{

"authors": [

"Zainab Usman",

"Alexander Csanadi"

],

"type": "other",

"centerAffiliationAll": "dc",

"centers": [

"Carnegie Endowment for International Peace"

],

"collections": [

"Africa’s Natural Resources in the Global Energy Transition",

"Climate Change",

"Africa’s Shifting Politics and Geopolitics"

],

"englishNewsletterAll": "africa",

"nonEnglishNewsletterAll": "",

"primaryCenter": "Carnegie Endowment for International Peace",

"programAffiliation": "AFP",

"programs": [

"Africa"

],

"projects": [],

"regions": [

"Southern, Eastern, and Western Africa",

"United States"

],

"topics": [

"Economy",

"Trade"

]

}

Source: Getty

Other

How to Advance U.S.-Africa Critical Minerals Partnerships in Mining and Geological Sciences

For the United States, the objectives of both increasing the volume of critical minerals supplies and diversifying the sources of these supplies could be advanced by developing collaborations with African countries premised on scientific and technical exchanges in the mining sector.

Critical minerals,1 such as nickel, graphite, manganese, cobalt, copper, and lithium, currently occupy a central role in global economic and geopolitical competition. Demand for these minerals is projected to skyrocket over the coming years, driven primarily by increased demand for renewable energy and electric mobility technologies. Depending on specific modeling assumptions employed, it is estimated that overall mineral demand will increase by a factor of between two and three by 2030 and continue to rise through 2050.2 For specific minerals, such as lithium and graphite, demand projections are even steeper. These demand surges create particular challenges given that the lead time for bringing new mines online—from discovery to production—currently takes an average of eighteen years globally.3

In addition to the energy sector, critical minerals also serve as necessary inputs for frontier technologies crucial to economic prosperity and national security. Gallium, germanium, and silicon, for example, are essential for the production of semiconductors,4 demand for which is forecasted to continue rising because of increased artificial intelligence (AI) applications and the associated proliferation of data centers.5

Beyond market supply and demand considerations, creating more diverse and resilient mineral supply chains is now a priority for most advanced countries.6 For the United States, both increasing the total volume of mineral supply and diversifying the sources of those minerals is imperative for economic and national security. Escalating export restrictions, including recently on gallium, germanium, and antimony, by China—which dominates the global supply of these commodities7—only reinforce this imperative.8 Correspondingly, the United States has framed the importance of augmenting its critical mineral supplies in economic and security terms.9 Much of the recent focus is aimed at increasing U.S. domestic supply of these minerals, particularly through permitting reform, support for expanding domestic production, and developing refining and processing facilities.10 However, there is also a clear signal of interest in complementary international engagements to achieve mineral supply and energy security.11 These engagements flow in both directions. That is, the U.S. government views international partners not only as potential sources of mineral inputs but also as potential recipients of U.S. energy and related technology exports.12

Mineral rich African countries arise as natural potential partners on both sides of this equation. With respect to inputs, taking copper as an example, the White House recently initiated a so-called “section 232” investigation to determine whether imports of copper—particularly from “a concentrated number of supplier nations”—pose a threat to national security.13 The concerns are not only over raw copper ore but also refined copper and concentrates. In 2024, China was responsible for an estimated 44 percent of global refined copper production, a far greater share than any other country.14 This was more than four times the refinery production from the Democratic Republic of the Congo (DRC) and Zambia combined, despite the fact that copper reserves in these countries are around two and a half times that of China’s reserves (and more than double that of the United States). Supporting the development of refining and processing capacity in the DRC and Zambia could therefore, alongside increased domestic production, help the United States alleviate its concerns around concentrated copper supply chains.

