Paper

Networks—from international payments platforms to key economic sectors—underlie many aspects of U.S. power. But they are suffering under an extractive approach to foreign policy.

Daniel W. Drezner

Source: Getty

American power is entrenched in Europe. Yet the depth of this relationship has become a source of unease in Europe and Europeans are working to reduce their exposure to the vicissitudes of U.S. politics wherever they can.

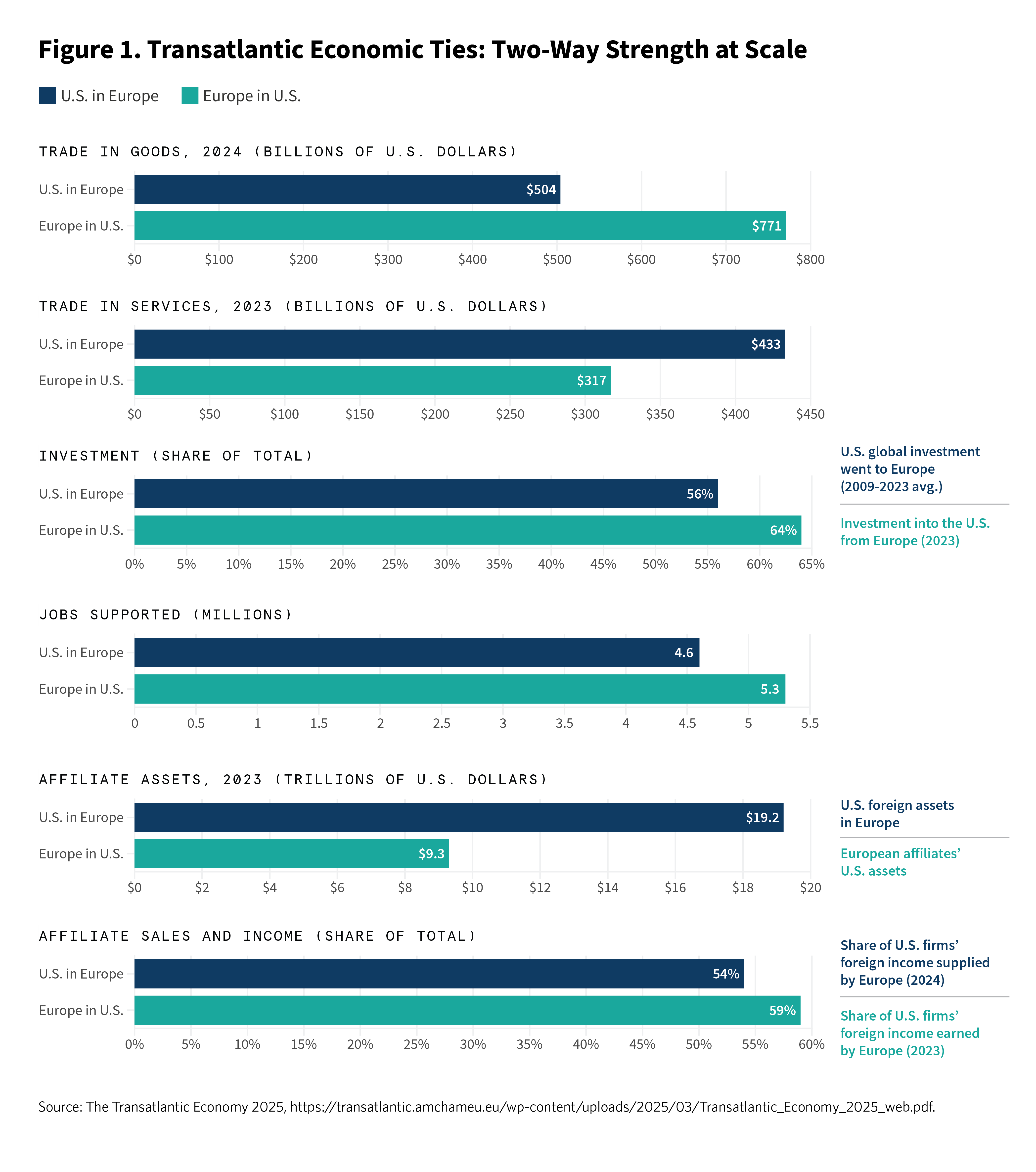

American power is entrenched in Europe. Some 70,000 U.S. soldiers are garrisoned at bases across the continent.1 American firms control 70 percent of Europe’s cloud computing market and supply the chips, artificial intelligence (AI) models, and connectivity services that underpin Europe’s digital future.2 The European Union (EU) is the United States’ largest trading partner, and transatlantic exchanges employ more than 16 million people—4 percent of the combined U.S.-EU labor force.3 European investors hold $15 trillion in U.S. financial assets,4 and the dollar still anchors Europe’s global trade. By every material measure, the United States is woven into Europe’s strategic, economic, and technological fabric.

Yet the depth of this relationship has become a source of unease in Europe. U.S. President Donald Trump’s claims on Greenland, his administration’s support for Europe’s far-right parties, and his willingness to abandon Ukraine and accommodate Russia have badly undermined Europe’s confidence in Washington. Europeans today see their relationship with the United States as weakened, and they suspect that America may have hostile intentions.5

To protect themselves in the face of such uncertainty, Europeans are working to reduce their exposure to the vicissitudes of U.S. politics wherever they can—diversifying spending, procurement, and trade; building digital, financial, and defense sovereignty; and courting new partners, including recalibrating relations with China. Senior European officials now openly discuss “insurance options” that would have been unthinkable a few years ago: a European nuclear deterrent as an added layer of reassurance to Washington’s extended deterrence, a payments system that circumvents the dollar, so-called Made in Europe defense procurement that cuts out American defense companies, and escape hatches from the imposing dominance of the U.S. tech stack.

Is American power in Europe about to run out as a result? No, but major changes are underway. The post-1945 transatlantic bargain—in which a benign American hegemon underwrites European order in exchange for political deference—is no longer tenable. Yet in many ways, that bargain was always exceptional. Instead, a more normal relationship could be emerging between asymmetric partners with overlapping interests.

