Commentary

Five major trends are shaping U.S. policy in the Middle East.

Daniel C. Kurtzer, Aaron David Miller

Alliances remain crucial to American statecraft in an era of great-power competition, but Washington needs to be clear eyed about their costs and benefits.

Allies are essential to U.S. strategic competition with China but carry costs and risks that require continuous, realistic management. Polarization in Washington has unfortunately impeded the correct approach: critics on the right are too narrowly focused on military power while advocates on the left underplay the real costs and risks involved in U.S. defense commitments.

Across the political spectrum, experts are now calling on allies to shoulder more of the burden for security in the Indo-Pacific. This is positive, but plans to deepen U.S. alliances also need to weigh allied political will and the danger of being drawn into conflicts that do not serve vital U.S. interests.

This report inventories these costs and benefits for seven key alliances across eight core areas of U.S.-China strategic competition. We conclude that:

We stress that if Washington consistently pursues a statecraft that undermines allied trust in the United States, allied leaders will not support U.S. global objectives, weakening America’s hand in competition with China. Some recent U.S. policies, such as the Trump administration’s broad tariffs, appear to have eroded trust.

The United States does not need a revolution in its alliances, which remain a source of strength for America at a time when U.S. power is under strain globally. But Washington does need to move with greater caution when deepening them. Ensuring alliances serve the needs of American citizens at a time when the world is in flux will require realism, periodic reassessment, and continuous adaptation.