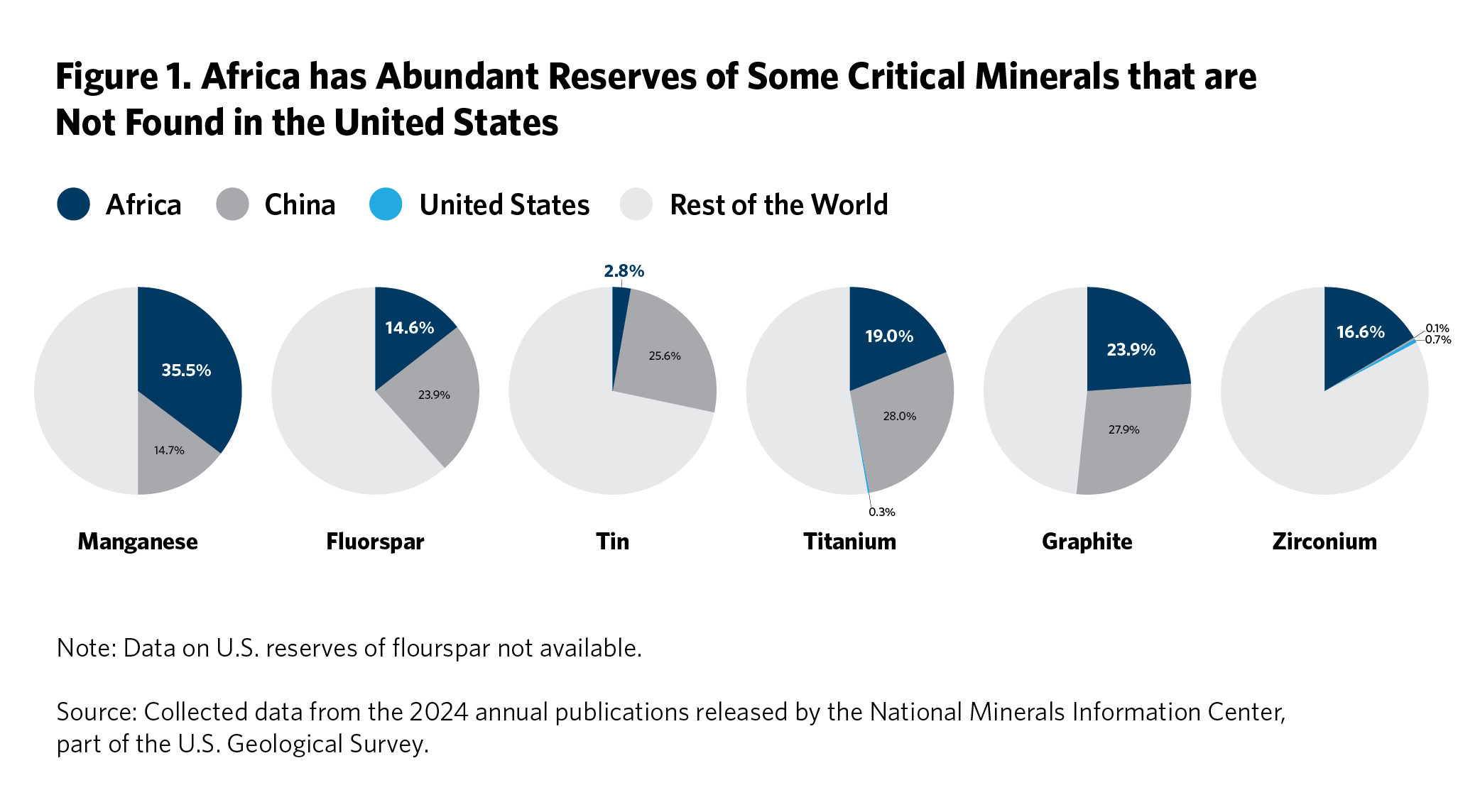

Similar potential exists for many other critical minerals, particularly those with which the United States is not endowed (see figure 1). Manganese, found in both South Africa and Gabon, the first- and second-largest producers in the world respectively,15 is a particularly compelling example: refined products like high carbon ferromanganese and silicomanganese are used in steelmaking, an industry identified by the current administration as critical for national security.16