American power in Europe will evolve and decline in some areas, but the United States will retain substantial leverage over European nations, which have few alternatives for the foreseeable future. As artificial intelligence becomes foundational to economic output and military power alike, technological dependence may overtake security as Washington’s greatest leverage, leaving even a more militarily autonomous Europe bound to the United States. A return to the levels of trust that characterized U.S.-European relations in the past may be desirable for the sake of stability and cooperation, but it will not be necessary to sustain American power as its relationship with this crucial region normalizes.

The future of U.S. power in Europe is thus a litmus test for a more coercive, transactional U.S. approach to regional partners: Can this new approach produce the same—or even more—cost-efficient results as the old alliance? Or will U.S. global influence decline as a result?

For most of the postwar era, U.S. power in Europe rested on two pillars: structural embeddedness and alliance-based trust. The former included bases, troop deployments, intelligence ties, market integration, financial links, and technological infrastructure. The latter revolved around Europe’s willingness to align with Washington politically and lend legitimacy to joint action. Together, they made American power in Europe both durable and efficient.

Any assessment of U.S. power in Europe must reckon with the disruptive and sui generis impact of the second Trump administration. But one man’s return to power should not obscure a larger point: Ongoing transatlantic tensions are the culmination of a U.S. foreign policy debate on two questions that predate Trump and will surely outlast him.

The first question is about efficiency: Can Washington preserve its influence while spending less? That question demanded attention when former U.S. president Barack Obama’s administration pivoted to Asia, and it has endured through arguments over whether Europe should shoulder more of its own defense. Russia’s invasion of Ukraine in 2022 revived the issue without resolving it.

The second question concerns alliance management: Should the United States lead through trust and negotiation? Or should it use its advantages in security, finance, trade, and technology to extract more from U.S. allies? One camp of analysts and policymakers sees coercive leverage as cheap and effective. Another warns that it erodes the consent and legitimacy on which lasting U.S. influence depends.

