Article

Sarah Labowitz, Katie Mears

Source: Getty

The rising pace and cost of disasters is cause for alarm, both because of the likelihood of major disruption in so many people’s lives, and because of the potential for systemic failures in the housing and insurance markets that could lead to wider, global economic shocks.

Please note that the Disaster Dollar Database was expanded and updated in February 2025. See the dedicated website for the database here.

In the first half of the twenty-first century, the world has experienced two primary economic shocks: the 2008 subprime mortgage crisis that started in the United States and became a global recession, and the COVID-19 pandemic that battered the world economy in 2020. There is a third, looming shock that is already starting to play out: a housing and insurance crisis fomented by climate disasters.

This is an acute threat to the United States. The United States experiences more disasters than other countries. Its policy ecosystem for recovering from disasters was architected over the last forty-odd years, with the premise that catastrophic disaster events are rare, even once-in-a-lifetime events. But that premise is not holding up as the cost and frequency of disasters rapidly increases. In 2023 alone, the United States had a record-breaking 28 “billion-dollar” disasters, in which total losses exceeded $1 billion. The rising pace and cost of disasters is cause for alarm, both because of the likelihood of major disruption in so many people’s lives, and because of the potential for systemic failures in the housing and insurance markets that could lead to wider, global economic shocks. We already are seeing early signs of stress, as homeowner's insurance is becoming almost prohibitively expensive for many people, if they can find a company to buy insurance from at all.

Omar Soloman (left) and Keysha Hill gather what is left of his shop after it was destroyed when Hurricane Beryl passed through the area on July 4, 2024 in Old Harbor, Jamaica. (Photo by Joe Raedle/Getty Images)

Senator Sheldon Whitehouse from Rhode Island has been warning of the risks of a coastal property value crash that “could hit the American economy as hard as the 2008 mortgage meltdown and subsequent global economic crisis: first, insurance crisis; second, mortgage crisis; third, coastal property value crisis.” As the Economist wrote in April 2024, on the eve of what is predicted to be a historic hurricane season, “climate change, in short, could prompt the next global property crash.”

Given its leading position in the global economy and the sheer number of high-cost disasters that happen in the United States, is the country preparing for the looming crisis? One answer lies in the amount of reactive funding the federal government is already spending to absorb the uninsured costs of disaster shocks. This is after-the-fact funding to individuals, households, and jurisdictions that can be deployed to improve resilience going forward. Federal grantmaking for disaster recovery—including funding targeting low- and moderate-income households and communities—is a unique feature of the U.S. disaster response system, but it is almost impossible to visualize the full scale of this spending for any given disaster incident.

Carnegie’s Sustainability, Climate, and Geopolitics Program is trying to help make the picture clearer. We’ve built a Disaster Dollar Database of disaster spending since 2015 that collects data on federal grantmaking to individuals, as well as state and local governments. This database does not encompass the full range of federal responses to the potential for a climate-driven property value crisis, but it makes visible a key piece of reactive federal spending that previously has been very difficult to see.

Understanding this kind of funding is important because the cost of a “billion-dollar disaster” is not disaggregated: responses occur through a mix of insurance payments, charitable donations, business and personal losses, and government spending. This database makes visible the largest pots of federal grantmaking to absorb uninsured disaster losses.

The database does not make value judgments about the effectiveness of this spending in driving desirable outcomes, either for people, climate stability, or national resilience. The premise of the database is that federal spending will be part of an adaptive national strategy to blunt the effects of a volatile climate, and that we should understand where and how much a large government like the United States is currently spending to absorb the uninsured costs of disaster shocks.

The database includes the largest disasters: those for which the Federal Emergency Management Agency (FEMA) authorizes its Individuals and Households Program (IHP) to provide funding to families recovering from fires, floods, tornadoes, hurricanes, or other disaster incidents. It includes 170 incidents, from 2015 through May 2024. (Note that FEMA data in the database is based on Freedom of Information Act (FOIA) requests, the latest of which was made at the end of May 2024. Data for the most recent storms will be updated in future iterations of the database.)

