Absent rapid reform, Tunisia’s economic policies will plunge the country into an abyss. Already, a financial crisis is brewing. This is the worrisome outcome of the path the country has followed since President Kais Saied’s power grab in July 2021. The path is underpinned by two main aspects of economic policy. The first is an expansive (and expensive) fiscal drive that has produced historically large deficits for four successive years, pushing public debt to unsustainable levels. The second is insufficient governmental support for economic activity, with a deteriorating business climate and heightened macroeconomic risks scaring the productive sector and halting economic growth.

The mechanism that could spark a conflagration is also becoming clearer. The closing of external spigots is pushing the government to finance more of its large deficit domestically, through increased borrowing (from banks, national bondholders, and the Central Bank). This is crowding out the private sector, lowering economic growth, increasing inflation, diminishing the quality of banks’ balance sheets, and increasing the risk of a large devaluation of the Tunisian dinar. All the elements are in place for a financial crisis that extends across public debt, foreign exchange, and the banking sector.

Presidential elections are scheduled for the end of 2024. Saied has built his populist appeal on a public commitment to two principles: resolute opposition to an International Monetary Fund (IMF) program, in order to avoid the austerity-related hardships it would cause the population; and fighting corruption by compelling the “corrupt business elite” to relinquish its allegedly ill-gotten wealth through a judicial process that threatens business owners with jail if they do not acquiesce. These two principles have resonated with a population fed up with a chaotic decade marked by repeated external bailouts and rising domestic corruption. However, Saied’s approach has also led to a jump in debt and a collapse of growth, both of which are now eating away at the economy.

As a result of all this, there is a serious risk of a financial blowout. Tunisia is perilously close to having to dig into its financial reserves. There is no guarantee that the situation will remain contained until the elections. A financial crisis, if it erupts, risks inflicting on the country a harrowing mix of state bankruptcy, economic collapse, deep social wounds, and major political challenges, given the need to distribute large losses across the population.

The repercussions of flawed policies have already resulted in a decline in economic growth and a deterioration of social conditions, with reduced real wages and increased unemployment. These outcomes have led the government to increase the size of subsidies, which contributes to a significant fiscal deficit and further reinforces the unsustainability of public finances. Consequently, the country faces difficult choices. A soft landing would require a bold reform program to boost economic growth, sound and determined political leadership to ensure social cohesion, and, ideally, a supporting hand from Tunisia’s friends abroad.

Summary of Tunisia’s Prospects for 2024

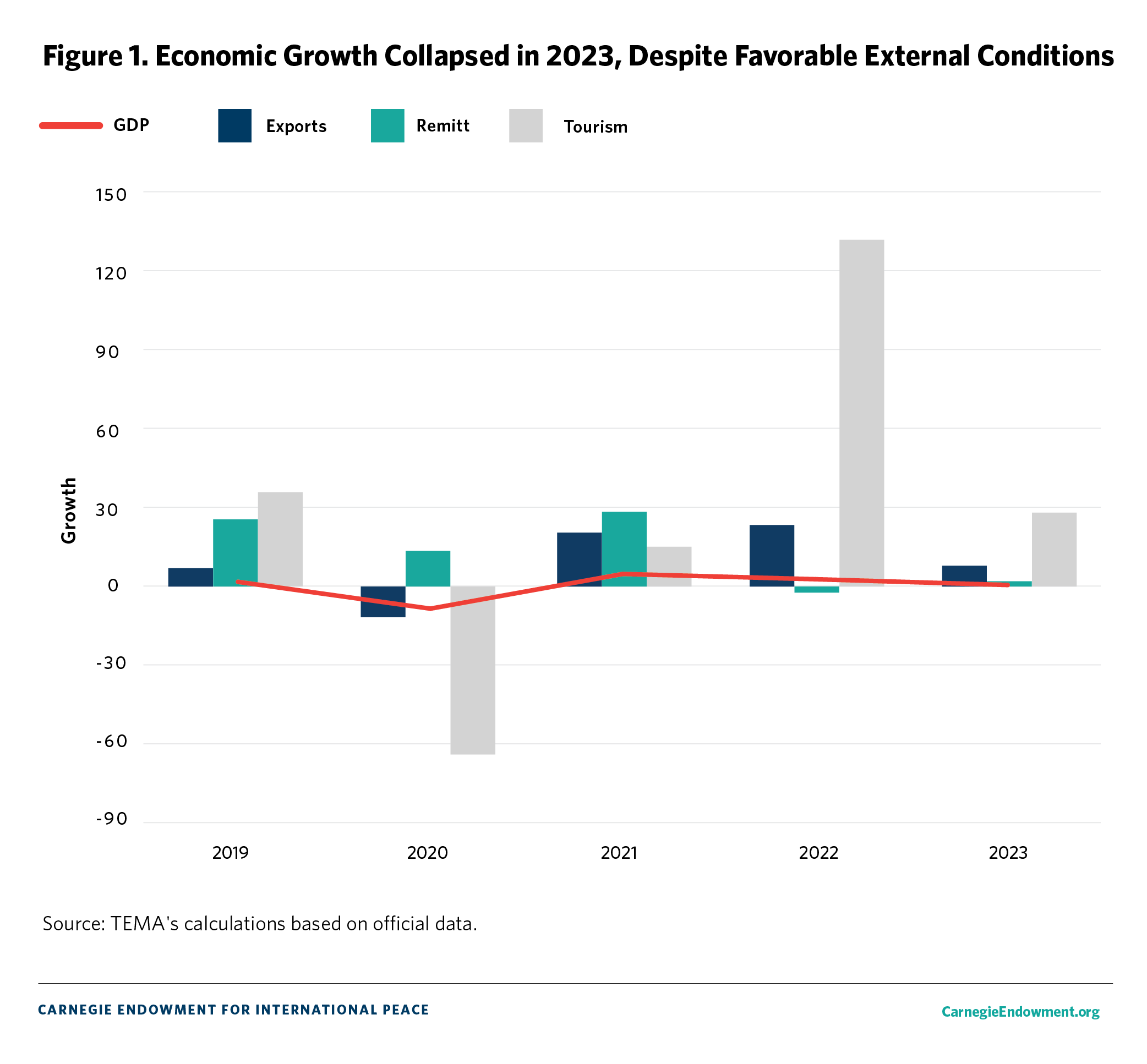

In 2023, Tunisia experienced its lowest economic growth in a decade, save for the first pandemic year of 2020. This poor performance had domestic causes: declining consumption caused by rising inflation and the deterioration of employment and social conditions, as well as a fall in investment. There are high risks of macroeconomic instability in 2024:

The president’s insistence on high levels of social expenditures—subsidies and transfers—is leading to a rise in debt. Given the dearth of external financing, it is also leading to an increasing reliance on domestic borrowing and direct financing from the Central Bank.