From the perspective of African countries, U.S. engagement in mineral supply chain development would be welcome, provided it does not replicate the historical pattern of extraction of raw ore for export. Adopted by the African Union in 2009, the African Mining Vision (AMV) aims to achieve optimal growth and broad-based socioeconomic development from mineral resources by focusing on ensuring value addition and ultimately industrialization on the back of the mining sector.17 Additionally, the recently released African Green Minerals Strategy contains among its organizing structure a focus on industrialization through mineral beneficiation and mineral-based economic transformation.18 Similar language around the importance of value addition from minerals is contained in the relevant strategy documents of many mineral rich countries, including Zambia,19 Zimbabwe,20 and Tanzania.21

Among the constraints to African development of mineral beneficiation and manufacturing cited by the AMV is a lack of requisite energy infrastructure. The new U.S. energy secretary, Chris Wright, has spoken about the importance of energy in the lives of people not just in the United States but also around the world and the potential for U.S. energy technology to be adopted globally.22 In his remarks at the tenth annual Powering Africa Summit on March 7, 2025, Wright explicitly committed U.S. support for African energy.23 U.S. energy technology exports have the potential, therefore, to address the energy bottleneck and unlock the industrial activity African partners aspire to achieve, while augmenting the mineral supply chains necessary for downstream industry in the United States.

Another constraint to African countries fully exploiting their mineral resources is with respect to geological technology—from exploration to processing—and human capital. On both fronts, the United States is uniquely positioned to be an effective partner. The technical and training expertise contained within government entities, academic institutions, and private companies can be leveraged to help unlock the development of world-class mineral supply chains in African countries—to the benefit of all parties.

It is within this context that the Africa Program at the Carnegie Endowment for International Peace convened around forty high-level African and U.S. policymakers and leading members of the private sector in February 2025 during the Investing in African Mining Indaba Conference in Cape Town, South Africa. The roundtable had a clear mission: to brainstorm proposals for developing collaborations between the United States and African countries premised on scientific and technical exchanges in the critical minerals and mining sectors. The discussion produced ten core sets of ideas. Five outline the strategic case for leveraging U.S. technical and scientific expertise and the other five outline specific areas to consider in expanding this collaboration.

Why: The Strategic Case for Deploying U.S. Technical Expertise in Africa’s Critical Minerals

Africa is still under-explored geologically, and diversifying supply chains for the United States requires identifying and developing new deposits globally. It is frequently cited that Africa is home to an estimated 30 percent of the world’s proven critical mineral reserves.24 This figure is likely an underestimate, as many African countries have not been adequately geologically mapped, largely because of capacity constraints within geological survey organizations.25 This reality of under-exploration was emphasized by roundtable participants, who noted that some countries’ surveys dated back to the colonial period. Furthermore, geological mapping to identify new commercially viable deposits is made more critical as the grade of existing operations declines, especially for copper.26 The U.S. Geological Survey (USGS) is among the most highly regarded scientific agencies in the world and already works internationally with partner countries, including on geological mapping. Expanding collaboration between the USGS and mineral rich African countries to augment existing geological mappings would be in the direct interest of the United States as it continues seeking alternative sources for the minerals and metals necessary to secure its economic future. It would also benefit African countries seeking to design development strategies premised on their endowments.

The United States’ comparative advantage in mining and geological sciences can be the basis for a durable and effective collaboration. Beyond the USGS and geological mapping, the United States boasts world leading research centers within the Department of Energy’s seventeen National Laboratories as well as through academic and private sector organizations. Roundtable participants spoke about ongoing research projects related to mining innovations currently underway within the National Lab ecosystem and raised the possibility of collaborating with African partners through those projects or distributing findings to them. Relevant academic institutions include the Colorado School of Mines, which is home to the Payne Institute; Missouri University of Science and Technology, home to the Critical Minerals and Materials for Advanced Energy Tech Hub; the New Mexico Institute of Mining and Technology; and many others that conduct research on mining and mineral processing, including from nontraditional sources like tailings and recycled material.