In its first iteration, the database includes the two largest federal agencies involved in grantmaking to individuals and communities: FEMA and the Community Development Block Grant-Disaster Recovery Program (CDBG-DR) of the Housing and Urban Development (HUD) Department. Of the 170 incidents for which FEMA opened its Individuals and Households Program, 94 also had funding appropriated by Congress to be administered by HUD as grants made to states, local governments, and tribes.

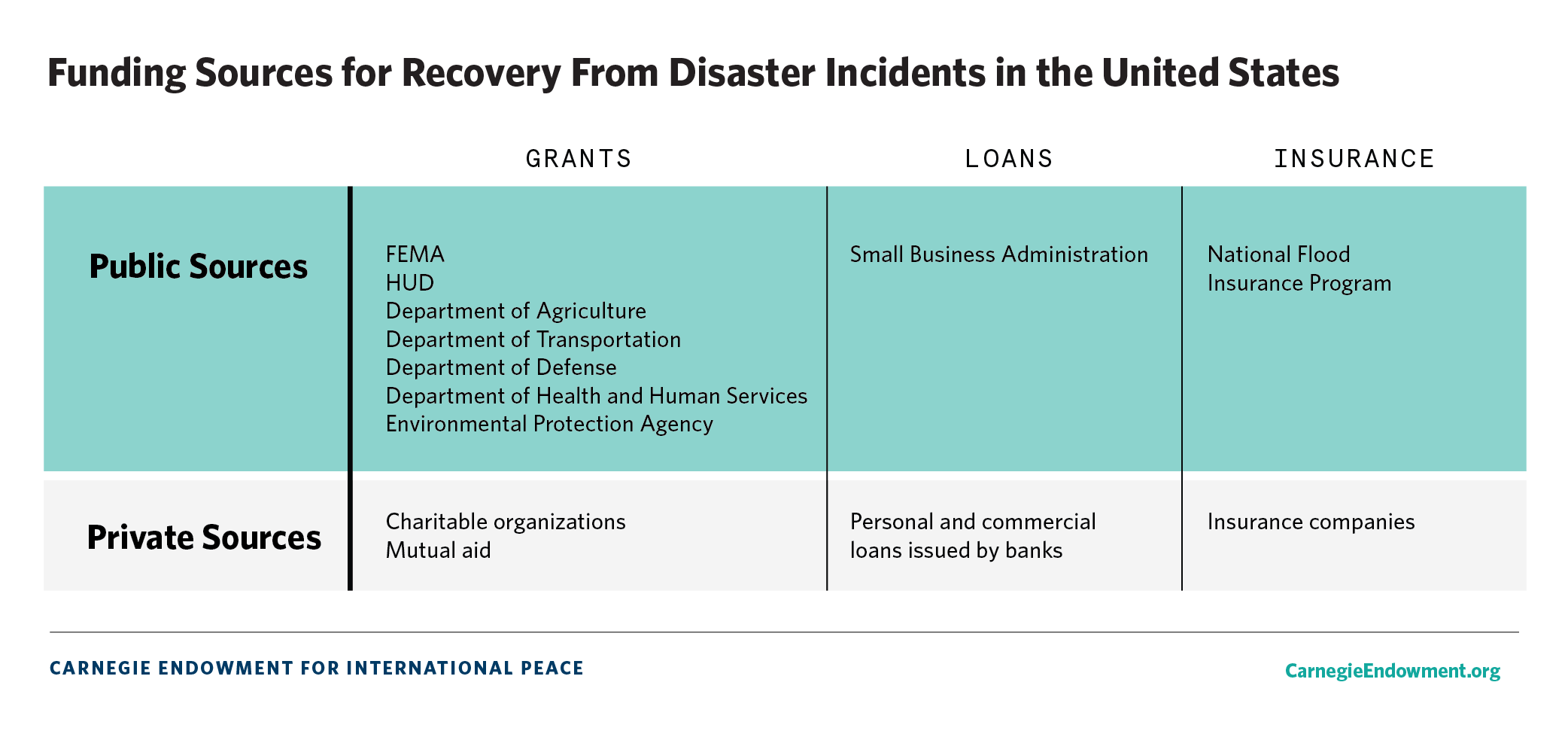

In the U.S. system, there are a range of federal departments and agencies involved in disaster recovery, though their participation varies from incident to incident. They include: The Departments of Agriculture, Defense, Transportation, and Health and Human Services; the Environmental Protection Agency; and the Small Business Administration. The database does not (yet) include these agencies because of challenges in creating apples-to-apples data that tracks spending at the incident level.