The 2024 budget still contains a significant foreign funding gap that is likely to prove very difficult to close under the current circumstances. Given the scarcity of external funding sources, and in the absence of an agreement with the IMF, Tunisia has increasingly leaned on the domestic financial sector, particularly banks, to finance its budget deficit. However, this heavy reliance on the domestic capital market is crowding out financing of the private sector and heightening the exposure of the banking sector to sovereign default risk.

Given the limited availability of external borrowing options and the weak capacity of Tunisian banks to absorb a significant financing gap, the state is likely to increase its reliance on monetary financing. This risks rising inflation, as well as a run on foreign exchange reserves that could in turn precipitate a financial crisis from which the country may find it difficult to recover.

Instead, the recession was caused by Tunisia’s domestic weaknesses. On the production side, agriculture, construction, and industrial output declined, while manufacturing stagnated (see Table 1). Agriculture was hit hard due to bad rains, but all sectors suffered because of a fall in domestic demand and low domestic investment. On the aggregate demand side, household consumption declined due to the rise in prices and the fall in incomes, and investment continued to decline—reaching a historically low level—due to the deterioration in the business climate and risks connected to macro-instability. High spending by the government was not sufficient to compensate for these weaknesses.

Table 1. Economic Growth and Social Conditions

Units

2022

2023 (estimates)

Real GDP growth rate

Percent change per year

2.50

0.70

Agriculture

Percent change per year

1.00

-12.50

Industry

Percent change per year

-5.40

-4.60

Manufacturing

Percent change per year

5.50

0.20

Construction

Percent change per year

-5.70

-3.90

Tourism

Percent change per year

10.30

11.90

Other services

Percent change per year

1.40

1.40

Level of prices

Average percent change per year

8.30

9.40

National investment as a percent of GDP

Percent

14.90

12.80

National savings as a percent of GDP

Percent

6.30

7.00

Unemployment

Percent

15.50

15.80

Unemployment for people aged 15-24 years

Percent

38.10

39.10

Unemployment, college graduates

Percent

23.60

23.80

Poverty

Percent

16.60

Source: National Institute for Statistics, Ministry of Finance (Tunisia); TEMA. Data for 2023-24 from Budget Law-2023

and Budget Law-2024; 2024 estimates from TEMA and IMF.

Inflation was not fueled by the devaluation of the dinar, which remained stable vis-à-vis major currencies (see Table 1). Moreover, the prices of imported basic products fell that year. Instead, inflation can be explained by the state’s increased recourse to monetary financing. The Central Bank has thus far provided the liquidity that the Treasury needs to meet its expenses—first via the banks it refinanced, and then, since February 2024, directly. All indications suggest that inflation will remain high for the immediate future, especially if the dinar experiences further depreciation to help balance the external accounts.

