be undervalued—especially in countries that share security concerns with having a Chinese presence in their domestic critical infrastructure.22

A strong array of U.S. firms are developing next-generation technologies in the solar, wind, and nuclear sectors. Although these technologies could deliver varying degrees of importance for resilience and domestic energy transition goals, many are just beginning the pilot stage and may struggle to catch up, let alone compete, with Chinese industry in the global market. Solar photovoltaics are the fastest growing energy source globally and in the US, presenting substantial long-term potential.23 Several start-ups and US solar manufacturers are developing perovskite solar cells—a highly efficient next-generation technology poised to lower costs and expand deployment.24 But their market adoption is unlikely to displace conventional solar cells, as the technology will need to be integrated with conventional panels, limiting its leapfrog potential.25 Further, U.S. industry is just beginning to pilot this technology and could face significant challenges competing against Chinese industry’s dominance in perovskite patents, its lead on developing perovskite factories, and unparalleled stature in conventional solar manufacturing.26

There are no observed leapfrog technologies for the incumbent onshore wind turbine, but about two-thirds of the nation’s offshore wind potential could come from turbines in deep waters, known as floating offshore wind turbines.27 While there are multiple U.S. start-ups beginning to pilot innovative techniques to deploy floating offshore wind, the U.S. offshore wind industry is still nascent compared to those in Europe and China and has been struggling to get off the ground.28 Although these systems can help decarbonize certain parts of the country, they yield little opportunity for resilience or competitiveness; floating offshore technology will require new infrastructure and will not be an area where U.S. industry can compete globally. World-leading Chinese wind players are already developing commercial floating projects at home with plans to expand in Europe, a historical leader of offshore wind development.29 These challenges are furthered by recent price trends of Chinese turbines being sold at increasingly lower cost than Western competitors.30

A similar and perhaps more severe dynamic is emerging in the nuclear sector. Even with nonpartisan fiscal and regulatory support from Washington, next-generation nuclear reactor designs, including small modular reactors, are still at a nascent stage and are unlikely to come online until the 2030s in the United States, despite a world-leading roster of new reactor designs by U.S. firms.31 By contrast, the Chinese began operating a small next-generation reactor in 2023 and are expected to begin commercial power generation from a second small modular reactor in 2026.32 Currently, Chinese industry is constructing the largest share of the world’s new reactors to satisfy domestic energy demand and will continue to pursue exporting its technology abroad.33 The strength of Chinese industry and its supply chains will make it difficult for the U.S. nuclear industry to compete, apart from foreign markets with aligned security interests (albeit on long-term time horizons).34 Further, it remains unclear if next-generation reactors are the industry’s technological future; many new reactor designs will require higher levels of enriched uranium fuels and robust levels of standardization to achieve economies of scale.35 Fusion technology is further from commercialization, but is perhaps an area of parity between the United States and Chinese R&D, though the technology remains difficult to gauge over the long term.36