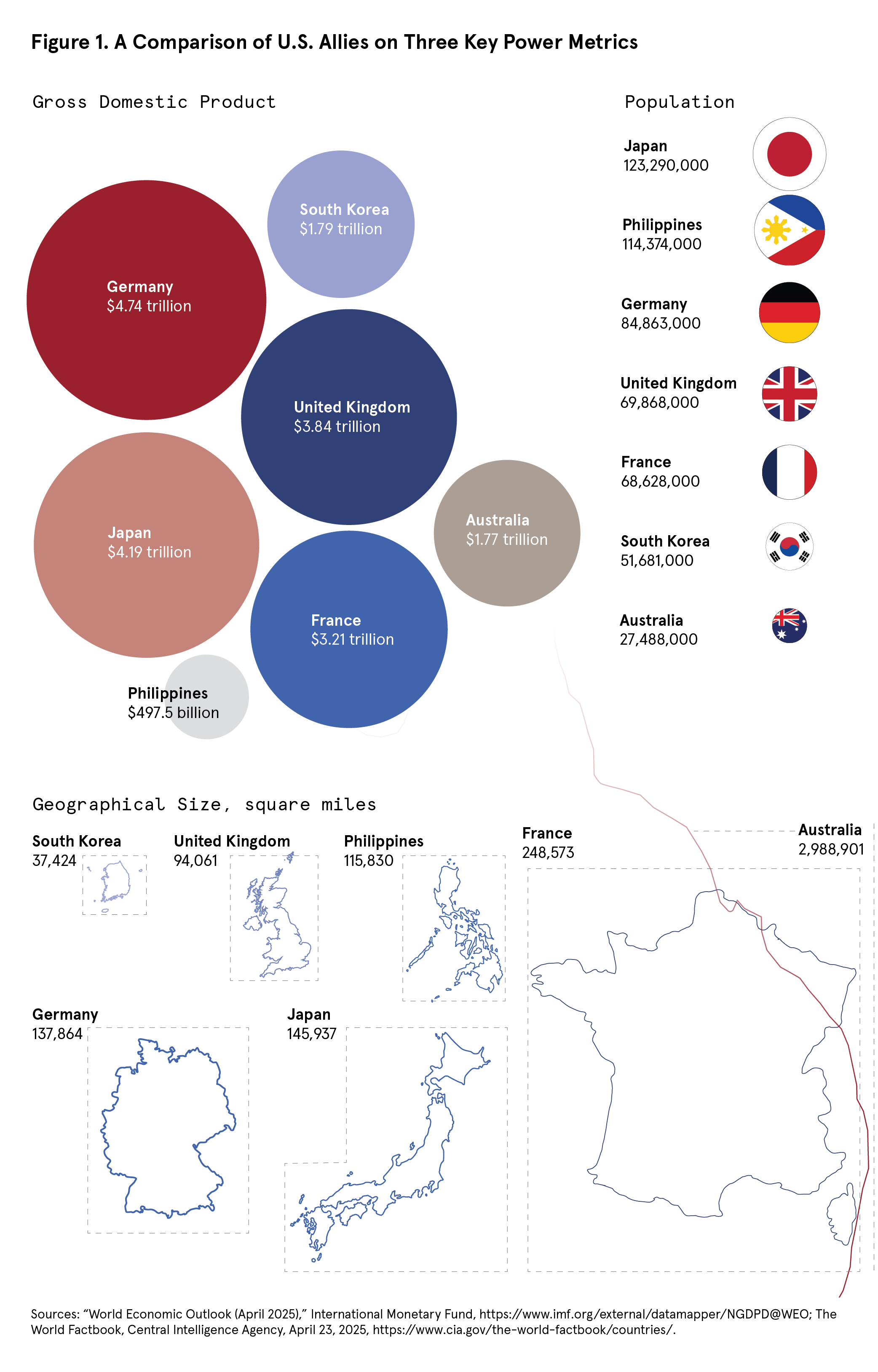

Alliances remain crucial to American statecraft in an era of great-power competition, but not all alliances are equally fit for purpose when it comes to the China challenge. This report assesses seven key allies’ concrete contributions to U.S. China strategy—and their limits—across military, economic, and technological domains, factoring in each ally’s capabilities, political will, and entanglement risks. The comparative analysis indicates that while some alliances bolster U.S. aims vis-à-vis China, others offer more modest benefits, sometimes with greater risks.

Whether U.S. alliances are fit for purpose is an essential question U.S. policymakers must constantly be asking and answering. Presidents Donald Trump and Joe Biden debated it. Trump has been skeptical of allies while Biden warmly embraced them. Both approaches had merits, and both had drawbacks. The fact is, alliances are not inherently good, as Biden evinced, nor inherently problematic, as Trump often has. Alliances can greatly amplify a nation’s political, military, and economic strength—but they can also entrap nations in unnecessary wars, create security dilemmas, and drain resources.

The key question U.S. strategists and policymakers must confront today is whether the costs associated with current U.S. alliance structures are justified by their benefits. Some see the durability of U.S. alliances as a sign of their success, but durability may simply reflect habit. The historical legacies of America’s alliances of course offer benefits—better working relationships between allies, for example—but at the end of the day, if U.S. alliances do not yield concrete benefits toward America’s key strategic goals, serious reforms will be needed.

A number of prominent experts now recognize the need for fresh thinking about U.S. alliances, but more can be done. On the positive side, recent discussion of alliances has broadened to include more attention to economic, technological, and diplomatic power. For example, former Biden officials Kurt Campbell and Rush Doshi have emphasized the need to develop the nonmilitary dimension of U.S. alliances in Asia by deepening allied capacity across the board.1 Also on the positive side, Republican and Democrat-aligned experts, such as Elbridge Colby and Ely Ratner, have emphasized the importance of U.S. alliances paying clear and concrete benefits to the United States.2

Both the broader perspective and the emphasis on benefits to the United States are welcome and are central to this report. This study emphasizes the need to consider two additional factors, however: allied will and entanglement risks. Doing so provides a more complete cost-benefit picture of what allies truly contribute—and where Washington could exercise more caution.

To begin with political will, it is one thing for an ally such as Japan to express growing concern over China’s behavior, another for them to adopt Washington’s preferred China strategy. Treating allies as more than “tripwires, distant protectorates, vassals, or markers of status,” to borrow Campbell and Doshi’s phrasing, means more than asking allies to contribute capability—it also means accepting that they are independent and sovereign actors whose interests align only imperfectly with the United States. Grand plans for strengthening U.S. alliances need to face up squarely to the reality that allies have wills of their own. Doing otherwise runs the risk that in an effort to bring them around to U.S. strategy, Washington will end up offering allies more security protection than is warranted—thus opening the path to greater strategic overextension.