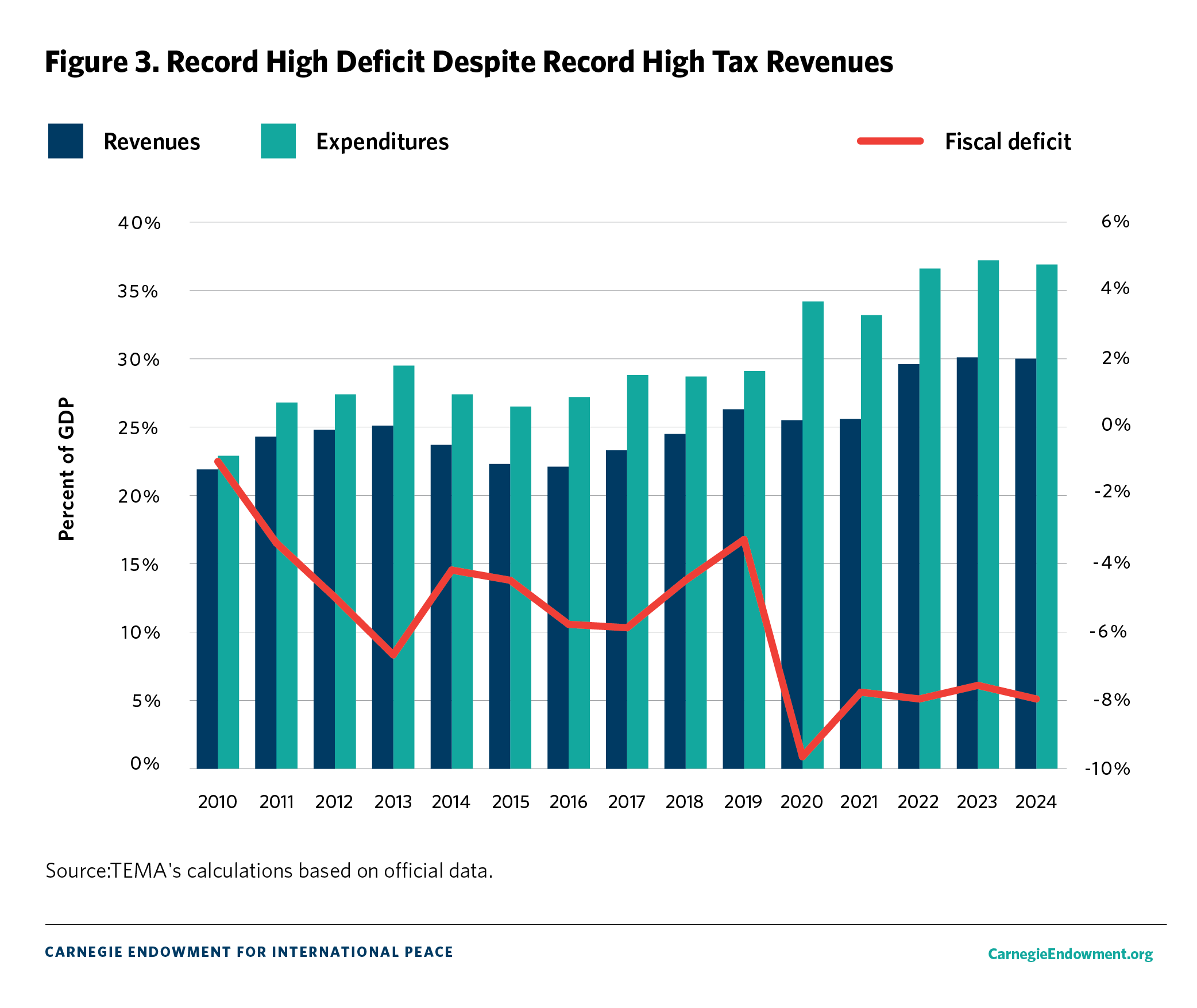

Now that the 2023 books are closed, it is clear the hoped for improvement in fiscal accounts did not take place. Indeed, 2023 ended with a state deficit of 7.7 percent of GDP, close to the levels of 2021 and 2022 (see Table 2). Tunisia has been grappling with high fiscal deficits since 2011 (see Figure 2). The acceleration in the growth of the state deficit coincides with the political change brought about by the uprising of 2010–2011. This was a period during which Tunisia, which until then displayed good control of its public accounts, turned fiscal deficits into a tool of social appeasement by increasing the public sector wage bill and social expenditure. From 2.8 percent of GDP on average during the 2000s (during which time Tunisia was known for its fiscal rectitude), these deficits rose to 4.5 percent of GDP on average during the 2010s. After 2020, the new decade saw larger deficits in its first half and a difficult adjustment. The deficit shot up from 3.4 percent of GDP in 2019 to 9.4 percent in 2020, owing to government support of households during a difficult period of confinement and collapse in income (see Figure 2).

In the years following the overthrow of Zine al-Abidine Ben Ali in 2011, the deficit was driven by the increase in public sector wages—an initiative undertaken by the government to appease the country’s largest and most powerful labor union—which reached the extremely high level of 16 percent of GDP in 2020 before stabilizing. Afterward, instead of declining to normal levels, the deficit remained high—around 7.8 percent of GDP during 2021–2023, which is a record and which corresponds with the presidency of Saied (see Figure 2). The fiscal deficit rose on account of a rise in subsidies and social transfers, policies that suited the new populist regime (see Figure 3). The servicing of the accumulated debt also increasingly weighed on the deficits. The poor fiscal performance of 2023 was a result of a continuous rise in public spending, which caused a high deficit despite a rise in state revenues.

In 2023, tax revenues reached 30.1 percent of GDP, well above the average of 21.1 percent of GDP during 2015–2019 (see Figure 2). In fact, they are now at a record level in Tunisia, and are also the highest in Africa and the Middle East. This rise, which came despite sluggish growth, was due in part to a rise in rates (an increase in VAT revenues—the result of the removal of the 13 percent rate on some products and the generalization of the 19 percent rate—and a rise in customs duties). The main reason, however, is the effort made by the tax administration to improve tax collection with an unprecedented increase in tax control campaigns targeting the business community.