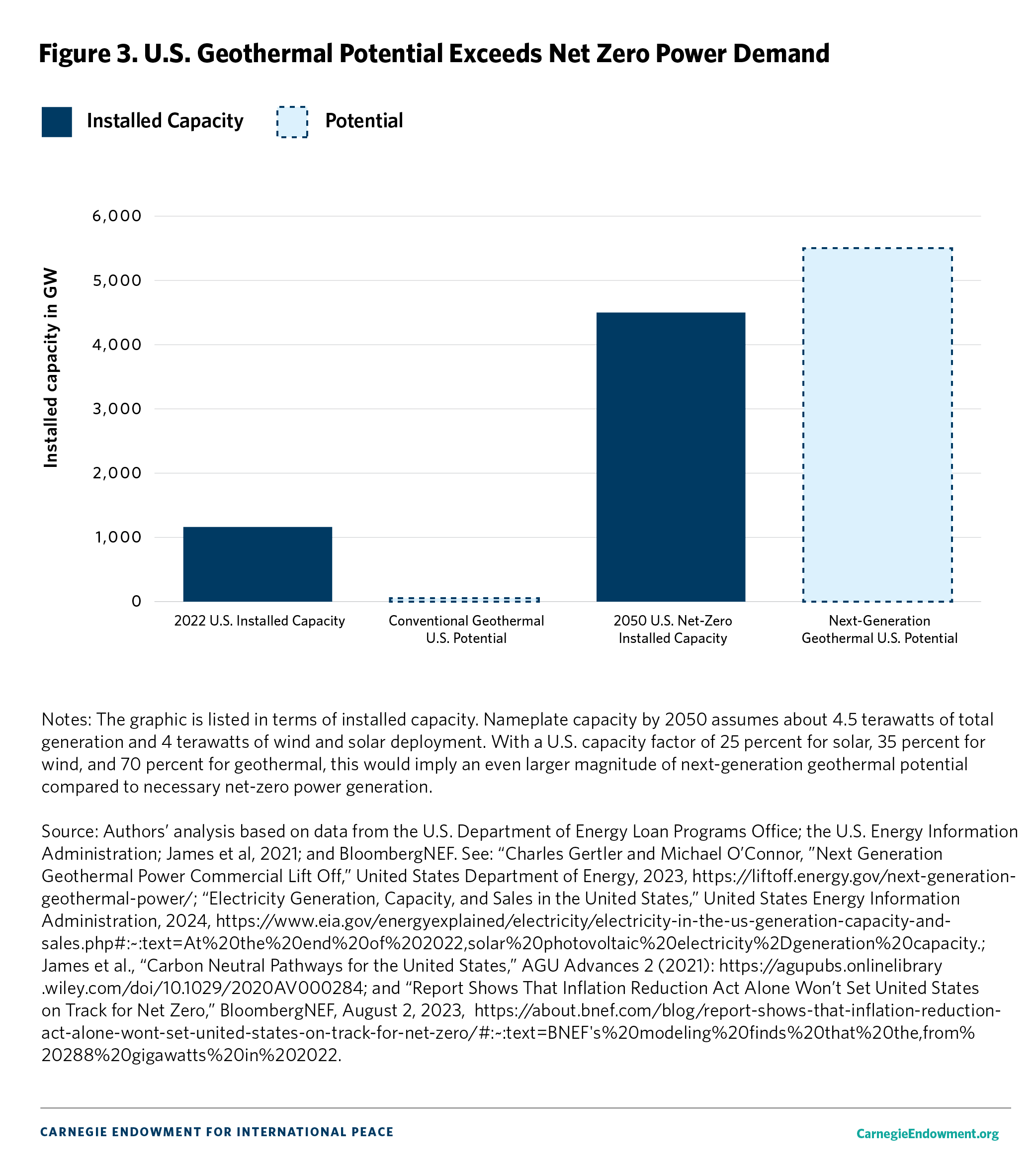

Conversely, geothermal energy is the decisive sector where the United States can leapfrog ahead in the race for new power generation. Geothermal energy (extracting heat from the earth’s crust) was once constrained by limited access to high-temperature underground fluids, but today those barriers are breaking. U.S. oil and gas engineers have pioneered two new techniques to provide 24/7 clean power and expand national geothermal power generation potential 140-fold—roughly five times the nation’s entire installed power generation today (see figure 3).37 Over the long term, these systems will support decarbonizing the remainder of the power grid by offering flexibility to adjust output as needed alongside variable renewable energy sources.38 But in the near term, they are being deployed to power data centers as well as future projects for direct air capture facilities and U.S. military bases.39 Most importantly, the United States is home to a world-leading workforce and drilling service industry capable of rapidly scaling this technology, some of which are already cutting costs at faster rates than observed in the wind and solar sectors—which have yielded transformative cost reductions.40 Despite some geothermal developments from a Chinese state-owned oil firm, the U.S. industrial advantage in drilling positions next-generation geothermal energy as an area where the United States can prove competitive globally. 41

U.S. technology is strategically positioned to decarbonize heavy industry, an asset to net-zero and climate leadership. Heavy industry—including the production of steel, cement, and chemicals—represents about one-third of global emissions, and those emissions are at risk of increasing amid positive decarbonization trends in the transportation and power sectors.42 Despite this concerning outlook, some U.S. start-ups are developing new disruptive processes to produce low-carbon steel, cement, and chemicals. Other U.S. technologies decarbonize industrial heat through the likes of thermal batteries or high-capacity heat pumps. The United States will continue to be the global leader in carbon capture technology, which is increasingly utilized in the industrial sector, but no new leapfrog techniques were observed beyond incumbent solvent and sorbent processes (which have been regularly utilized and have failed to deliver cost-cutting results).43 Industrial decarbonization technologies pose the opportunity to corner export markets with carbon tariffs and diffuse these systems to developing countries with relatively low manufacturing costs but high risks of growth in industrial emissions. While clean industrial processes entail cost premiums that require support in their journey to market, U.S. industry actors are well-positioned compared to China. China only recently outlined industrial decarbonization goals and began hydrogen-based low-carbon steel projects, but is unlikely to possess the arsenal of analogous next-generation processes.44

To feed the production of low-carbon steel, fertilizer, chemicals, and sustainable aviation fuels, the United States could unlock new sources of hydrogen fuels. Tomorrow’s hydrogen economy will require clean and cheap molecules, but today’s hydrogen processes are far from that goal. Hydrogen from renewables uses large quantities of electricity to produce a high-cost product, while hydrogen from natural gas struggles to sufficiently abate emissions.45 One already-operational solution uses controlled heat to cleanly extract hydrogen from methane gas, producing EV tires as a bonus biproduct (similarly, one start-up is seeking to produce graphite for EV batteries as a biproduct).46 Other firms are taking a wildcat approach by drilling the earth for deposits of hydrogen, which (if viable) could yield abundant and low-cost products.47 Although the United States and Europe maintain some global electrolyzer production—the incumbent machinery used to produce green hydrogen from renewables—China’s low-cost electrolyzers have left European industry in a panic over a potential future flood of cheap products.48 To leapfrog over electrolyzers, some industry actors are researching techniques that split water into hydrogen using direct sunlight without renewables or associated machinery, but it remains unclear if this process will deliver commercial results.49