The Trump administration—in an often-haphazard manner—is currently testing whether pressure can deliver the benefits of alliance management at lower cost. This paper asks whether that bet can succeed. To that end, we examine American power in Europe across four domains: military, economic, technological, and soft power. For each, we also assess the constraints on that power—both the counter-leverage Europe can bring to bear and the domestic political limits on Washington’s freedom of action—and weigh the realistic alternatives available to Europe, including China, partnerships with other middle powers, and Europe’s own sovereign initiatives.

Europe is structurally dependent on the United States across trade, finance, energy, and payments systems. There is no obvious combination of third parties that could replace the United States in these areas. Nevertheless, Europe is learning to make U.S. economic coercion more costly. The EU’s threat to trigger its anti-coercion instrument during the January 2026 Greenland crisis, a market sell-off, and thin domestic support for Trump’s designs pushed the president to back off at Davos. Even unused, European leverage proved more than just theoretical. In the process, Europeans departed from their past practice of seeking deescalation with the United States. Future U.S. leaders will be less able to contemplate using their power without the specter of having to absorb real economic costs at home.

Economic interdependence generates prosperity on both sides of the Atlantic, but the asymmetric relationship gives more coercive potential to Washington. The United States vastly benefits from a coherent European single market that remains open to U.S. firms. The transatlantic economy is still the world’s deepest commercial relationship. The EU is the United States’ largest trading partner, and the transatlantic investment relationship is the largest in the world6—U.S. foreign direct investment (FDI) in the EU is close to four times its stock in the Asia-Pacific, and EU FDI in the United States is around ten times its combined investments in China and India.7

The density of these exchanges is what makes the transatlantic trade relationship unique: Washington has influence through market size and structural chokepoints. American economic power in Europe rests on dollar finance, energy supply, sanctions capacity, and the ability to connect security dependence to commercial negotiations. Political conflict since Trump’s first term has not reversed this.

The dollar’s reserve role and the centrality of U.S.-linked financial infrastructure allow Washington to impose costs faster than Europe can insulate itself. European leaders have discussed beefing up the euro’s international role, more joint borrowing through the EU, and greater financial autonomy, but these are long-term projects.8 For now, transatlantic finance remains anchored by America.

The energy sector provides the clearest illustration. Europe’s exit from Russian gas after the 2022 invasion of Ukraine traded one dependence for another, as U.S. liquefied natural gas (LNG) filled the gap. New terminals, pipelines, and long-term contracts have locked in that dependence on a multidecade horizon. U.S. supply has become both a commercial relationship and a political instrument, providing Washington with additional leverage over Europe. Alternatives are emerging—including Qatar,9 Norway,10 and an accelerated renewables buildout—but each carries its own constraints, and none rivals the scale, speed, or political alignment offered by the United States to Europe after 2022.

U.S. trade wars against Europe provide another useful illustration. In response to Trump’s threat of tariffs, Europe’s first instinct was accommodation. This was in part due to the breadth of American power,11 including the possibility that a trade dispute could escalate into an unrelated security crisis (such as the Greenland crisis in January 2026). Europe’s reticence produced the 2025 Turnberry deal, which has been criticized as lopsided and humiliating, and served as a reminder that economic and security ties can be linked.12 To keep the U.S. security guarantee over the continent and to ensure that Washington stayed invested in negotiations to end the war in Ukraine, the EU swallowed an asymmetric bargain with its largest trading partner. But repeated tariff threats have accelerated Europe’s hedging strategy. Europeans now believe that even if the relationship with the United States is inextricable, they must make coercion costlier for Washington.

Europe’s response to U.S. coercion has been to diversify its economic activity at the margins. The EU now has forty free-trade agreements with eighty partners and is negotiating another twenty-seven.13 Recent deals—with South America’s Mercosur bloc,14 Australia,15 India,16 and Mexico17—fit the logic of so-called friendshoring: move supply chains to countries deemed politically safer. The EU has also courted Japan as a partner, including in its Made in Europe scheme and as part of the so-called competitiveness alliance.18 None of these partnerships, individually or cumulatively, comes close to substituting for the transatlantic economic relationship; they widen Europe’s range of options rather than replace its core dependence.