There is overwhelming African preference for U.S. engagement and deployment of technical expertise over other external partners. Other countries host geological survey organizations, including the Geological Survey of Canada and France’s Bureau de Recherches Géologiques et Minières (BRGM) which operates across the continent. South Korea’s National Geographic Information Institute has also partnered with Tanzania in support of geoscientific investigations.27 Despite other countries’ geological science organizations and existing international collaboration, participants noted a general preference among many Africans for engagement with U.S. technical experts because there tends to be suspicion about the real or perceived motivations of technical agencies from Europe and Asia, with high levels of concern about lack of transparency in some cases. This preference is echoed in data from Afrobarometer that indicate Africans tend to view the political and economic impact of the United States much more favorably than that of former colonial powers.28

Certain segmentsof select mineral value chains, particularly midstream processing and refining, should be located within specific African countries to reduce costs and vulnerabilities. The United States is looking to secure the necessary inputs for downstream manufacturing in support of its economic and defense industrial base. While some of these inputs—processed and semi-processed minerals and metals—may be commercially produced domestically, generally the comparative advantage of U.S. industry lies further down the value chain. African countries can provide a cost competitive, diversified source of inputs for U.S. industry. Today, raw ore is often extracted from African countries and then shipped overseas for processing and refinement. This creates cost inefficiencies because of high transportation costs and exacerbates supply chain vulnerabilities. Locating midstream activities closer to the source of raw material can solve both challenges. Traditional impediments to locating these facilities within African countries include prohibitive capital and operating expenses and high energy and water demand, particularly for pyrometallurgical techniques. Innovative technology originating from the United States has the potential to disrupt this status quo. At least one U.S.-based company is already utilizing cutting edge techniques to operate efficiently on the African continent.29 Concerted expansion of this type of industry could unlock cost competitive economic activity throughout the continent and contribute to resolving acute supply chain challenges for the United States, including for battery technologies and defense applications. Additionally, participants noted that some cost analyses indicate that certain manufactures, particularly battery precursors, could be produced more cheaply in Africa than in the United States or Europe. Supporting the development of this segment of the battery value chain in Africa would complement the U.S. objective of building out its own battery production facilities, by allowing the country to focus on downstream activities like modules and battery packs.

Training future miners, engineers, and geologists in Africa is in the United States’ interest. Cultivating the African continent’s human capital base to manage a resource-based economic ecosystem is critical for durability and reliability. Participants noted that, when developing their national strategies, African countries must consider the fact that it typically takes ten to fifteen years for full training programs to yield impactful results. The USGS is well-positioned as a partner here, as capacity building is integral to its existing international work. In addition to on the job training, the USGS partners with U.S. academic institutions, such as the Colorado School of Mines, to facilitate longer term training. During the discussion, roundtable participants also highlighted existing training programs with U.S. academic institutions, like New Mexico Institute of Mining and Technology. Land-grant universities with a focus on mining or mineral processing could also be potential partners on this front.

How: Recommendations for Expanding U.S.-Africa Technical Collaborations in Critical Minerals

U.S. entities and agencies can collaborate with African countries to expand and update geological mapping. Many African countries, even those with a long history of extractive industries, have incomplete or insufficient geological data. While these countries have competent and motivated geologists, they are often limited by issues of capacity and access to the latest technologies. Technical support from relevant U.S. government agencies and other partners to shore up these data is in the direct interest of both parties: African countries may more accurately design their mineral-based economic developments strategies and U.S. policymakers seeking increased and alternative sources of supply for critical minerals and metals will be better able to craft holistic partnership frameworks.

U.S. technologies and expertise can enable the harvesting of crucial information from African countries’ existing geological data. Improved geological data is essential for both the United States as it seeks to identify sources for diversifying its mineral supply chains and African countries as they seek to attract investment and build out their mineral value chains. Although shoring up African data is essential, even the relatively incomplete and older data that exists within African ministries can be made useful. Participants noted that there is more data within African countries than commonly believed; however, it is often siloed across agencies or in forms that are not amenable to commercial analysis. AI applications and machine learning techniques could quickly assess these datasets and identify potential deposits, even in areas that have been previously examined. U.S.-based entities are already working in this space on the African continent.30 The U.S. Department of Energy is also developing similar technology across the National Laboratories and within the Defense Advanced Research Projects Agency (DARPA).