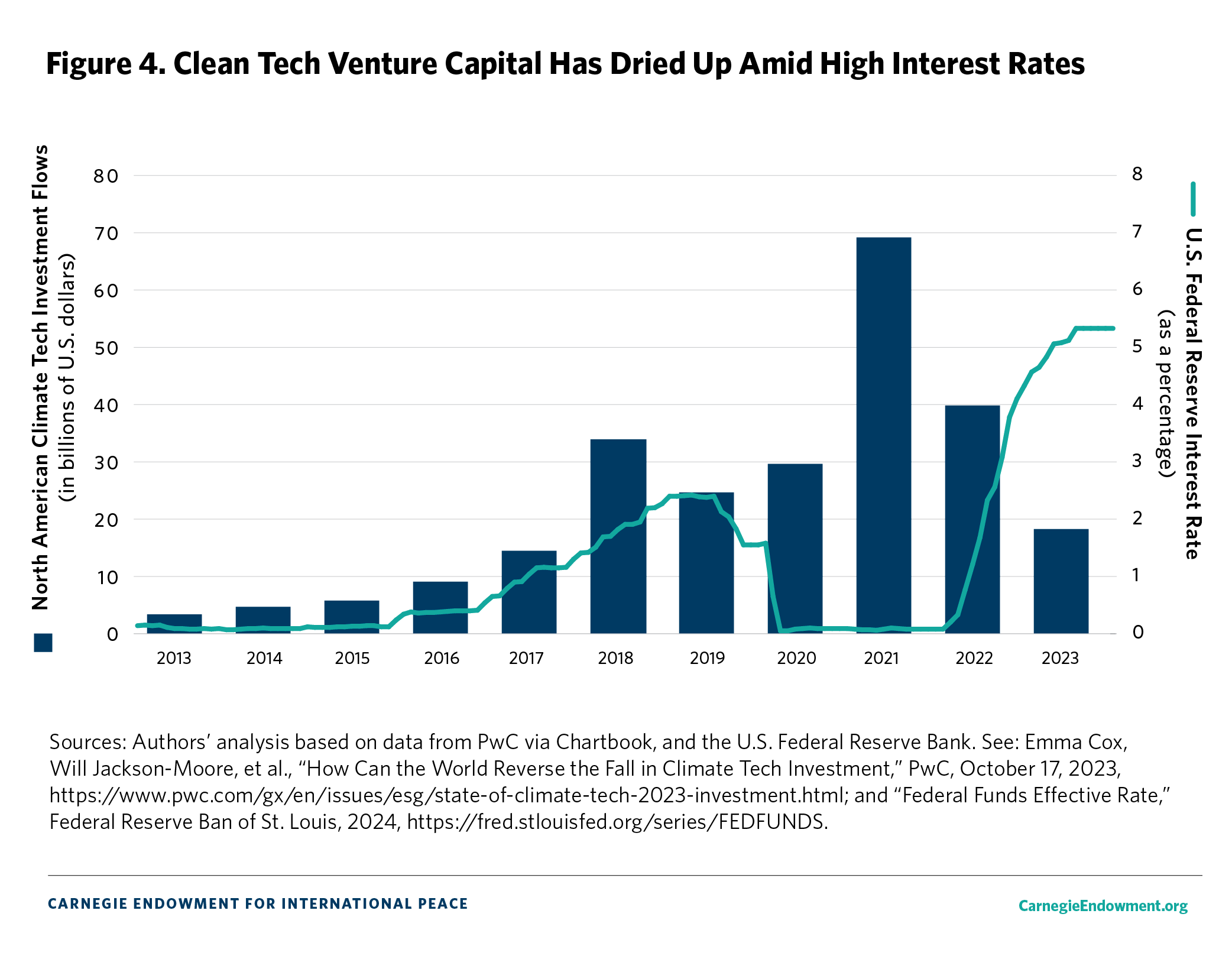

These are some of the many advancements underway in the United States, but what unites them is the predicament of being at a pre-commercial stage. After several rounds of equity raising amid positive policy signals, some of these firms could be entering a precarious valley of death, especially those at later stages of development seeking financing for demonstration or a first-of-a-kind project.50 At present, many of the government grants to demonstrate next-generation technologies have been expensed while some investors have become cautious amid structurally elevated interest rates (see figure 4). Although global clean energy investment flows are annually increasing and are expected to reach $2 trillion this year—double those of fossil fuels—venture capital for North American climate tech has waned since peaking in 2021 (although clean energy-specific flows have may have proven slightly more resilient, peaking in 2022).51 Even though the number of climate tech deals as a percentage of venture capital remains strong, investment flows have dried up particularly for later-stage start-ups hoping to start commercializing their technology.52 U.S. policy will now need to address these market dynamics by propelling its most impactful leapfrog technologies to market—all the while continuing to incubate new, disruptive systems.