China is not a credible alternative either. Despite being the EU’s third-largest trading partner in goods and services,19 the relationship is marked by systemic rivalry,20 large trade imbalances,21 and increasing concerns over Chinese competition in higher-value sectors such as electric vehicles, renewables, and pharmaceuticals—often referred to as the impending second China shock.22 Europe is also heavily dependent on China for critical raw materials; a move toward Beijing would only double down on existing vulnerabilities. China’s support for Russia’s war in Ukraine also remains a persistent thorn in Europe’s side. Beijing, therefore, has not emerged as a credible hedging option. The underlying competition between the European and Chinese economies suggests that even in the long term, closer ties will not deliver mutual benefit.

Europe’s internal response to all of this is its sovereignty agenda—the central idea in the Letta and Draghi reports.23 According to this approach, Europe must deepen the single market, build the capital-market union, coordinate industrial policy, and develop stronger external trade instruments to implement its geopolitical agency. The EU’s anti-coercion instrument is a key part of Europe’s newfound will to defend itself.24 While it remains untested—and internal divisions and fear of escalation will make its deployment difficult—it is the first meaningful attempt to create European counter-leverage against external pressure. The very threat of its activation against the United States was alarming enough to crash markets and convince Washington to—at least temporarily—ease its menace.

U.S. coercive behavior is pushing Europeans to diversify trade, discuss financial autonomy, and invest in sovereignty tools. Yet because no alternative partner can match the scale and quality of the transatlantic relationship, American power in Europe remains largely unchanged. The key shift has been political: Europe is learning not how to leave the relationship, but how to raise the price of dependence.

American military power in Europe is declining in relative terms. The United States retains significant leverage for now, but it is eroding. Europe’s current rearmament is unprecedented in scale and ambition, backed by the broadest political consensus in postwar Europe: Procurement patterns are shifting away from U.S. systems, regional defense-industrial cooperation is gathering pace, and Europeans are rethinking their nuclear deterrence options. Europe’s progress on the military front is slowed by national procurement instincts, North Atlantic Treaty Organization (NATO) planning built around U.S. capabilities, and Washington’s lack of clarity about its national security interests in Europe and the extent to which it can accept European defense industrial autonomy. Nonetheless, there is an unquestionable sea change underway as Europe moves toward security and defense autonomy.

No actor outside Europe comes close to substituting for the role of the United States as security guarantor, and no single European country can expect to fill the leadership vacuum alone. The United States retains roughly 70,000 personnel, more than thirty permanent bases, and additional rotational deployments across Europe.25 Washington has long acted as NATO’s central member, leveraging that position to shape European defense and deterrence planning, encourage transatlantic procurement, and project power into the Middle East and beyond from European bases.

European militaries remain deeply dependent on this architecture. Beneath the U.S. nuclear umbrella, which covers deterrence at the highest level of escalation, sits a dense layer of dependencies built up over decades through NATO planning: strategic intelligence, surveillance, and reconnaissance (ISR) and early warning; ballistic-missile defense; suppression of enemy air defenses; long-range precision strike; and a largely American command-and-control backbone. Capability dependencies are often reinforced by export controls, which allow Washington to govern not only what weapons European states buy but how they use them and to whom they can sell.

The Trump administration has advanced an agenda of so-called burden shifting and a reduction of the United States’ conventional footprint in Europe, while at the same time instrumentalizing threats of withdrawal—especially the abandonment of all aid to Ukraine—to win a bargaining advantage (resulting, for instance, in a favorable trade deal with the EU). But Washington’s ability to credibly threaten massive military retrenchment as a coercive tool is constrained by national interests. American power projection is supported by European bases, overflight rights, and logistical networks—demonstrated by the Trump administration’s recent efforts to rely on allied bases during the 2026 Iran campaign. Additionally, NATO offers U.S. leaders not only deterrence against Russia, but also leverage, an open arms export market, and ready-made stages for performance.