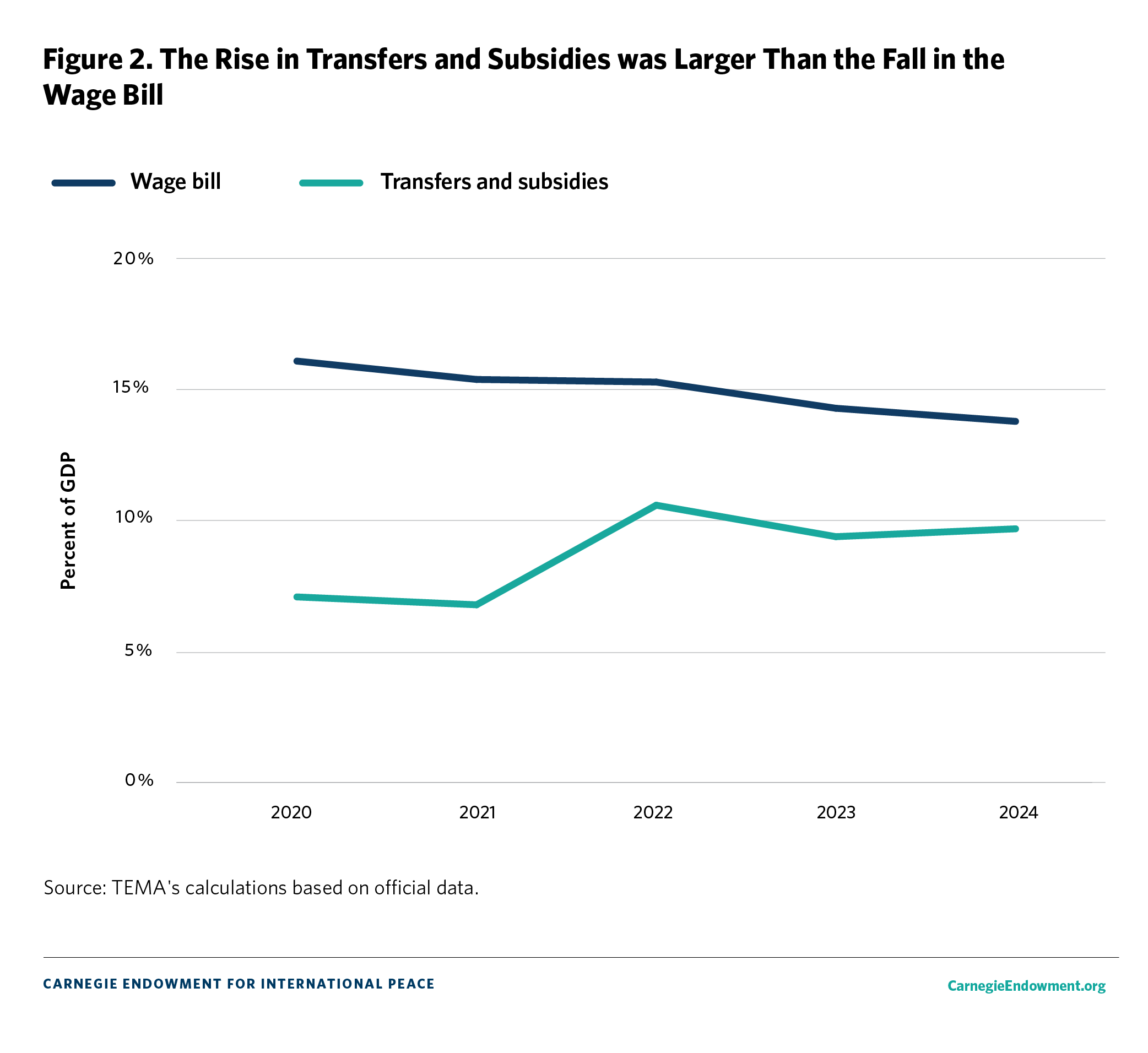

Expenditures also closed the year at the record level of 37.2 percent of GDP, the highest expenditure ratio in Tunisia’s history—higher than the already high figure of 36.6 percent in 2022—and far exceeding the 32 percent average reached in the period 2015–2019 (see Figure 2). This occurred despite a relative fall in the wage bill, which declined from 16.1 percent of GDP in 2020 to 14.3 percent in 2023. It also came despite further cuts in public investment, which is now at a paltry 3.5 percent of GDP—not enough to maintain infrastructure, let alone spur economic growth (see Table 2).

The stabilization of the wage bill and the rise in fiscal revenues reflect the two major political changes brought about by Saied’s increasingly repressive rule: a weakening of the main labor union; a September 2022 decree of a salary increase of only 3.5 percent for public sector employees for the following three years (2023–2025); and a populist attack on the economic elites for their “corruption” and inadequate support for the domestic economy.

The main budget line that has risen is social expenditure—subsidies and transfers—which have been extended as a safety net to offset the worsening economy (see Table 2). Paradoxically, however, this is leading to a rise in debt and a further aggravation of the economic situation. Saied’s insistence on high social spending is also the main reason for his refusal to enter into an agreement with the IMF.

In 2023, subsidies and social transfers stood at 12 percent of GDP, a high level in Tunisia (see Table 2) not much different from that of the previous year. Subsidies are designed to support the population’s ability to pay for energy products, transport, and basic food staples, which is why their share of the state budget has doubled since 2021. Their real cost is in fact higher, however, since some subsidies that are not financed through the budget and end up showing as losses in state-owned enterprises, taking the form of state-guaranteed loans or even arrears. Fuel subsidies more than doubled in 2022–2023, increasing from $1 billion in 2021 to $2.5 billion in 2022 and reaching $2.3 billion in 2023. Expenditures meant to subsidize consumer products other than fuel have similarly risen. Social transfers, which are direct payments to people below the poverty line, rose during the COVID-19 pandemic due to the growth of the AMEN program of monetary transfers to the poorest segment of the population, which helps 341,000 poor households across the country, and have also remained at a high level.