Policymakers may not need to strive for another clean energy bill. Instead, they might choose to bolster these technological opportunities through a broader “innovation first” policy to enhance U.S. competitiveness across high-tech sectors. To do so could neutralize the partisan nature of the energy sector and address the macro-level challenge at large; amid Washington’s attempts to restrain Beijing’s technological advancement, Chinese innovation has only accelerated and the country has cemented its status as a “scientific superpower.”53 If the Inflation Reduction Act (IRA) and Infrastructure Investment and Jobs Act (IIJA) were, at least in part, responses to the supply chain shocks of the coronavirus pandemic and the Russian invasion of Ukraine, then a sector-neutral innovation agenda would be a fitting response to such tectonic shifts in technological power dynamics. Within this innovation framework, several policy principles for the energy sector are key: targeted demand drivers to pull mature technologies to commercial scale, coordinated technology hubs to incubate domestic know-how through continued demonstration, and an expansion of R&D policies to develop future innovations.

Advancing near-commercial technologies to market requires targeted market-shaping measures that can be applied through existing legal frameworks. If the IRA is the blueprint for U.S. clean energy policy, then future legislation may consider updating this tax architecture when Congress deliberates tax reform at the end of 2025. The IRA has a technology-neutral tax credit for clean power that already includes bonus incentives for domestically manufactured renewables, and a similar bonus tax credit could be extended to next-generation, U.S.-made technologies like advanced nuclear, geothermal, or solar energy (an analogous bonus could be applied to the tax credit for stationary energy storage).54 Amid the absence of a domestic carbon tax, an IRA-style production tax credit could be leveraged for the clean industrial sector to reward emission reductions per unit of the material produced. Similar tax credits could incentivize advanced grid technologies, vital for decarbonization and domestic security. Such subsidies should be designed to sunset over time—much like Europe’s feed-in tariffs—to ensure that industry organically cuts costs and does not become reliant on handouts.

But even if the United States does not pass new legislation, certain facets of U.S. tax law could be amended at the department level to encourage the adoption of new technologies. As silicon and lithium-metal batteries begin to be commercialized, the U.S. Treasury Department might take more stringent measures against allowing Chinese graphite to be eligible for the IRA’s EV subsidies. This would, in turn, limit the number of incumbent graphite-based batteries eligible for tax breaks while expanding the competition for the disruptors to enter the market: lithium is highly IRA compliant, and some silicon firms are already sourcing their products domestically55 (enacting this policy, however, would require amending the IRA’s language to include silicon as a critical mineral, something that could be achieved by instead referencing the Department of Energy’s critical minerals list).56 Although this could temporarily slow the pace of EV sales, the trade-offs would benefit the acceleration of better technology that could prove an asset to fully decarbonizing U.S. road transport and potentially aviation.57 Policymakers could view this as a necessary course correction as the United States risks sleepwalking into spending over $150 billion in tax breaks and loans to onshore an incumbent battery technology (think of Blackberry factories at the dawn of iPhones and Androids).58

The federal government should take a more stringent approach to domestic procurement by leveraging its purchasing power and market structures to bring next-generation technologies to market that boast the greatest long-term resilience. Already, the federal government has initiated offtakes for solar panels from the Department of Defense and EVs for government services.59 But committing federal funds to technologies that Chinese firms dominate—even if these technologies are produced in the United States—does not advance long-term U.S. competitiveness. Going forward, such contracts might prioritize products like the first wave of thin-film perovskite tandem cells, military drones, or federal vehicle fleets with lithium-sulfur batteries and non–rare earth magnets, all of which open the door to phasing out Chinese-dominated supply chains.

In the power sector, the federal government can coordinate with states to act as subnational drivers of high-priority technologies too. The New York state government has offered subsidies for long-duration storage, a necessity for its climate goals.60 And while Colorado has issued incentives for geothermal projects, policymakers in Denver and other Western states should prioritize next-generation geothermal systems over incumbent hydrothermal systems.61 California is already deliberating an analogous measure.62 Similarly, the Public Utilities Commission of Nevada is weighing the approval of a “clean firm tariff” that would allow utilities to leverage the upfront costs of off-takers like data center developers to stimulate demand for technologies like advanced nuclear energy, next-generation geothermal technology, and long-duration grid storage.63 If successful, this could be a model for other state and regional regulators to use as well.