Despite the United States’ outsized military role, Europe’s collective pursuit of defense and security autonomy is advancing quickly and reducing Washington’s importance and leverage. The European rearmament project is massive. EU member states spent $402 billion on defense in 2024—a 19 percent rise from the previous year—and are projected to have spent $445 billion in 2025.26 Germany’s transformation is the most striking: Berlin plans to reach $205.4 billion by 2030,27[AB1] up from roughly $125 billion in 2026 and only $58 billion in 2022.28 The political consensus underwriting these increases is unprecedented in postwar Europe. Several European countries are seriously considering or have already reintroduced compulsory military service.29 Battlefield advances in Ukraine are accelerating European innovation in drones and electronic warfare.

The bottleneck today is no longer money but political coordination. Countries with mature defense industries channel new funds toward national champions rather than pooled European procurement, while countries without primes buy wherever there is fast availability—often from non-European suppliers. There is no European joint planning mechanism yet to help systematically fill US dependencies. But as European defense industries rebuild, and as European regional military cooperation gains momentum, joint procurement and development between neighbors is becoming more accepted.30

U.S. signals on conventional pullback are also reviving discussions about Europe’s nuclear options. France has begun formalizing conversations about the role of its nuclear arms in European security that were unthinkable a few years ago.31 While this is not a replacement for the U.S. umbrella, it marks the first steps toward diversifying a domain that Europeans long assumed was off the table.

Europe is unlikely to wholly substitute the role the United States has played in its security and defense. But Europeans have grown sufficiently skeptical of the U.S. security guarantee to set in motion a process of rearmament, defense industrial build-up, and strategic reorientation and reorganization that is unlikely to reverse.

The greatest concern for Europeans is the immediate future and the security risks created by a rapid U.S. withdrawal that outpaces European rearmament efforts. By 2030, Europe will not have replaced the American security guarantee outright, but with sustained political will—and budgets to match—it could close a substantial share of its dependencies. Some will remain in place longer: Europe is not yet pursuing a genuine substitute for the nuclear umbrella and many of the high-end capability dependencies beneath it take a decade or more to build. The more important shift is that Europe will have stopped trying to substitute U.S. power like-for-like. Europe is increasingly defining its own narrower objectives—deterring Russia and defending the continent—and its own way of warfare, leaning on lessons learned in Ukraine. The result is a more balanced interdependence in which Washington’s leverage grows materially thinner.

Both burden shifting and the coercive threat of retrenchment may reduce U.S. costs and increase U.S. leverage in the short term, but it comes at the price of defense-industrial export margins and agenda control. As Europeans invest in their own defense and security, Washington’s coercive power, derived from Europe’s military dependencies, will decrease.

European dependence on American technology is deep, growing, and difficult to escape on any meaningful timeline. The United States has a kill-switch capability unique to this domain, which shapes European technology procurement decisions. Yet the same depth of dependence that makes American leverage so potent also makes it costly to exercise: Europe is the largest foreign market for U.S. firms, so Washington’s threats are credibly limited by the political and regulatory response that a demonstrated use of the kill-switch capacity would trigger.

The United States’ technological power in Europe is concentrated in cloud computing, AI, chips, and connectivity. Network effects and scale keep U.S. firms entrenched, while credible alternatives remain thin.32 Rapid U.S. progress on AI has widened the capability gap and pulls European talent across the Atlantic. Amazon, Google, and Microsoft provide about 70 percent of Europe’s infrastructure.33 U.S. firms also dominate mobile operating systems,34 AI companies (ChatGPT, Anthropic), satellite internet (Starlink), and AI chips (Nvidia). Europe’s online public squares are likewise U.S.-owned, as Meta and X dominate social media.35 The result is not just a commercial success but a major emerging structural dependence: Europe increasingly operates inside an American technology stack.

A recent report by the Future of Technology Institute (FOTI) found that roughly three-quarters of listed European firms rely on U.S. tech.36 Reliance is highest in Iceland, Norway, Ireland, Finland, and Sweden, where over 90 percent of firms use U.S. cloud providers.37 The UK’s competition authority has found that Microsoft and Amazon Web Services control 60–80 percent of the UK cloud market.38 In the UK, France, and Spain, the biggest firms (worth altogether over $200 billion) were entirely dependent on U.S. tech.39 Europe has few homegrown providers—OVHCloud, SAP, and Deutsche Telekom are the exceptions, not the rule.