Entanglement—being dragged by allies into conflicts of limited U.S. interest—has been debated in academia but needs to be taken seriously in policy discussions.3 Skeptics argue that evidence of entrapment in recent decades is limited to a handful of cases. If U.S. relative power is declining globally, however, the risks of entanglement may increase as U.S. adversaries act more boldly and create more crises, each of which offers the chance for U.S. entanglement. Meanwhile as U.S. relative power wanes, Washington may become more concerned about demonstrating its will and the strength of its commitments—and therefore more willing to adopt risky policies when the crises do arise.

Fear of entrapment or entanglement should obviously not be the sole consideration in determining U.S. alliance relationships, but those who argue that Washington can manage all its entanglement and entrapment risks down to acceptable levels are underestimating them. Entanglement is often conceived in terms of being dragged inadvertently into a war on account of a crisis, but some of the costs of entanglement occur well below the level of all-out war. Moreover, even if the probability of entrapment in an all-out war is fairly low, the risk varies from one case to another, and in all cases, the consequences of being entrapped in a war with China would be extremely high. At a minimum, those who downplay these risks put a very high level of confidence on Washington’s capacity to consistently conduct a skillful diplomacy that maintains sufficient flexibility to avoid war.

This report thus combines these three key elements of assessment—what an ally can bring, its will to cooperate, and the risk of entanglement—while taking a broad view of alliances that goes well beyond the military dimension. The focus is on support to U.S. strategy toward China. China is one of the central, or potentially the central challenge of U.S. foreign policy in the next decade, and as such it offers an excellent lens through which to consider what U.S. allies bring to the table.

Allies have increasingly been brought into U.S. strategy toward China since its aspirations to great power status became clear a decade ago.

Allies have increasingly been brought into U.S. strategy toward China since its aspirations to great power status became clear a decade ago. The Biden administration was especially conscientious about its use of alliances and other partnerships to strengthen deterrence in the Indo-Pacific, and the Trump administration has also touted the importance of allies in countering China, albeit with less consistency.4 Recently, Trump’s harsher approach to allies, along with his trade policies, have prompted concern among allied capitals about America’s reliability as a partner. Public opinion in several of the allies studied reflects a growing perception that the United States may be less dependable or less likely to come to their defense in a crisis.5

Too often the U.S. debate about allies has had a primarily military focus. Under the Biden administration, the AUKUS partnership with Australia and the UK was a leading example, as was the expansion of U.S. military basing in the Philippines. When it comes to strategic competition, nonmilitary contributions to U.S. security are hugely important, however. Consider, for example, the importance of allies in building more resilient global supply chains or supporting China-related U.S. objectives in multilateral fora and with third countries around the world.

To develop a more comprehensive framework for assessing U.S. alliances, we examined the written strategies and official policy statements of the Trump I, Biden, and Trump II administrations. From this, we derived eight primary areas where the United States expects allies to contribute to its China strategy:6

This report examines the capacity and will of seven key allies across these eight categories. The allies include the four major U.S. Indo-Pacific treaty allies—Australia, Japan, the Philippines, and South Korea—as well as its three major European allies—France, Germany, and the United Kingdom. We assessed each ally’s capacity and will to contribute concretely to the eight U.S. goals, assigning a value of “very important,” “somewhat important,” and “not important” in each case. These assessments are by nature subjective, but we have made every effort to ensure that they are congruent across the cases by adhering to clear definitions of what we mean by “very,” “somewhat,” and “not” important in each category—these definitions are provided in a section before the case studies.

The allies assessed were selected in part because they are widely viewed as key when it comes to China. They were also selected because the United States has treaty commitments to defend them, which means they all pose at least a theoretical risk of entanglement—although this risk varies widely as discussed throughout this report. Given the security commitments the United States has made to them, these allies should be expected to provide substantial benefits to U.S. security. Important partners like India or Taiwan are thus not included because the United States does not have a treaty commitment to defend them, although future analysis might usefully focus on them.