To support firms at the pilot stage, the federal government should expand sectoral innovation hubs where firms can test their technology while protecting intellectual property (IP). The Department of Energy’s Utah FORGE project, which tests enhanced geothermal systems, could be expanded to include other innovative geothermal drilling techniques like closed-loop and superhot-rock systems, which are both comparatively further from commercialization but yield additional opportunity.64 In the nascent U.S. battery sector, the Department of Energy’s partnership with Stanford University has created a battery-testing facility, and similar sites might be dedicated for lithium-metal batteries near gigafactories across the Battery Belt like the Georgia Tech Advanced Battery Center, which researches solid-state technologies and is located in the state with the second-largest battery manufacturing capacity in the country.65 These hubs can serve as centers of economic and academic development, and are emerging organically and by design.66 The CHIPS and Science Act funded a mineral processing hub in Missouri and a battery recycling hub in Nevada, while in the state of Washington a group of silicon-anode battery companies have partnered with local universities for workforce development.67 As regions become epicenters of technology deployment—including direct lithium extraction in Arkansas, floating offshore wind turbines in California, and clean hydrogen in Texas—local hubs might be leveraged as places to test next-generation systems, resulting in transferrable expertise to similar projects across the country.68

In 2025, Congress is slated to reauthorize the Energy Act, creating opportunities to preserve the role of new Department of Energy agencies essential to providing continued funding to help leapfrog firms. While the IIJA authorized the Office of Clean Energy Demonstrations (OCED) to oversee hydrogen and direct-air-capture hubs, the Department of Energy’s recently initiated Office of Manufacturing and Energy Supply Chains (MESC) was a partisan creation to oversee the development of batteries and other important industrial supply chains. To galvanize nonpartisan buy-in, both offices could be authorized under the specific mandate to bolster U.S. resilience and future competitiveness: MESC’s authorization could mandate the office as a central nervous system for the Department of Energy’s supply chain agenda and the name could be subject to nonpartisan alteration, perhaps changing to something like the Office of Supply Chain Security.

Doing so could preserve internal knowledge of domestic industry while ensuring the office’s long-term funding potential, which is essential to derisking demonstration and first-of-a-kind projects amid a more modest growth market. Although the IIJA granted $8 billion for hydrogen hubs and analogous sums to next-generation nuclear and direct-air-capture technologies, OCED’s reauthorization should remediate the imparity left on the geothermal industry, which received only $84 million to demonstrate projects.69 OCED’s reauthorization could set a similar spending contribution for next-generation geothermal hubs comparable to those observed in other sectors. MESC’s future grants should continue at their current scale to help later-stage projects, but they should also include smaller grants to critical supply chains at an earlier stage seeking pilot demonstration funding—arguably a gap in U.S. tech-to-market funding.70 For example, next-generation batteries will require new materials, like solid electrolytes or lithium metal, all of which are logical areas to prepare the U.S. supply chain to develop further.