Europe’s response to this emerging area of dependency is threefold. The first track is regulation as both shield and lever. The General Data Protection Regulation (GDPR) established Europe as the global rule-maker in digital governance,40 and the Digital Services Act,41 the NIS2 directive,42 and Digital Operational Resilience Act (DORA) extend that role into platform accountability, cybersecurity, and operational resilience.43 These give Europe political leverage even where it lacks industrial and technological strength, but they also create friction with Washington—especially when U.S. leaders portray European regulation as discrimination against American firms.

The second track is industrial policy with a sovereignty frame. The EU Chips Act has spurred over $115 billion of investments.44 Brussels’s InvestAI initiative aims to mobilize $235 billion, including $23 billion for up to five AI gigafactories with a target output of 100,000 advanced AI chips. And pilot lines, such as IMEC’s NanoIC line, test processes below 2 nanometers.45 None of this yet produces sovereign capacity at scale, but the policy infrastructure, reinforced by the latest Cloud and AI Development Act (CADA) proposal,46 is now in place.

The third track is strategic partnerships outside the American technology stack. A proposed $20 billion tie-up between Canada’s Cohere and Germany’s Aleph Alpha, backed by both governments, is pitched as an escape hatch from U.S. AI infrastructure.47 EuroStack—the broader initiative for a European-controlled technology stack—depends on more such deals.

The strategy of turning to China as a hedging option complicates the picture rather than solving it. In some parts of Europe, lower dependence on U.S. providers has entailed deeper Chinese ties, notably through vendors such as Huawei and ZTE.48 But shifting away from the United States by accepting more Chinese infrastructure would simply replace one vulnerability with an even greater one. Brussels is moving to ban Huawei and other Chinese vendors from sensitive infrastructure, targeting telecoms, energy, transport, and security supply chains.49 Washington has cheered the crackdown and pushed for tighter transatlantic tech alignment—which is itself a form of leverage, since Europe’s anti-China tech posture deepens its dependence on the United States.

The kill-switch risk is the sharpest constraint on European autonomy and therefore the most consequential vulnerability. Because cloud services, AI tools, satellite communications, payment infrastructure, and software updates are controlled by U.S. firms under U.S. jurisdiction, Washington could, in principle, interrupt or even just slow down essential services to European users. Whether it would choose to do so is political rather than technical. Nevertheless, the possibility of such a scenario is already shaping procurement choices and forcing European policymakers to prepare for the contingency.

This makes technology the domain in which U.S. leverage is deepest, easiest to operationalize, and hardest for Europe to escape or even mitigate. Yet using this leverage would not be cost-free for Washington. A demonstrated use of its kill-switch capability would accelerate every European response—including through regulation, industrial policy, strategic partnerships, and capital allocation away from U.S. firms—and would damage American firms in their largest foreign market.

The conditions for Europe’s sovereign capability—capital, regulatory legitimacy, talent, and an industrial base—are more in place than the gap with the United States suggests, and the U.S. position is more contingent on European acquiescence than the asymmetry implies. Nevertheless, Europe is struggling to meet the promise and speed of AI that it would require to become a leader in tech policy.

Europe, more than perhaps any other region, staked its postwar identity and security on the premise of an exceptional United States—a democratic and benign hegemon underwriting a Pax Americana that genuinely benefited Europe and its peoples. The cultural foundation of American soft power—universities, technology brands, scientific prestige, and cultural production—remains largely intact. But the political foundation, which rested on the United States as a model of stable democracy and an effective foreign policy actor, has fractured.

Soft power stands apart from the other domains of power. This is not a zero-sum category: There are no direct competitors or indigenous alternatives to U.S. soft power in Europe. Instead, this category matters across domains. Trust in the United States—and its powerful attraction to Europe—has underwritten and stabilized the transatlantic alliance.