U.S. allies have been responding to the rise of China in different ways, and their policies have evolved over the course of the last decade. Few allies, if any, are as seized with the challenge that China poses as Washington has been, but concern has grown especially since the pandemic and China’s bungled diplomacy of that era. Allies in Asia have become more wary of China’s power and the possibility that it might destabilize the region with its ambition. This has fueled a deepening of U.S. alliances. Recent U.S. policies—the tariffs mentioned above, for example—could counter this trend, however.

Few allies, if any, are as seized with the challenge that China poses as Washington has been, but concern has grown especially since the pandemic.

Allies in Europe have tracked U.S. concern about China to some degree, but the degree has varied substantially by country. Even among the major U.S. allies in this report, there are clear variances. Germany’s deep investment in China’s auto industry creates headwinds for German leaders focused on meeting the geopolitical challenge from China. Political leaders in the UK have vacillated, while France under President Macron has sought to position Europe as a third pole in a U.S.-China-EU world—although one clearly still linked to the United States. The EU has acknowledged the challenge and sought a strategy of “de-risking” from China that would avoid economic and political decoupling altogether. China’s support for Russia’s war on Ukraine hardened Europe’s line to some degree, but not enough to bring key European capitals fully into line with Washington.

As of 2025, allied ability to meaningfully contribute to U.S. objectives with China thus varies substantially.

The benefits America gains from any single alliance may also be viewed in the context of the alliance system as a whole. Adding an ally to a network may offer benefits that go beyond those from a purely bilateral relationship—for example, if that ally serves as a crucial node in a network that would otherwise not function. Allies can also add military, economic, and political resilience. The challenge, however, is to determine what the marginal gain from a particular ally may be in terms of resiliency. After all, the more resilient a network of allies grows, the less important any particular ally becomes. A wise strategy would seek to limit U.S. costs and risks as the marginal benefit from adding additional allies diminishes.

This study brings together a wide range of data sources across what we assess to be the key issues that policymakers should consider in assessing the value of U.S. alliances. It also provides a framework that could be replicated in other cases to further deepen U.S. understanding of the value of its various alliance and partner relationships around the world. It is not intended as a comprehensive assessment of the overall value of U.S. alliances, nor the overall value of the allies assessed. The allies herein are assessed only in relation to their capacity to contribute to U.S. objectives on China. This is obviously very important, but it means that contributions that, for example, France makes to security in Europe are not considered herein.

A second limitation is U.S. strategy itself, which is evolving. We have attempted to assess allies against a synthetic version of U.S. China strategy, derived from primary sources. This is necessary in order to hold some aspects of a complex system constant. We are not intending to claim that the U.S. strategy is ideal—although it certainly has strong suits. A further study might assess the value of these allies against strategic alternatives, and as U.S. strategy evolves it will be useful to further refine or update the major categories. Similarly, as allied contributions shift, reassessment will also be warranted and additional allies may be added. Some important allies and partners have been scoped out of this study—the Netherlands, for example, is significant when it comes to supply chains, and India could bring a range of potential benefits but is not a treaty ally.

The next chapter compares the cases for an overall picture. Individual case studies follow.

A comparative assessment of our case studies reveals key differences among U.S. allies. Japan clearly stands out, followed by Australia and South Korea. In contrast, European allies, while influential economically and diplomatically, contribute far less to Indo-Pacific military needs. The Philippines, despite its strategic location, has limited capabilities and poses higher entanglement risk. This section details these findings across eight functional areas of competition, from semiconductors to security cooperation.