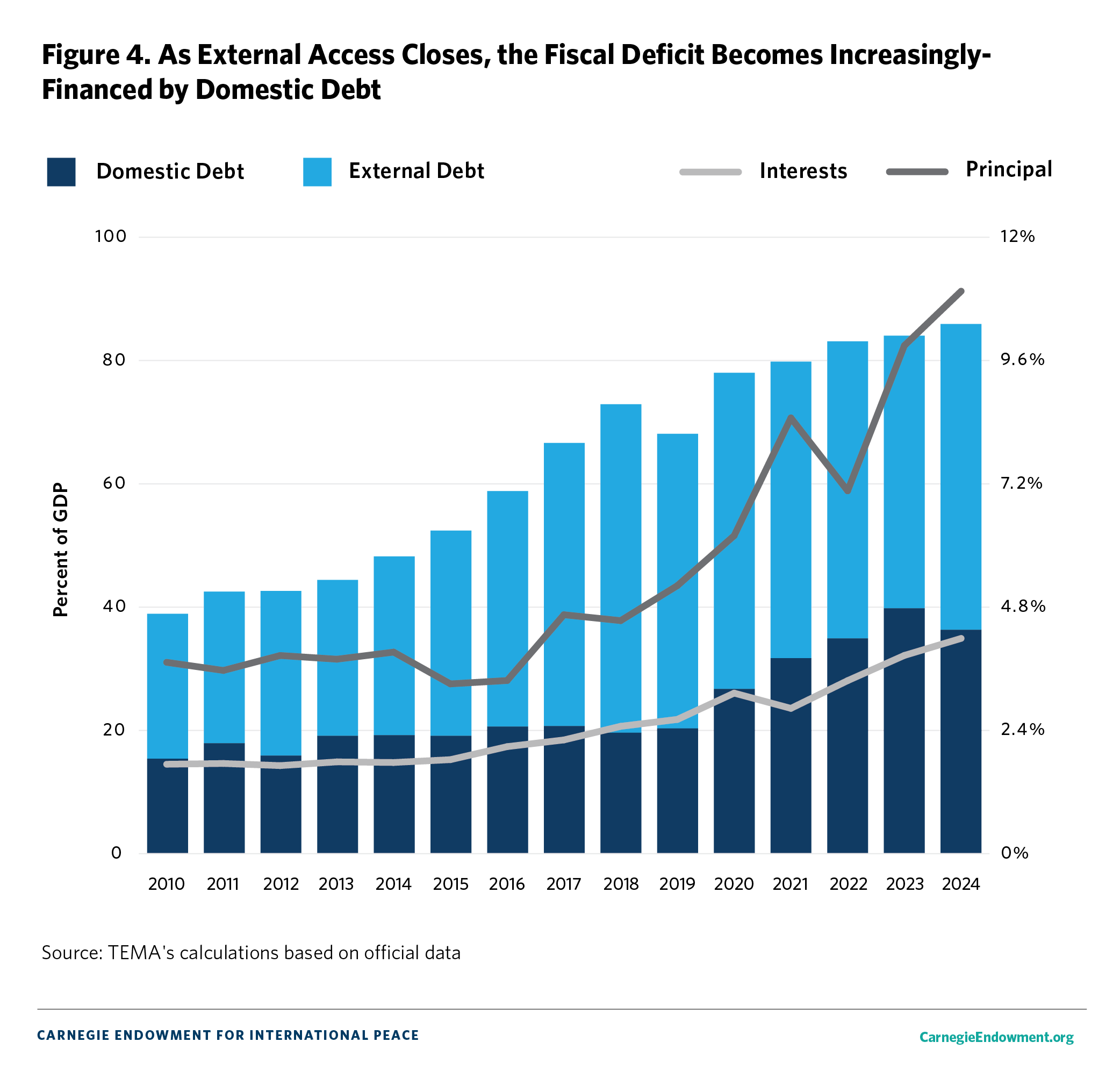

The rise of the debt burden is also worrisome. To service its debts, the Tunisian state must pay not just a large interest payment, but also a repayment of the principal, which has become more difficult to roll over, especially now that the international bond market for Tunisia has closed. The debt service in 2024 amounts to $8.3 billion, a charge that has more than doubled in four years, and which represents 14.4 percent of GDP (compared to 13.2 percent of GDP in 2023 and only 7.8 percent in 2019). At 10.4 percent of budgetary expenditure in 2023, debt servicing has become the third largest expenditure item in the state budget, after salaries (40.6 percent) and subsidies (20.5 percent). This includes significant repayments of principal on external debt. The amortization required for 2024 is $6 billion—a charge that has tripled in five years (it stood at only $2 billion in 2019). The interest bill alone amounted to 3.7 percent of GDP in 2023—it was 3.1 percent in 2020 (see Figure 4).

The rise in debt servicing is due to the rise in indebtedness. At the end of 2023, the central government’s stock of public debt stood at 81 percent of GDP, or $42.5 billion, which was 10.8 percent higher than at the end of 2022, and five times higher than on the eve of the uprising in 2011. This amount does not include the debts of public enterprises, which are guaranteed by the state. But the debt of many state-owned enterprises (SOEs) has ballooned in recent years, following the deterioration of the financial situation of these companies. The exact figures are not known. But the total amount of guarantees on loans of the 43 largest SOEs, which is published by the Ministry of Finance, stood at $7 billion at the end of 2023, double what it was seven years earlier. If we add the debt of these public enterprises to the debts of the central government, total public debt stood at 94.4 percent of GDP at the end of 2023 (see Table 3).

The 2024 Plan: From External to Internal State Borrowings

The recently approved 2024 budget is only a bit less expansive than the 2023 budget, with a planned deficit of 6.6 percent of GDP. The main questions are whether the budget is financeable and whether it can stave off a financial crisis.

For the state to reach its fiscal targets, many budget items—wages, subsidies, and transfers—would have to grow at a rate less than that of inflation. The deficit might well end up larger than planned, as is often the case in Tunisia, since it is based on overly optimistic expectations regarding both revenues and economic growth. The 2024 budget assumes that the economy will rebound at a rate of 2.1 percent and that inflation will decline to 7.3 percent. While the government insists that there will be no tax rate increases in 2024, it anticipates an increase of approximately $1.5 billion in tax revenue, which represents a 10 percent increase compared to 2023, driven by corporate tax revenues, which are expected to rise by about 20 percent. Given that the corporate sector is already over-taxed, this increase in tax revenue is unlikely to improve the deteriorating business climate and does not foreshadow a rise in private-sector investment. Moreover, despite the political red lines imposed by Saied, the budget foresees revenues of more than $160 million provided by privatizations—an unrealistic goal, given that these brought in less than $15 million between 2020 and 2023. On the financing side, the 2024 budget plan foresees a need to borrow approximately $3.8 billion to finance the current deficit, plus $6 billion to refinance the principal due on past debts. This adds up to borrowing needs of nearly $10 billion—more than the previous record reached in 2023. A key challenge is that more than half of the servicing of the debt (58.3 percent) must be honored in foreign currencies and must be contracted from abroad in order to keep foreign reserves from shrinking. What is most worrisome is that only $1.5 billion of new external loans have been sourced. The remainder, which amounts to more than $3.5 billion, has yet to be found. Thus, the main challenge facing the state in the 2024 budget remains the large foreign funding gap, which would be very hard to secure under the current circumstances.

As its creditworthiness has deteriorated, Tunisia has faced constraints in obtaining even short-term trade financing. The increasing constraints on imports faced by SOEs have affected several products, including coffee, tea, vegetable oils, both soft and hard wheat, and medicines, causing repeated shortages since 2022. The reduction in imports has also been driven by a weakening domestic demand and a shrinking of the manufacturing sector. In April, Tunisia secured $1.2 billion in trade credit from the Islamic Trade Finance Corporation, an international development financing institution, to support state-owned enterprises facing challenges in financing essential imports, such as crude oil and petroleum products. This loan will alleviate import shortages stemming from the inability to finance imports but will not help in covering the budget funding gap.

Tunisia’s high level of indebtedness has started worrying its creditors, both external and domestic, and this is exacerbated by the country’s refusal to enter an IMF program. The fact that the risks of default have risen has resulted in the drying up of external sources of financing. The challenge of refinancing external debt has become more difficult as a result of the closing of the external funding market. The yield on Tunisia’s Eurobond remains over 20 percent, meaning that the international financial market has essentially closed down, resulting in Tunisia being relegated to the list of countries likely to default. In 2023, external public debt represented more than half (56.7 percent) of total public debt. This amounted to 53.6 percent of GDP that year, lower than its peak of 65.5 percent in 2018 (see Figure 4). For a country of Tunisia’s income level, this is not a very high level of external indebtedness, especially given that a large share is due to multilateral sources at concessional rates. What makes the external debt riskier is the lack of action to adjust the financing situation. External debt is made riskier by the rising exchange rate risk, since a real (as opposed to nominal) devaluation increases the domestic cost of servicing external debt. Reflecting the deterioration of the country’s creditworthiness, its credit rating has been downgraded repeatedly in recent years. As of June 2023, Tunisia’s rating from Moody’s is Caa2 and from Fitch is CCC-, indicating a substantial risk of default. In September 2024, Fitch upgraded Tunisia’s rating to CCC+, citing the country’s commitment to meeting its external debt obligations. However, the rating agency emphasized the ongoing challenges, including high financing needs, limited access to external funding, and uncertainty about the banking sector’s capacity and willingness to absorb significant volumes of domestic debt. The closing of access to external debt has pushed the Tunisian authorities to resort more to the domestic capital market. Yet domestic borrowing on an abnormally large scale has become increasingly problematic. The share of domestic borrowing in total state borrowing increased to 52.6 percent on average during 2021–2023 compared to 29.5 percent during 2015–2019 (see Figure 4).