American soft power in Europe has rested on two distinct foundations. The first foundation is cultural and institutional: U.S. universities, Hollywood, technology brands, scientific prestige, and the ordinary draw of American life. Today, that cultural foundation remains largely intact and insulated from political swings. In 2023, Europeans highly rated U.S. technological achievements, entertainment, and universities.50 The cultural pull of the United States remains powerful enough that even sharp political ruptures produce only modest declines in tourism and university enrollment.51

The second foundation is political and ideological: the United States as a model of stable democracy, an effective foreign policy actor, and a credible standard-bearer for liberal values. This is more volatile. European confidence in the United States has over the last twenty-five years risen and fallen depending on which party controls Washington.52 European favorability collapsed during the 2003 invasion of Iraq,53 but was largely restored by 2008.54 It dropped sharply again during Trump’s first term, then recovered under president Joe Biden.55 Europeans have historically learned to wait out unfavorable U.S. presidencies, believing that the model itself will remain stable even when the leadership is not.

Two things suggest the current decline may break from that pattern. The first is the depth and breadth of the drop since Trump’s return to office. U.S. favorability has fallen across nearly every major European country—in many cases by twenty points or more in a single year.56 Only 30 percent of French and German respondents say the United States will have a positive influence on world affairs over the next decade.57 Majorities in Sweden, Germany, Spain, and the Netherlands describe Trump as dangerous.58

The second reason is structural. Europeans are reassessing the political foundation on which American soft power has been built. According to Pew’s Spring 2025 surveys, Europeans’ confidence that “democracy in the U.S. works” has dropped sharply. Their confidence in Trump’s ability to handle Ukraine, the international economy, U.S.-China relations, the Middle East, and climate is low across the board, suggesting they doubt not only the model of American democracy but the effectiveness of U.S. foreign policy leadership. When asked which country is the world’s leading economic power, majorities in Greece, Italy, Spain, Germany, Poland, France, and Hungary now name China rather than the United States.59

The institutional apparatus that translated American soft power into operational influence has been hollowed out alongside the political foundation. Combined with the erosion of U.S. democratic institutions—which Europeans are watching closely—the United States can neither model the form of governance it once exported nor deliver effective foreign policy. A future administration could rebuild these institutions, but it is unclear whether European trust will be restored on a five-to-ten-year horizon after watching a single administration unwind it in months.

Additionally, American soft power in Europe is no longer singular. Alongside the traditional model—liberal, multilateralist, and institutionally embedded—a version of America rooted in Trump’s Make America Great Again (MAGA) ideology has gained visibility, presenting itself as a revisionist force skeptical of multilateralism, critical of liberal institutions, and aligned explicitly with European political forces that contest the European project itself.60

So far, this rival vision has underdelivered. Pre-election interventions in Hungary failed to secure Viktor Orbán’s political survival and may have even contributed to his electoral loss.61 The MAGA agenda on migration, climate, and the EU remains attractive in principle to European far-right parties, but its association with the Trump administration’s actual foreign policy decisions is proving harder to sell: The Iran war drove up European energy prices and increased security risks. Since far-right electorates have absorbed those costs, far-right parties across Europe have been distancing themselves from Trump.62 Nevertheless, to the extent that MAGA ideology outlasts the current U.S. president, it would not add to American soft power so much as restructure it. Instead of a broadly shared attraction to a liberal, multilateral United States, the traditional model and its revisionist challenger would pull against each other—two rival Americas competing for different European constituencies.

The United States’ irregular approach to Europe has led Europeans to seek greater self-reliance and to search for alternative partners. Washington’s relative power in Europe is poised to diminish as a result, even as its absolute power persists. The trajectory for the U.S.-Europe relationship will therefore not be a dramatic European exit or U.S. escalation, but rather a slow, frustrated rebalancing in which the nature of American power evolves.

U.S. coercion does produce gains and Europeans are not asking for a wholesale divorce. Although they are seeking greater autonomy in the military realm, they lack alternatives that would make a real exit possible from decades of accreted transatlantic structure. They are also coming to realize that Washington faces its own constraints: While the United States theoretically dominates Europe in all domains of power, using its dominance fully would cost the United States far more than American citizens are willing to tolerate. U.S. leaders could, of course, impose devastating costs on Europe by cutting off access to LNG, AI, or extended nuclear deterrence. But Washington’s coercive capacity does not automatically translate into power, even for an administration as committed to using it as Trump’s has been. Europeans have learned that the costs of American coercion can be raised, and they have begun to do so.