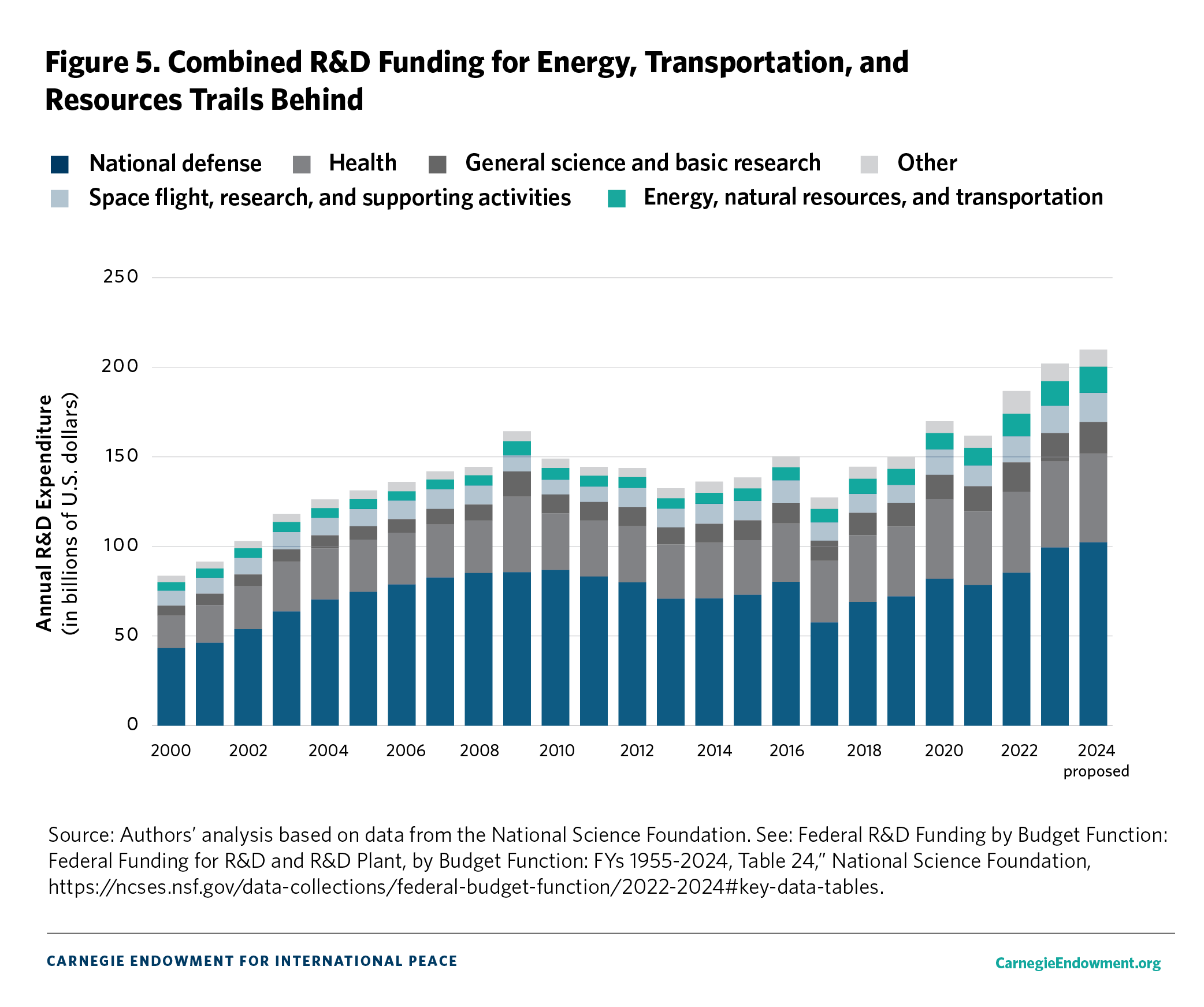

But once new ventures have made it to market (or failed trying), additional support will be needed to incubate new, early stage technologies. In reauthorizing the Energy Act, Congress might also consider expanding the budget and role of the Advanced Research Projects Agency-Energy (ARPA-E), which was designed to take on high-risk, high-reward projects and has proven a success. After $3.8 billion in R&D funds, the program has triggered over $12 billion in follow-on private financing and the formation of over 150 new companies.71 Both academics and past program directors have made the case for bolstering ARPA-E’s budget, but annual funding is still a fraction of the agency’s counterparts in the health and defense sectors despite increasing over the past decade.72 For context, the agency’s 2024 budget was lowered to $460 million, a mere 0.22 percent or so of total U.S. annual public R&D expenditures. In general, combined R&D spending in the United States for energy, transportation, and natural resources is lower than that in health or space (see figure 5).73 An expanded budget could help ARPA-E expand its SCALEUP program which helps new technologies commercialize.74 It could also expand funding to sectors which have received comparatively less government R&D funding like advanced solar cells and superhot-rock geothermal technologies.

Beyond departmental authorizations, Congress can leverage tax structures in next year’s tax package to spur corporate innovation, the primary provider of R&D funds in the United States.75 Washington will need to contend with Beijing’s innovation-friendly tax regime, which includes a 10 percent increase for all R&D in 2024 and an R&D super deduction that allows firms to write off up to 200 percent of relevant expenses.76 By contrast, U.S. policy has backtracked on innovation-centered tax incentives. Corporate tax cuts from 2017 mandated that R&D expenses be amortized over a five-year period instead of filed that year, which muted the tax break’s impact.77 Allowing companies to expense R&D costs the year of expenditure might encourage innovation, especially in energy start-ups struggling to survive with smaller cashflows and larger R&D expenses.78 For larger firms, carrots are not the only opportunity to guide policy. Some assert that the rise of stock buybacks has come at the expense of internal R&D funding, and sticks might be leveraged to push larger firms to invest in their long-term competitiveness in addition to short-term stock evaluation.79 Large companies could be required to spend a minimum portion of their revenue on R&D before they can buy back stocks (or, perhaps, failing to meet a quota could merit a penalty).

To help unleash this catalytic clean energy ecosystem, the United States can strike a balance between proactively protecting IP while not stifling collaboration with allies or opportunities in foreign markets. Policymakers could view foreign policy pathways for these leapfrog technologies within two existing frameworks based on technological proximity to commercialization. For earlier-stage technologies like next-generation batteries, solar, magnets, hydrogen, and nuclear energy, diplomacy for science may be prioritized with foreign laboratories and universities to spur domestic know-how and incentivize cross-border discovery.80 Technologies that are closer to reaching the market like advanced grid, storage, geothermal, and industrial systems are areas where trade and foreign development agencies should seek to build a durable export market and related opportunities to promote green industrial growth abroad.