Understanding how the government spends right now to respond to climate shocks is a first step that will enable further analysis about whether that spending is working to prepare the United States for the coming housing and insurance crisis, and if not, to develop better policies that encourage the kind of resilience that will be required for the second half of the century. For example, it could be possible to reimagine our expenditures to focus on keeping people safe in the first place, by incentivizing development in safer places, conditioning federal expenditures on updated building codes and land-use planning, or announcing that funds will be devoted to steadily decommissioning infrastructure in dangerous places. Given the weight of the United States in the global economy, the implications of U.S. resilience are potentially global. And policymakers in the United States and other advanced economies will need to learn from each other to develop national strategies of resilience.

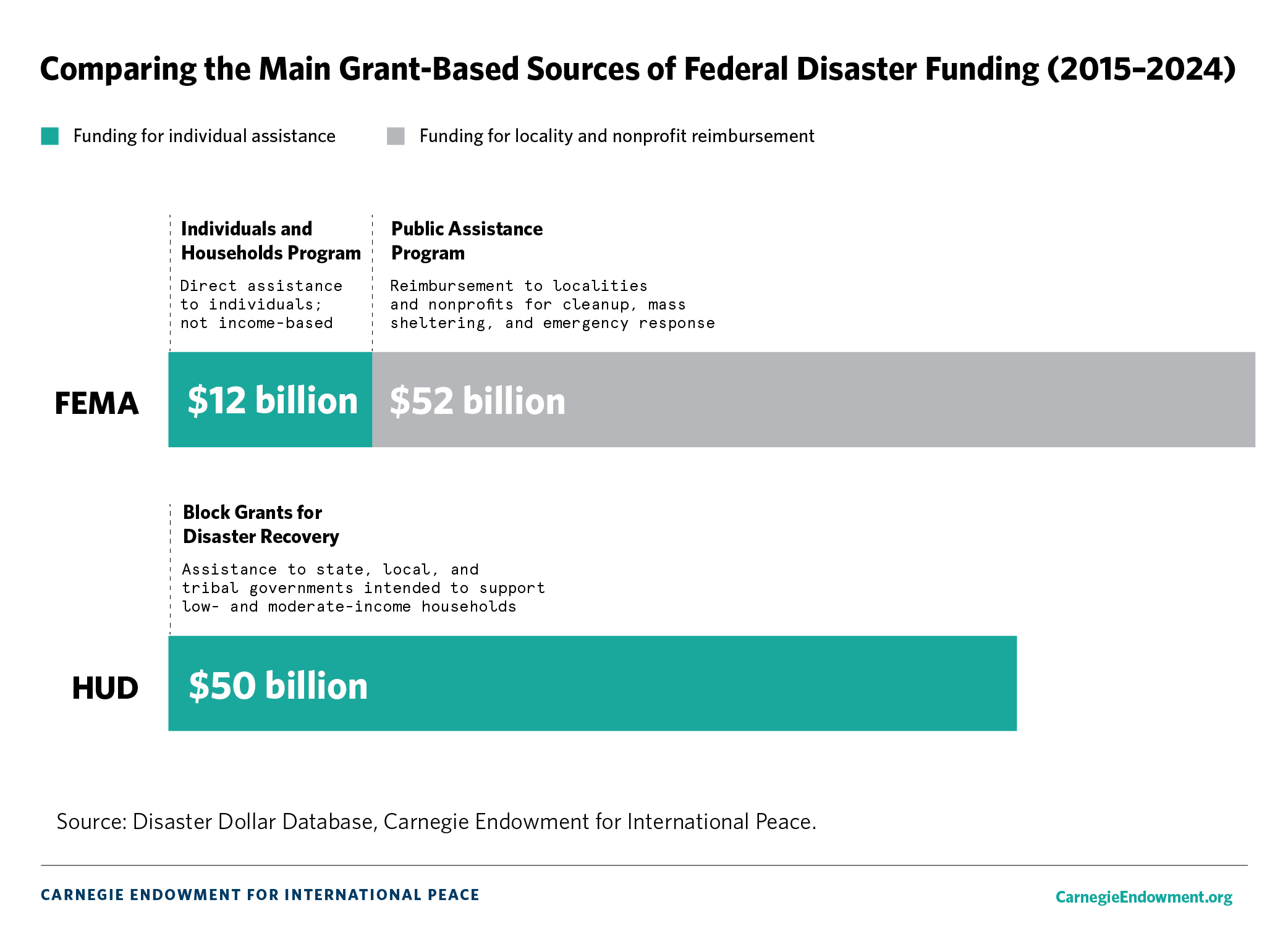

From the perspective of a disaster survivor, FEMA is the face of the response. It deploys to disaster zones and opens applications for assistance directly to homeowners, landlords, and sometimes renters. The program is designed to cover uninsured losses and is not income-based.

But the Individuals and Households Program is only about 18 percent of FEMA’s spending on large disasters since 2015. FEMA spent far more—$52 billion—through its Public Assistance Program on large disasters during the same period. Public assistance reimburses localities and nonprofits for debris cleanup, mass sheltering, and emergency response.

In addition, HUD has spent $50 billion since 2015 through its CDBG-DR grantmaking program to state, local, and tribal governments. This funding is especially important because it is intended to support low- and moderate-income households, who may not have the resources to rebuild or otherwise recover from insurance and FEMA payments alone.