A focus on the mining value chain’s midstream—refining and processing—can support African countries’ industrialization objectives and meet U.S. needs for supplier diversification. U.S. industrial activity requires processed mineral inputs—silicomanganese for steelmaking, cobalt sulfide and spherical graphite for batteries, and neodymium for magnets, to name a few—and African countries are seeking to support their industrialization by producing these midstream products. In their resource-based engagements, U.S. partners must therefore meaningfully supportactivities that add value beyond extraction and export of raw materials. This means they should support ancillary economic infrastructure beyond just transportation (although this is welcome) to include energy generation and other activities. They should also think intentionally about creating jobs at different skill levels and connecting mineral engagements to wider economic development and industrialization objectives. Additionally, the approach to value addition must progress in phases, beginning with segments of the value chain that are commercially and industrially viable, rather than leaping directly into advanced manufacturing. Cultivating this ecosystem will require a deft touch. Standard tax breaks to incentivize investment may be useful, but they will not be a panacea. Ensuring downstream offtake arrangements can help reduce risk, but securing sufficient upstream feedstock is equally important. While certain targeted trade restrictions may help galvanize development, blanket export bans alone risk cutting against the interests of mineral rich African countries by encouraging investors to seek other jurisdictions and incentivizing the development of substitutes.

Although there is scope for regional engagement with many African countries, there should also be flexibility in taking a bilateral approach in selective cases. U.S. engagements with African countries should connect to existing national strategies and frameworks and not devolve into a one-size-fits all approach.Many African countries share similar goals with respect to developing their mineral value chains. However, the levels of industrialization, energy access, and transportation infrastructure vary widely across countries, and these variations must be considered when tailoring international collaborations. Moreover, what constitutes a “critical” mineral differs across countries, and use cases for minerals change as technologies advance. Flexibility will be an important component of successful engagement, both across countries and over time.

African countries and partners must learn from past experiences. Mineral-based industrialization strategies in Africa are not novel, and lessons from past attempts are important for guiding policymaking today. Participants recalled how the African Minerals Skills Initiative,31 launched in 2009 as a collaboration between governments and the private sector to train geologists, ultimately vanished in the wake of commodity price cycle fluctuations and other challenges. Similarly, the African Minerals Geoscience Initiative once sought to make the entire continent’s geological data available, but broke down because of countries’ concerns about data ownership.32 Participants suggested that insulating contemporary efforts from short term commodity price fluctuations and, importantly, resolving tensions related to data access for the purpose of attracting investment and national security imperatives will be key to ensuring the long term viability of resource-based industrialization in Africa.

Definitions of “critical minerals” vary across countries (and even between government agencies) and evolve over time. The term is used here in the broadest sense to refer to the full suite of minerals and metals that are used in the manufacturing of various hardware, including batteries, renewable energy components, semiconductors, and defense industrial products.

“Opening Remarks by the Deputy Minister for Minerals Hon. Steven Kiruswa (Mp) at the African Minerals Geoscience Initiatives (AMGI) Technical Workshop on 30th August 2022 at Hyatt Regency Hotel in Dar Es Salaam,” Republic of Tanzania Ministry of Minerals, August 30, 2022, https://www.madini.go.tz/media/SPEECH_FINAL.pdf.

Afrobarometer Round 10 (2024-2025), Section M: Regional and global relations. The survey question asked, “Do you think that the economic and political influence of each of the following countries on [country] is mostly positive, mostly negative, or haven’t you heard enough to say?” Afrobarometer Online Data Analysis Tool, accessed March 2025, https://www.afrobarometer.org/online-data-analysis.

Carnegie does not take institutional positions on public policy issues; the views represented herein are those of the author(s) and do not necessarily reflect the views of Carnegie, its staff, or its trustees.

More Work from Carnegie Endowment for International Peace

Does Donald Trump want to redraw the map of the world? Historian and geopolitical thinker Stephen Wertheim tries to parse the logic behind current American foreign policy

Is the Gulf moving beyond the dollar? This article examines how China is expanding the renminbi's role across Gulf markets, what that means for regional finance, and why the future of global currencies is more complex than the de-dollarization debate suggests.

As India undergoes a demographic transition, its cities will be its economic powerhouse—but only if it accurately captures city growth and empowers cities to support their citizens.