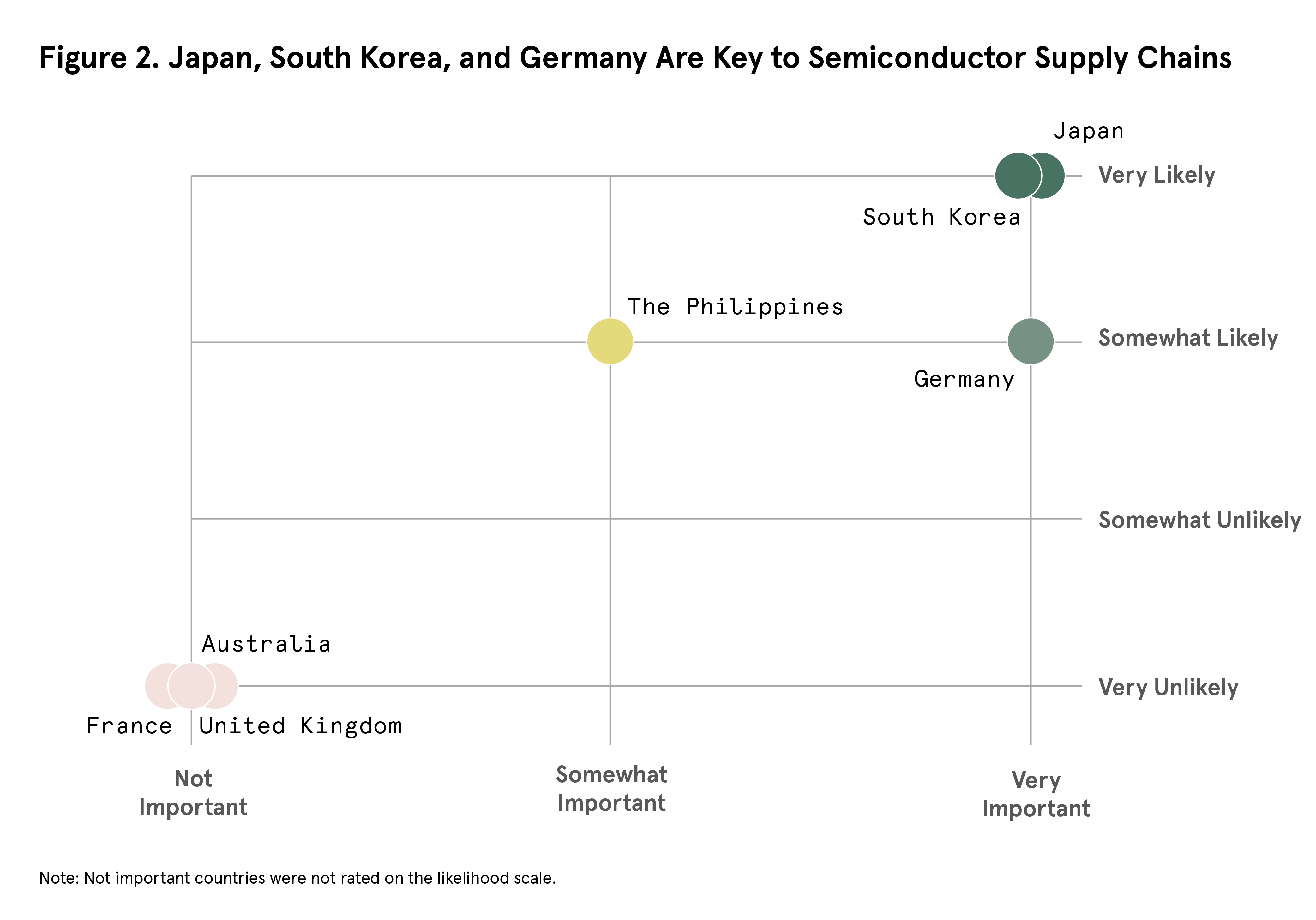

The United States and its allies currently dominate most cutting-edge chip design and manufacturing, but China dominates legacy chip production and is gaining ground with advanced chips. Our assessment of each ally’s importance in reinforcing American semiconductor supply chains is based on the size of the ally’s share of global manufacturing, machinery, materials, parts, and chip production capabilities for both cutting-edge and legacy chips. Given China’s dominance in outsourced semiconductor assembly and testing (OSAT), we place particular emphasis on allies that have OSAT capabilities. (We recognize that other U.S. allies such as the Netherlands make substantial contributions here, but they are outside our scope.)8

Japan, South Korea, and Germany are the key U.S. allies when it comes to “friendshoring” advanced semiconductor manufacturing.

These three allies are also likely to be willing to assist the United States with friendshoring. While South Korea and Japan remain wary of antagonizing China, each aligned its supply chains with the United States in response to the 2022 CHIPS and Science Act and have taken legislative action to bolster their roles in the semiconductor supply chain through strategic investments.