CDBG-DR funding is an enormous source of support to communities, but it is not permanently authorized by Congress. In contrast, FEMA’s Disaster Recovery Fund (DRF) is statutorily authorized; think of it as a bucket that Congress can refill whenever it runs low, as it currently is (funding the DRF was also a key objective in the strategy to avert a government shutdown in 2023). For money to flow to communities through CDBG-DR, Congress has to make a special appropriation for each and every disaster, which creates delays and administrative burdens for grantees, according to the Congressional Research Service. There is no bucket at HUD that Congress can fill to anticipate an especially active disaster season, or otherwise prepare for multiple disasters before they happen.

In the absence of permanent authorization for this vital recovery program, HUD funding can be invisible. HUD and FEMA do not publish data according to consistent incident identifiers that would allow interested parties to track spending on an individual incident across agencies. The most authoritative way to ascertain HUD funding associated with FEMA incident identification numbers is by reading PDFs of Federal Register Notices, a time-consuming and cumbersome process.

At its most basic, the goal of the Disaster Dollar Database is to start to make visible federal spending on uninsured losses in disaster recovery, at the incident level. There is already a wealth of data available about aggregate agency spending. Rebuild by Design’s Atlas of Disaster and the Bipartisan Policy Center’s breakdown of CDBG-DR spending are examples of this kind of aggregated, single-agency reporting on disaster spending.

But blunting any housing, insurance, and economic crisis will likely happen, at least initially, in response to specific shock incidents. At the same time, the resources available to individuals and communities are, at the moment, tied to the effects of an individual incident according to FEMA and HUD rules. Understanding spending levels beyond a single agency, at the incident level can help policymakers, charitable funders, and disaster survivors make more informed choices in a high disaster-frequency landscape.

Through FEMA and HUD (and the host of other agencies contributing to federal disaster recovery spending), Congress is appropriating significant resources that could be used to temper the worst effects of climate disasters and even help people make better informed choices about where to live. But in the absence of a permanent HUD CDBG-DR program, some of the largest sources of funding aren’t made available for months or years after a disaster incident.