A Financial Sector at the Service of the State

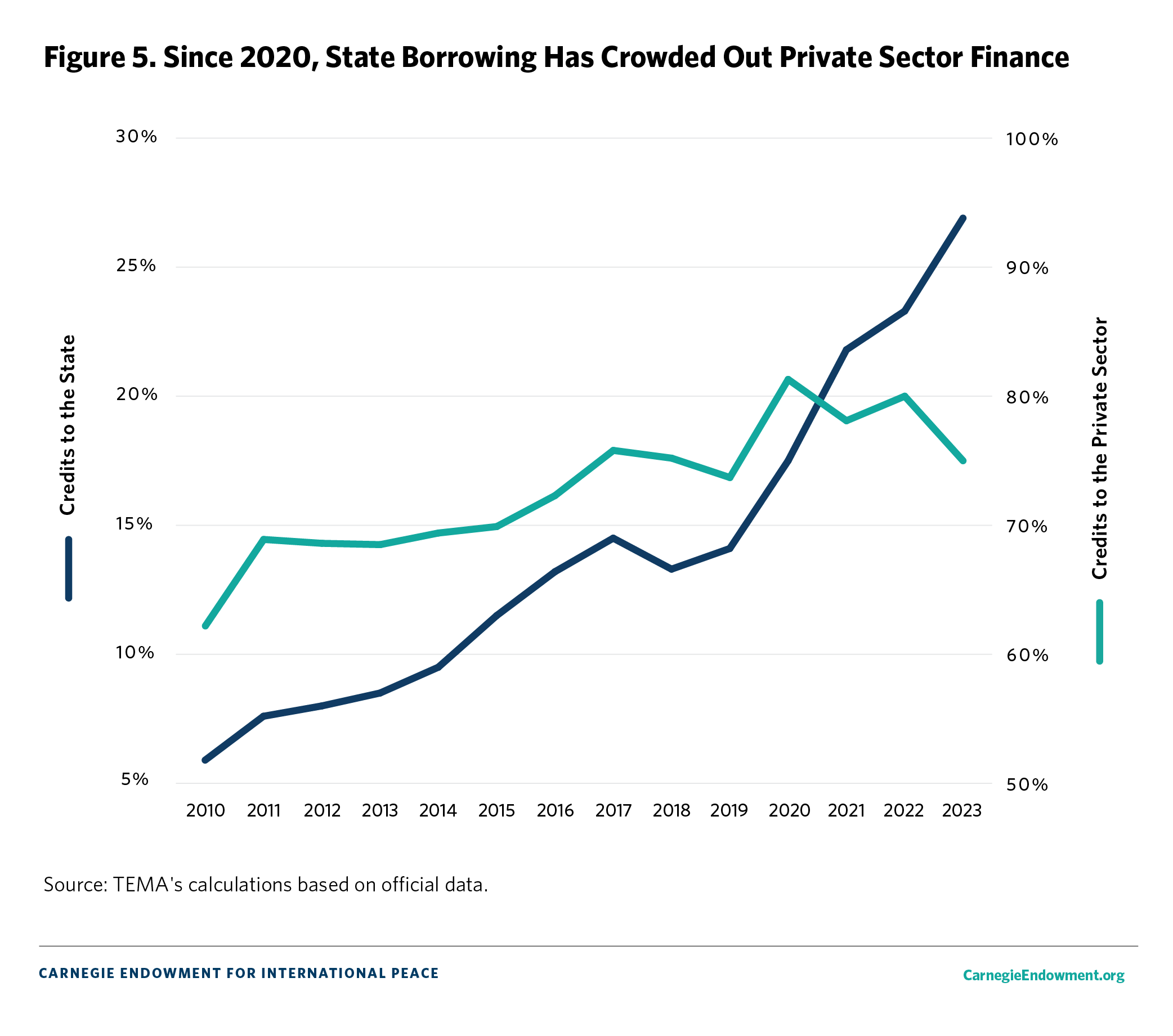

The major disadvantages of the orientation toward the domestic capital market are that it both crowds out financing of the private sector and increases the riskiness of the banking sector. The banking sector’s net claims on the state, which have almost doubled over the past five years, amounted to 23.6 percent of GDP by the end of 2023 (see Figure 5). Given the attractive returns, a credit risk that is deemed low (in comparison to lending to the private sector), and the systematic support for liquidity provided by the Central Bank in times of need, the banking sector has welcomed the growing exposure to sovereign debt. Banks were also encouraged to shift their lending to the state by the drop in demand for credit from the private sector, a consequence of the reluctance of businesses to invest in a time of deteriorating conditions.

The imbalance became more extreme during 2023. Bank credits granted to the state increased by 24.8 percent over the year, while credits to the private sector increased by only 2 percent—the lowest growth rate of bank financing of the economy in at least two decades. Of the $17 billion in domestic debt recorded in November 2023, just over 75 percent ($12.9 billion) was held by Tunisian banks and 22.7 percent ($3.8 billion) was on the balance sheet of the Central Bank. There were also direct loans in foreign currencies granted by Tunisian banks: they tripled in 2023 compared to 2022, reaching $400 million (see Figure 5). These figures indicated that in the event of payment default by the state, the situation of Tunisian banks would be considerably weakened.