Some may argue that we are overstating the future of American power on the grounds that the foundation of the United States’ power in Europe is its military defense of the continent—absent that, the other dimensions of American power would evaporate. While Washington’s role as security guarantor has historically had a stronger effect than its other forms of exercising power, the coming decade will test whether that hierarchy holds. Especially as AI becomes foundational to productivity, state capacity, and military capability itself, Europe’s technological dependence on the United States may come to supplant the foundational role that security dependence has played since 1949. U.S. hegemony in Europe and globally could increasingly rest on its position as a technological superpower rather than primarily on its security guarantee. If so, greater European military autonomy will still matter, but it will not by itself restructure the relationship because the crux of structural dependence will have changed.

Others may object that we have overstated the degree of European leverage over the United States. By this logic, European countermeasures worked during the 2026 Greenland crisis partly because most Americans did not support Trump’s ambitions in the first place. A harder test would be a coercive demand with real domestic backing over China. Yet the U.S. consensus on confrontation with China is softening, even as Europe’s own views of China have moved in Washington’s direction63: Where Europe’s China relationship was once defended as a commercial opportunity, it is now more often framed as exposure that must be managed.

We predict that the future of the U.S.-Europe relationship will not be a return to “normalcy” but the beginning, for the first time, of a true normalization. The post-1945 transatlantic bargain was historically exceptional. What is emerging now is a more conventional relationship between asymmetric partners with overlapping interests.

This evolution will not be undone by a change in U.S. political leadership. The financial and political investments Europe has made in response are sticky enough that they will not be simply reversed if or when Washington changes course.

For the U.S.-Europe relationship to normalize, a return to prior levels of trust is not required, but predictability is. A more stable U.S. articulation of its interests in Europe would help Europeans adapt. The current administration is unlikely to provide this predictability; it is built around the mercurial nature of a sui generis president. But future U.S. presidents, even if they are not transatlanticists, will likely once again put forward a more stable definition of the U.S. national interest that Europeans can engage with. How quickly and smoothly normalization proceeds will depend on both sides agreeing on the shape of their future bargain and sticking to it.

What is the future of American power? The United States commands extraordinary resources across every dimension of national power, yet in recent years it has struggled to achieve many important foreign policy aims. This paradox raises a key question for Americans and the world: What can the United States actually do with the power it has? Our project examines not just the quantity but the qualities of American power, assesses the degree to which it is eroding, and asks how the United States might use the power it has to better effect.

Senior Fellow, Europe Program

Sophia Besch is a senior fellow in the Europe Program at the Carnegie Endowment for International Peace. Her research focuses on European foreign and defense policy.

Tara Varma

Managing Director, German Marshall Fund’s Strategic Foresight Program; Director, German Marshall Fund Paris office

Tara Varma is the managing director of German Marshall Fund’s Strategic Foresight program and director of the organization’s Paris office.

Carnegie does not take institutional positions on public policy issues; the views represented herein are those of the author(s) and do not necessarily reflect the views of Carnegie, its staff, or its trustees.

Networks—from international payments platforms to key economic sectors—underlie many aspects of U.S. power. But they are suffering under an extractive approach to foreign policy.

Daniel W. Drezner

It seems likely that, no matter what, the power of the U.S. nuclear arsenal will face erosion, not least in the credibility of its commitments to defend allies and the political durability of those alliances.

James M. Acton, Ankit Panda

Democratic erosion is undercutting four key elements of U.S. power, with mounting and likely lasting effects.

Thomas Carothers

The future of American economic power will be determined by the interplay between Trump’s ambitions and the global backlash against them, as well as economic developments outside the direct control of the government, such as advances in AI.

Peter Harrell

State capacity is, at its core, the ability of governments to do what their citizens ask them to do. The Trump administration’s cuts come against a background of long-term capacity decay.

David E. Lewis