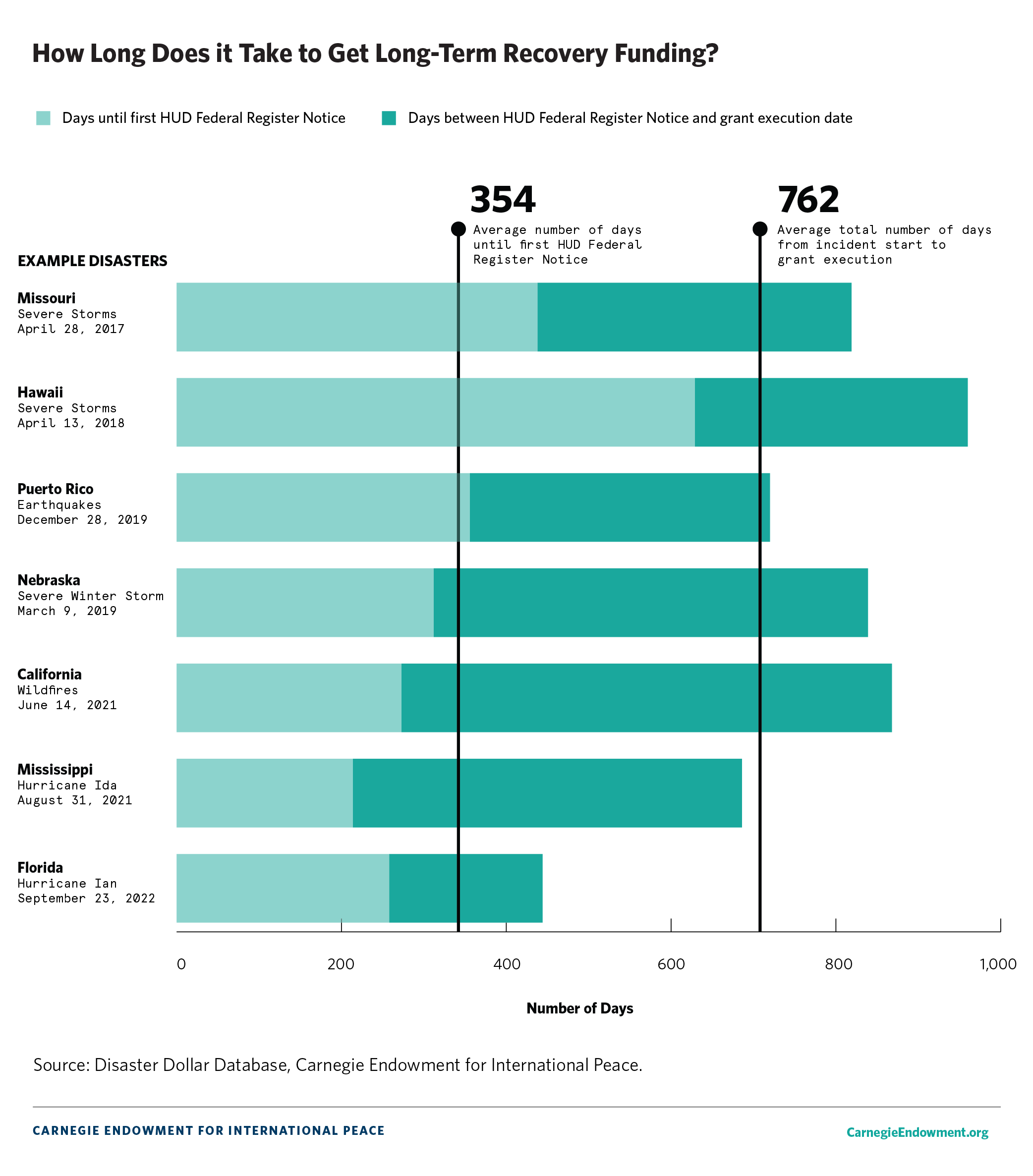

While Congress has appropriated $50 billion for CDBG-DR since 2015, there is a multi-step process to make this funding move from Congress to HUD, onward to state and local grantees, and then to households and to fund community projects. According to Carnegie’s dataset, it takes just under a year on average—342 days—from the date of the disaster until HUD publishes its guidelines for the rules that apply to that disaster in the Federal Register. From that point, there is still a long process of rule-writing, community consultation, and program design before HUD and the state or local grantee sign a grant agreement that allows spending to begin. Because HUD does not publish data about its grants according to FEMA incident identification numbers, it is not possible at this stage to include a grant agreement date in the database.