Today, public debt represents an important share of banking sector assets, and it is even large relative to its capital base. Public debts are now estimated to represent 20.7 percent of the assets of the banking system, and 73 percent of its own capital base. Foreign exchange lending alone represents 11 percent of the capital of the banking sector. The rise in exposure to public debt has led to high rates of profit and returns on assets, due in part to rising interest rates. But at the same time, this increase in banks’ exposure to the state has led to a rise in the grave systemic risk of a default of public debt, which would severely affect the domestic financial system.

At the end of November 2023, the Central Bank too held a growing amount of public debt ($3.7 billion), an amount that had tripled in four years and come close to almost a quarter of the Central Bank’s balance sheet. In the past, the Central Bank purchased T-bills from the banking sector only as part of its monetary policy. But since 2020–2021, the Tunisian state has relied on direct financing from the Central Bank. This recourse—prohibited by the law on the independence of the Central Bank of 2016—took place for the first time in 2020, during the COVID-19 crisis, an exceptional period during which the state found itself unable to collect taxes to meet urgent expenses. A loophole, introduced in 2023, consisted of the state’s issuance of treasury bonds that were then automatically transferred to the Central Bank at zero interest. This was intended to comply with the letter of the law, which prohibits the Central Bank from lending directly to the Treasury. Faced with the exacerbation of the Treasury’s needs, at the start of 2024 the government submitted to Parliament a bill authorizing the Central Bank to lend the state $2.25 billion, which also included interest-free advances.

Separately, the fiscal crisis and the drying up of financial sources led to an accumulation of arrears for the state. The state stopped paying many of its suppliers, which is particularly noticeable in the stoppage of crucial construction and infrastructure projects, such as roads and bridges. According to experts and high-ranking bureaucrats, the arrears have been kept off the books due to the obsolete national accounting system, which registers payments only once they are made. This highlights the increasing risk of the politicization of Tunisia’s statistics, a critical issue that recently resulted in the dismissal of the director of the National Institute of Statistics (INS), who had published accurate figures regarding payments, angering the authorities. Since then, data has been scarce and made difficult to obtain by the government and the Central Bank.

Given the lack of external borrowing options and the weak capacity of Tunisian banks to absorb a large financing shortfall, 2024 is proving to be a risky and difficult year. By announcing that the budget provisions for 2025–2026 will be more restrictive, the government is effectively promising that the current largesse will last only one more year, to be followed, after the presidential elections of end 2024, by several years of tough adjustment. It is not clear how feasible this is, despite a government roadmap for restoringfinancial sustainability over the next two years. The plan is to halve the budget deficit by 2026—a goal in line with IMF recommendations—by reducing state expenditures, particularly when it comes to wages, subsidies, and social transfers. The crucial question is whether the financial sector can be kept from imploding until then.

2024: The Year of All Dangers

The change in the political setting from democratization to a restoration of authoritarianism has not put an end to the practice of increasing fiscal deficits to keep the economy afloat. Raising fiscal expenditures was initially a decision on the part of the power-sharing coalition that took charge after the 2011 uprising. Later, in 2020, the pandemic became a turning point in the management of Tunisian public finances: the budget deficit reached a high of 9.4 percent of GDP. Though decisive action was needed to correct a trajectory leading to financial chaos, Saied’s time in office, especially after the July 2021 “political coup,” has heightened unsustainability. Indeed, over the past three years, the fiscal deficit has hovered around 8 percent of GDP. Since Saied granted himself full powers, he alone is responsible for an economic policy that has abandoned all semblance of fiscal prudence. He has preferred to break with the IMF, even at the cost of losing nearly all of Tunisia’s traditional sources of financing, and resorted to monetizing a large part of the fiscal deficit, which risks an acceleration of inflation. This situation also raises worries about the outlook for Tunisian public debt—not just in the medium term, but even in the short term. At this stage, the outlook for the trajectory of the public debt remains uncertain. The most recent IMF forecast from April 2024 does not foresee a resumption of rapid growth. The IMF forecasts GDP growth at 1.8 and 1.9 percent for 2024 and 2025, respectively, even lower than the low levels achieved in 2021–2023 (2.7 percent). The IMF also forecasts that state revenues will continue to grow during 2024–2025, while fiscal expenditures will shrink as a share of GDP. This makes for a modestly optimistic scenario, as it would allow Tunisia to reduce its fiscal deficit over time, and, as a result, enable it to stabilize public debt at below 80 percent of GDP by 2025. The scenario envisaged by the Tunisian Ministry of Finance is broadly similar, but it foresees a slower growth in budget revenues in 2024–2026 (7.4 percent). Both scenarios could be described as realistic, if not for the constraints of domestic politics related mainly to Saied’s opposition to subsidies reduction, structural reform, resorting to the IMF, and privatization of public companies. These policies, together with the fact that fiscal expenditures grew at the high rate of 11.2 percent during 2021–2023, make it difficult for the state to implement deep adjustments, particularly in the short term.