There is strength in numbers. To balance the astounding growth of Chinese research, the United States should continue to engage in joint-research endeavors with its partners.81 Bilateral and minilateral R&D efforts should target high-priority leapfrog sectors where U.S. know-how can be strengthened through the U.S. national labs. South Korean companies rank second to China in global battery production82 and the Korea Institute of Science and Technology recently announced joint research with its American counterparts for solid-state battery development.83 Similar projects might be pursued with Canada and Finland, known for advanced mineral processing know-how, a concerning gap in the U.S. labor market.84 Other collaborative R&D projects could be pursued in areas of mutual discovery like geologic hydrogen, where Australia and France have identified deposits and are studying this potential.85 Although the United States has backed R&D collaborations with Japan and the United Kingdom for nuclear fusion, policymakers could consider mimicking this approach with superhot-rock drilling, an equally impactful potential breakthrough that could unlock abundant geothermal resources.86 Kenya and Iceland have analogous efforts underway.87

The United States should also pursue R&D and commercial collaboration in multilateral forums that have long-term, nonpartisan buy-in like the Quadrilateral Security Dialogue (Quad), which includes India, Japan, and Australia—all countries tentatively aligned on China policy. The Quad has broadly outlined R&D collaboration and clean energy coordination.88 Next-generation solar could be an area of focus with Japan prioritizing perovskite solar cells under its Green Innovation Fund, while Australia and India develop domestic PV manufacturing (and India could rank as the world’s number-two producer later this decade).89 In addition to South Korea, Quad countries are the essential actors in a non-Chinese solar supply chain, and ensuring that perovskites are integrated into this market will be important to maintaining some semblance of technological parity with Chinese producers. Other areas might include critical minerals where Australia’s renowned reserves and mining industry, Japan’s legacy battery industry, and India’s ambitions to be a player in processing could prove an avenue for the United States to deploy its advanced mineral processing IP.90

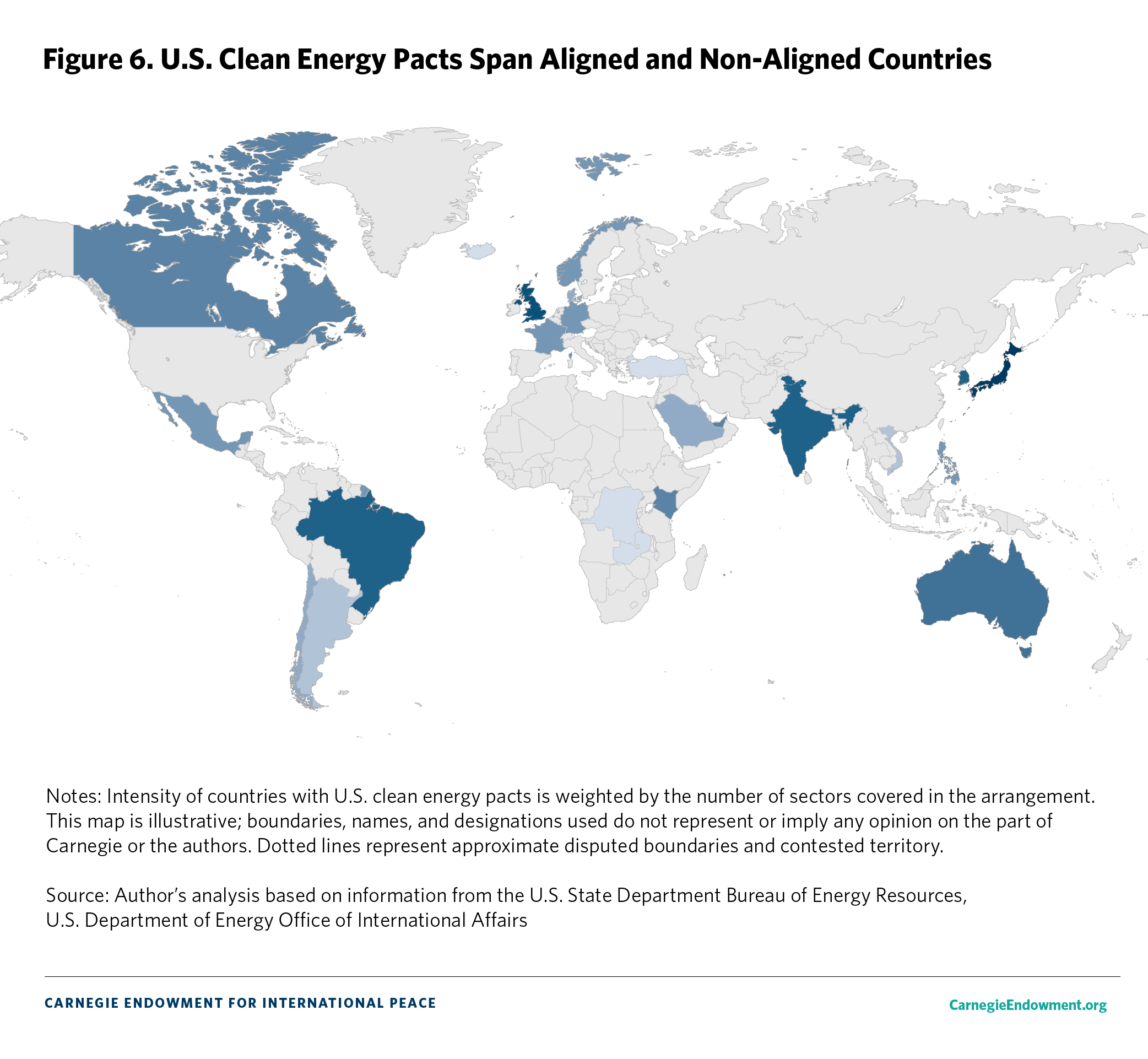

For leapfrog technologies that are closer to commercialization, the U.S. federal government should begin leveraging its various diplomatic trade arms to facilitate export markets and technology diffusion. These include the U.S. Trade and Development Agency and the International Trade Administration for promoting exports as well as the U.S. Export-Import Bank and the International Development Finance Corporation for deploying capital. As has been done in the semiconductor space, policymakers should define which security and multilateral bodies are most suited for diffusion and in which sectors (see figure 691).