That said, we were able to get access to some grant agreement data that begins to give a snapshot of just how long it takes for long-term disaster recovery funding to move to communities. In a sample of seven disasters from 2017 through 2022, negotiating the grant agreement added, on average, about a year (354 days) to the process beyond HUD’s publication of the Federal Register Notice. In this sample, the total time from the start of an incident until grant execution was just over two years on average (762 days).

The premise of FEMA and HUD programs for disaster recovery is that funding is only available well after an incident has occurred. In the current framework for these programs, there is no way to spend money in advance to encourage people to move to higher ground safe from flooding, or out of fire-prone zones. Moreover, the rules require and incentivize rebuilding in place. The system is designed for property, not people.

The last time Congress appropriated money for CDBG-DR was May 2023, for storms that happened in late 2022 and January 2023. From then until late May 2024, there have been 23 disasters for which FEMA made available its Individual and Households Program. None of these have received long-term recovery CDBG-DR funding from HUD. Some of those disasters have been large, with almost 100,000 people applying for assistance.

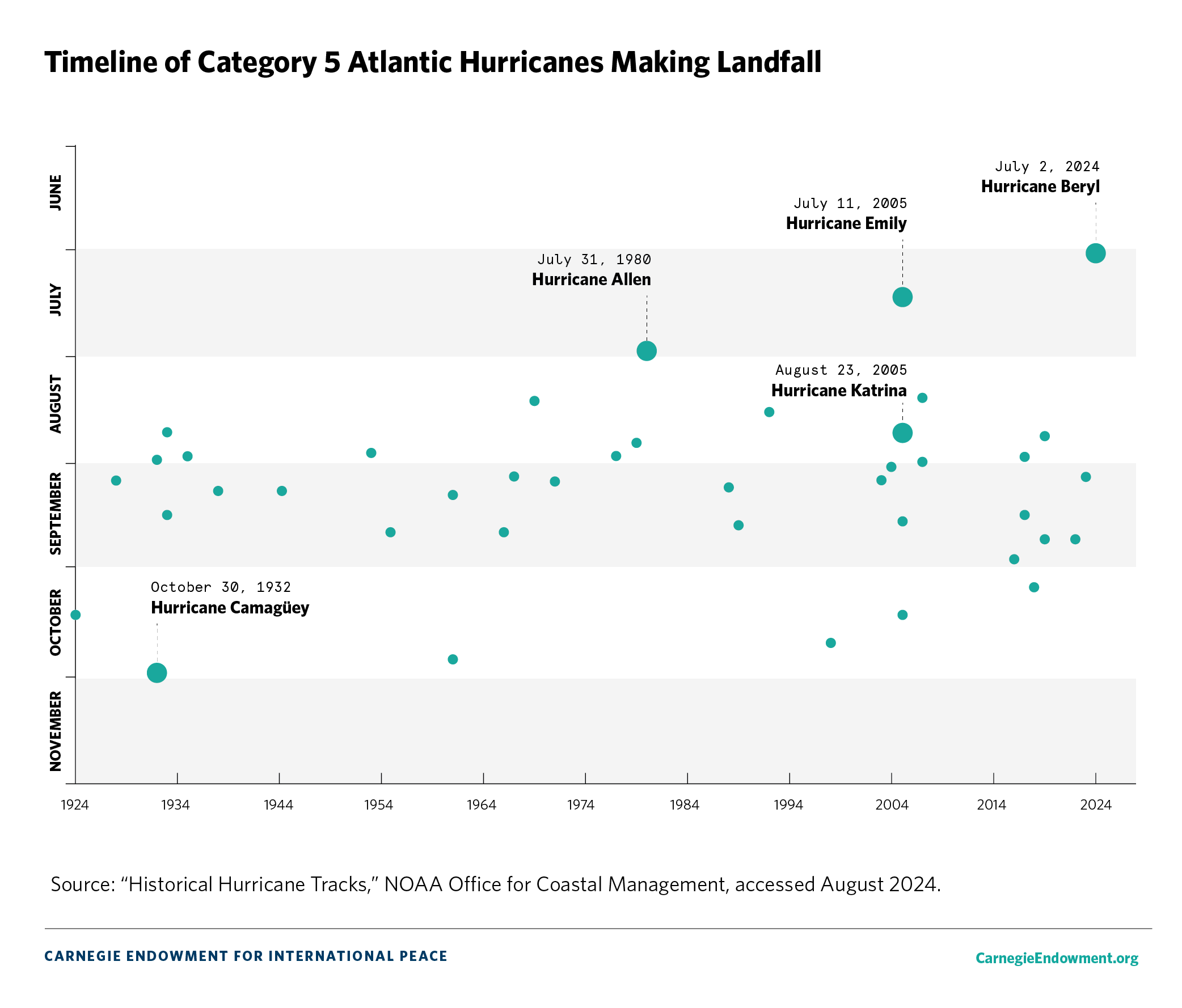

The summer of 2024 is predicted to be a historic hurricane season. The reality of the severe predictions came into focus in July, with the earliest category 5 hurricane ever to make landfall. Hurricane Beryl hit directly over Houston, knocking out power for 2 million people, many of them for a week or more. At least 64 people died in the storm, including deaths in Venezuela, Grenada, and the United States. While FEMA has deployed its programs for this and other storms since 2023, there will be no long-term funding designed to support low-income survivors until Congress makes special appropriations for CDBG-DR.

Early August 2023, wildfires swept through Maui, killing at least 102 people and devastating the house stock in the area. The official U.S. Department of Commerce damage estimate was $5.5 billion. For this and other disasters in 2023 and 2024, Congress has not appropriated any long-term recovery funding through HUD’s CDBG-DR program. Photo: U.S. Customs and Border Protection.