A crucial driver of future scenarios is the behavior of the exchange rate. The robustness displayed by the Tunisian dinar in 2023 was undermined by the deterioration of public accounts, the reduction in foreign exchange reserves, and the government’s failure to resume dialogue with the IMF. Because the dinar has not been allowed to float since 2019, the real exchange rate has been appreciating—by an estimated 40 percent (accumulated inflation since 2019, in addition to eurozone inflation, has produced an over-valuation relative to the euro). This means that at some stage, one can expect to see a large adjustment, as happened recently in Egypt following the devaluation in 2024. Devaluation in Tunisia, if it takes place, would create complex adjustment challenges, as it would lead to a jump in inflation, a sharp reduction in real wages, and an increase in the domestic cost of servicing external debt. Moreover, in the case of devaluation, one would expect the financial sector to be weakened through balance sheet effects. First, foreign exchange loans to the state would shoot up, increasing sovereign risk. Second, Non-Performing Loans (NPLs) to public-sector enterprises would also rise, given that SOEs have a high level of foreign debt, in addition to their domestic exposure. According to the latest report on public enterprises (annexed to the budget law 2023), the debt of the main public enterprises has reached $7.2 billion, with $2.6 billion borrowed from Tunisian banks and the rest from foreign banks. The recent management of foreign exchange reserves has remained a mystery for analysts. Over the past three years, the reserves have fluctuated, suggesting that the Central Bank has benefited, at various times, from deposits made by external sources. However, there is no information on the amount, duration, or cost of these operations, let alone the date by which repayment must be made. More recently, the drying up of external financing has eroded foreign currency reserves: these have fallen from 150 days of imports in July 2021, to 125 days of imports over the first 9 months of 2022, to 92 days over the same period in 2023. Moreover, though the level of gross reserves officially stood at $7.4 billion in February 2024, there is much uncertainty regarding the level of usable reserves and net reserves at the Central Bank. What is clear is that the Central Bank must now draw more on foreign currency reserves to cope with the growing service of the external debt, as happened when it had to pay 850 million euros on a Eurobond that matured in February 2024. The debt service burden will only grow as Tunisia faces a repayment wall of several years—the debt service in 2024 alone will absorb almost all tourist revenues and transfers from the diaspora. Ultimately, poor access to international credits endangers the stability of the dinar, which risks sliding severely in the coming months. The Central Bank has pursued an accommodating monetary policy by keeping its key rate unchanged at 8 percent since the end of 2022. But the real interest rate is slightly negative. This is not helping to raise domestic savings, which have fallen to a historically low 8 percent of GDP, a fall mainly connected to the decline in incomes. In the short term, the rising expectation of a devaluation of the dinar, a step associated with low interest rates, risks pushing remittances down—with Tunisians abroad either awaiting a devaluation before transferring their funds to Tunisia or transacting in a parallel, informal market. This in turn could precipitate a run on reserves, leading ultimately to a sharp devaluation, which would set in motion a downward spiral. If such an occurrence is allowed to happen, Tunisia would find itself in a financial crisis that would be difficult to recover from, with the experience of Lebanon being the extreme case of what can happen when negative expectations are not rapidly addressed (see Box).

Conclusion

The Tunisian economy is now very much below its potential. Its problems are self-inflicted. Put somewhat reductively, the problem is a government that overspends to ease social conditions—an approach that keeps growth low. Now that external sources are drying up, fiscal deficits are using up domestic financing. This crowds out the private sector. It also builds up domestic public debt, which creates a risk of future instability, further depressing private investment. This situation leads to inflation, lower real wages, and high unemployment—all of which pushes the government to overspend. How to break this vicious circle has become the main national challenge.

In the immediate future, financing external and internal deficits will prove extremely challenging. On the external side, only $1.5 billion of the required $5 billion for 2024 has been sourced, leaving a huge financing gap. On the internal side, the large amounts of planned borrowing will not only continue to crowd out the private sector, but will also keep inflation up. The main danger to the current financial structure could come from a further rise in inflation. Inflation ultimately leads to devaluation, which would make the external debt more expensive to repay. More scarcity of foreign exchange would increasingly threaten to bring down the whole system—generating in particular more acute risks of a run on reserves, and possibly a run on banks as well, given their large exposure to public debt.

These conditions have rendered Tunisia highly vulnerable and at the mercy of the slightest shock, whether of external or internal origin. The current situation is tenable only in the very short term. Tunisia could conceivably claw its way out of debt through a big investment push, but this would require a vigorous change in domestic policies and a large support package from international partners. Tunisia is more likely condemned in the months ahead to choose between two painful options: resorting to the restructuring of its debt or embarking on a path of austerity with IMF support.

Lessons from Lebanon’s crisis

Since late 2019, a sudden stop of capital inflow has created a triple crisis in Lebanon: fiscal, banking, and balance of payment. As a result, there has been massive inflation, a major decline in standards of living, large real devaluation, a collapse of imports, the freezing of banking deposits, and a crippled state. GDP has fallen dramatically by about half, and over 50 percent of the population is now below the poverty line, as opposed to 21.5 percent before the crisis. The real cause of Lebanon’s crisis, and its deepening, is very much related to poor governance and politics; successive governments were unable to muster the discipline to avoid a predicted crisis and have been unable to put a credible stabilization plan together because of disagreements over how to distribute losses.

The civil war in Syria, which started in 2011, and Saudi Arabia’s decision in 2017 to rescind its “implicit guarantee” of stabilizing the Lebanese monetary system with bailouts whenever needed, both weakened the Lebanese economy. But the road to crisis was also paved with bad fiscal and monetary policies. Attracting foreign exchange to finance the debt and defending the Lebanese pound’s peg to the U.S. dollar became more expensive. High interest rates and an overvalued exchange rate increasingly taxed investment. A devaluation of the currency earlier would have prevented deindustrialization and supported investment and export growth. Instead, there was rent-seeking, which favored non-tradable sectors such as real estate and finance, where political privileges could be bestowed to the connected few.

Lebanon’s experience suggests lessons as to how to avoid a crisis. The solution is to reduce deficits to low levels and keep the exchange rate at a competitive level. Addressing the economic woes requires reaching a political agreement on loss distribution while avoiding capital flight. This, in turn, requires protecting the poor, preventing contagion to the banking sector, and most importantly having a credible growth strategy that can back such a program, and that can create hope for a better future.

About the Authors

Ishac Diwan

Research Director at the Finance for Development Lab at the Paris School of Economics, Professor of Practice at the Department of Economics at the American University of Beirut.

Ishac Diwan is the research director at the Finance for Development Lab at the Paris School of Economics, Professor of Practice at the Department of Economics at the American University of Beirut.

Hachemi Alaya

Hachemi Alaya is an economist and the founding director of TEMA, a Tunisian think tank, and the editor of the macroeconomic newsletter ECOWEEK

Carnegie does not take institutional positions on public policy issues; the views represented herein are those of the author(s) and do not necessarily reflect the views of Carnegie, its staff, or its trustees.

More Work from Malcolm H. Kerr Carnegie Middle East Center

The armed forces champion a form of capitalism that is generating revenue, but its reliance on rent faces diminishing returns, leaving the country with massive sunk costs and deferred returns, deepening dependency on external borrowing.

Understanding how farmers in the Oued Sahel-Soummam Valley grapple with climate change is essential for addressing the paradoxes through which adaptation, operating at both individual and institutional levels, deepens the region’svulnerability and erodes the social fabric and agrarian identity that once defined life.

Unless the European Union-led energy transition provides economic development to Algeria, Morocco, and Tunisia, the process may be perceived as a new form of extraction.