For more sensitive, dual-use technologies, Washington may embrace promoting the manufacturing of these advancements to allies once they are established in the U.S. market. For example, if the United States commercializes batteries and magnetic motors that do not require Chinese-dominated minerals, it is in the United States’ interest to disseminate those technologies to allies who face analogous supply risks—so as to challenge the global importance of Beijing’s mineral empire. Long-duration grid batteries and correlated advanced grid technologies might be prioritized for export markets with high renewable-energy penetration like Chile, Spain, Germany, India, and Australia, and also countries willing to pay a security premium to avert Chinese involvement in their critical infrastructure (bans on Huawei’s network equipment could be a metric to gauge such appetite).92 Over time, advanced nuclear reactors could be deployed in countries with aversion to Chinese or Russian nuclear industry. The United States has promised a small modular reactor to Romania.93

For next-generation geothermal and industrial decarbonization, which are closer to commercialization and do not pose inherent security advantages, policymakers might prioritize trade and export strategies outside of security-aligned countries. Even though the United States is a leader in low-carbon cement or steel start-ups, it is not necessarily in the country’s economic interest to become a world-leading producer of low-carbon materials. Over time, as green premiums decrease, these technologies should be actively diffused through joint ventures in markets on the cusp of construction and emissions growth like India and countries in sub-Saharan Africa.94 Positive trends of this sort are already underway in the next-generation geothermal sector where U.S. trade delegates have paved the way for early developments in Kenya and the Philippines alongside local industry.95 Similar projects might be pursued in countries with existing geothermal industries like Turkey and Indonesia as well as with state-owned oil and gas companies seeking diversification. Those in Colombia and Brazil have already signaled interest.96

Beyond all the necessary domestic and foreign policy mechanisms, the clearest means of ensuring that leapfrog technologies reach the market is through long-term demand certainty. But in the American market, securing long-term demand for these technologies is not only a question of fiscal expenditures, IP law, or innovation incentives—it is a question of politics. Amid today’s seemingly intractable bipartisan divisions, the left and right must forge consensus that accelerating U.S. energy innovation is in the best interest of the country’s geostrategic goals and planetary boundaries. Part of this may entail that both sides concede on areas of discomfort: the right may need to accept a higher-level of risk tolerance and make peace with some government-backed energy start-ups failing; the left could loosen environmental permitting criteria to cut red tape and expedite the deployment of next-generation advancements. If Washington fails to find common ground and unleash its clean technology potential, it may render the nation an oil-and-gas laggard amid transformational shifts in energy systems, paving the way for China to be the green energy cartel of the future and subsequent arbiter of global climate solutions. But if the United States succeeds, it will unlock a new era of industrial and technological competitiveness to the benefit of the country and future of the planet alike.

The author thanks Varun Sivaram, Kate Gordon, Tom Moerenhout, and Lisa Hansmann for their peer-review of this work and to Carnegie colleagues Daniel Baer, Toby Dalton, Noah Gordon, and Daniel Helmeci for their invaluable input.

Fellow, Sustainability, Climate, and Geopolitics Program

Milo McBride is a fellow in the Sustainability, Climate, and Geopolitics Program at the Carnegie Endowment for International Peace.

Recent Work

Milo McBride, Pauline Gerard

Carnegie does not take institutional positions on public policy issues; the views represented herein are those of the author(s) and do not necessarily reflect the views of Carnegie, its staff, or its trustees.

It seems likely that, no matter what, the power of the U.S. nuclear arsenal will face erosion, not least in the credibility of its commitments to defend allies and the political durability of those alliances.

James M. Acton, Ankit Panda

When Giorgia Meloni very publicly rebuked Donald Trump’s disparaging remarks about her, it surprised many who saw her as a European extension of Trumpism. Is the spat a sign of trouble in the radical right’s transatlantic axis?

Rym Momtaz, ed.

European allies are less focused on appeasing Trump and more focused on smoothing the transition to a Europe-led alliance.

Sophia Besch, Alper Coşkun, Nate Reynolds, …

Middle powers in the region will keep hedging between Washington and Beijing. It’s in the great powers’ interests to play along.

Amr Hamzawy, Kathryn Selfe

Democratic erosion is undercutting four key elements of U.S. power, with mounting and likely lasting effects.

Thomas Carothers