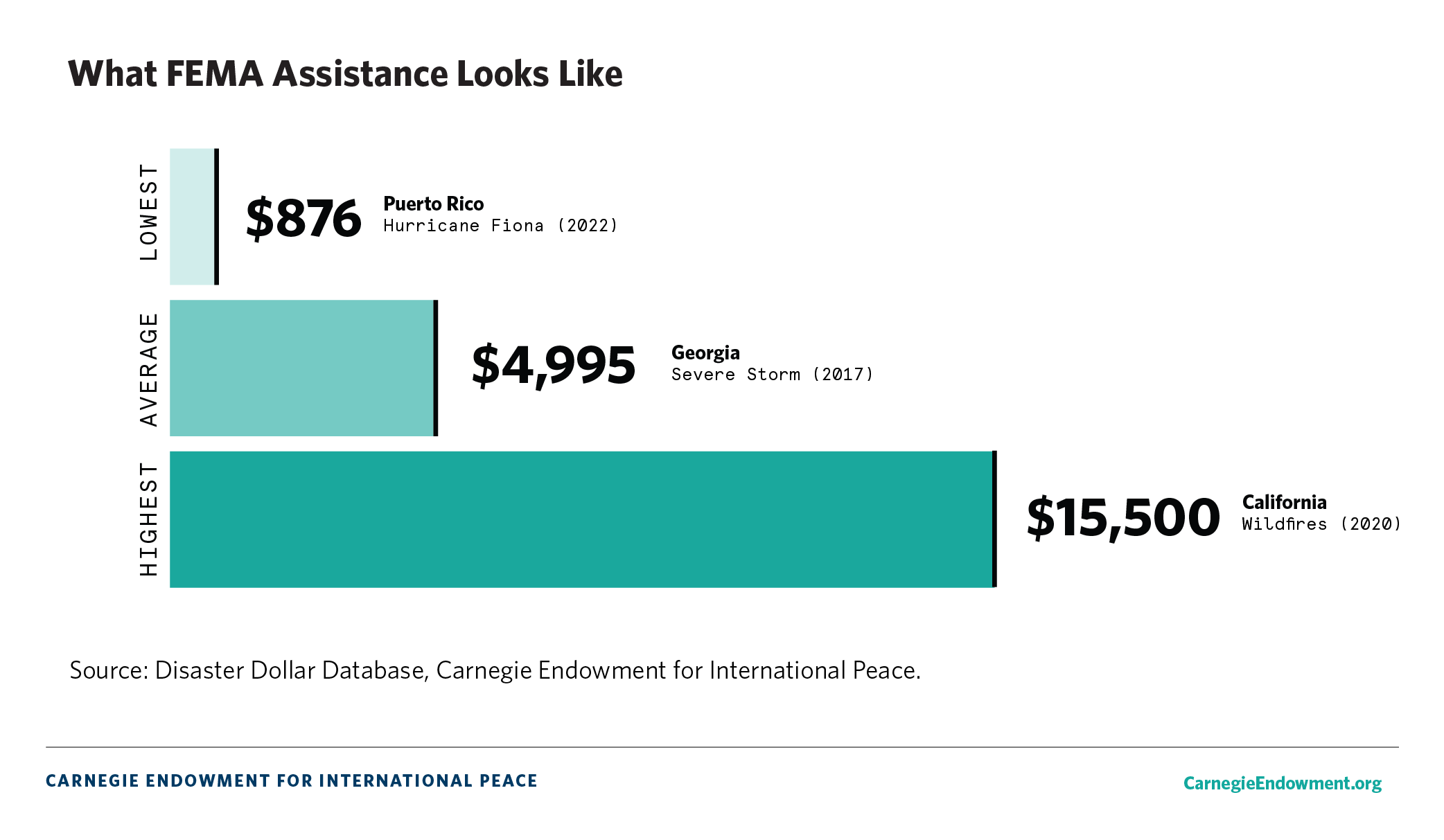

Since 2015, across 170 disasters, the median average assistance amount per approved application from FEMA’s IHP is $4,995. On average, just 39 percent of applicants are determined to be eligible for IHP.

While these programs can be a lifeline, the benefits are nowhere near enough to encourage households to rebuild differently or elsewhere, even accounting for payouts from insurance (assuming households can find an issuer) or charitable contributions. And there is evidence that FEMA assistance actually widens the racial wealth gap by as much as $80,000 between Black and White households in disaster-affected counties.

FEMA doesn’t reliably report the reasons that people withdraw or are denied assistance, but applicants are often denied because of a lack of documentation, as well as “insufficient damage.” Assessments of damage are notoriously subjective, especially in undervaluing the damage to homes of low-income households. FEMA’s denial rates have been the subject of significant public pressure by disaster survivors and Congress.

The data is available for download via Google Sheets here. Researchers, journalists, policymakers, government officials at the state and local level, and community organizers can use the data to better understand the impact of disasters and what is available to the people and communities who live through them.

The data can be sorted by year, incident type, state, dollar amount, and many more factors. Our hope is that the data helps drive better and more equitable disaster recovery policy in the United States and provides context for those around the world dealing with climate disasters and seeking to understand the U.S. model.

Carnegie’s Sustainability, Climate, and Geopolitics Program published the first iteration of the database in August 2024. The database was developed by nonresident scholar Sarah Labowitz, with support from Emily Hardy and Dan Helmeci, 2023–2024 Carnegie junior fellows. It draws on data from FEMA’s disaster declaration database, HUD’s Federal Register Notices for its CDBG-DR program, and FEMA’s response to FOIA requests. Our intention is for the database to be updated around December 1 and June 1 each year.

Senior Fellow, Sustainability, Climate, and Geopolitics Program

Sarah Labowitz is a senior fellow in the Sustainability, Climate, and Geopolitics Program whose work lies at the intersection of climate, national security, and democracy.

Recent Work

Sarah Labowitz, Katie Mears

Sarah Labowitz, Debbra Goh

Carnegie does not take institutional positions on public policy issues; the views represented herein are those of the author(s) and do not necessarily reflect the views of Carnegie, its staff, or its trustees.

The hybrid warfare landscape is evolving rapidly, leaving policymakers without clear strategies. To better inform their work in addressing emerging challenges, governments must dig deeper into the underlying dynamics at play.

Raluca Csernatoni, Alicia Wanless

Direct democracy is the political wildcard in the state’s midterm election.

Mark Baldassare, Ian Klaus

Despite the agreement’s uncertainty, it’s still a significant development in regional and nuclear policy.

Andrew Leber, Jane Darby Menton

“AI safety in parallel” is modest and pragmatic but vital.

Matt Sheehan

Trump is distracted and Ukraine wants Europe to step up. The continent’s leaders must find their voice and assert it in talks with Russia.

Alissa de Carbonnel