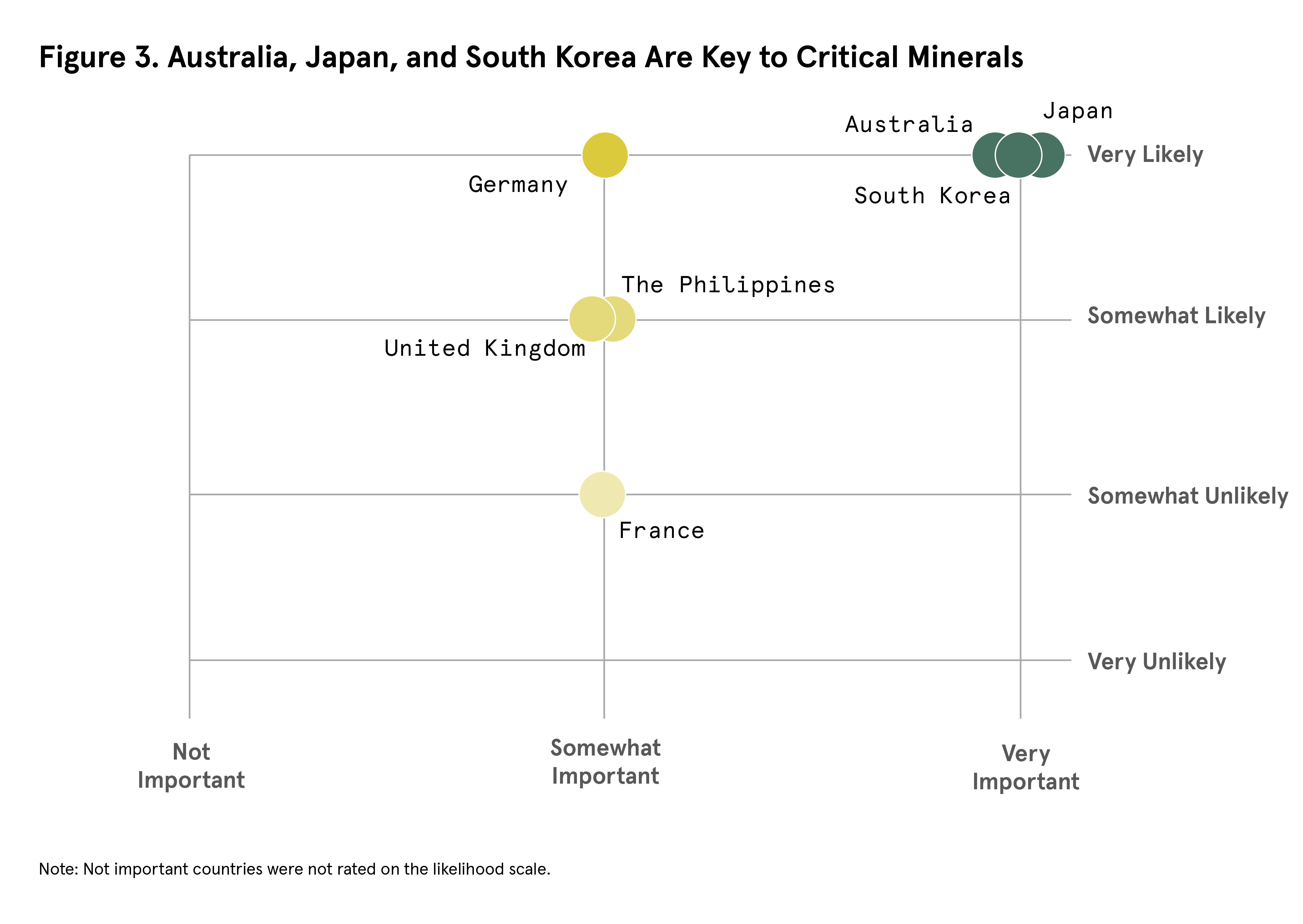

Critical minerals are important for a variety of strategic applications. For the purposes of this study, we focus on twenty minerals used in the manufacturing of advanced batteries, rare earth permanent magnets, advanced semiconductors, and arms production. These applications were chosen as key technologies that will influence future economic and military capabilities in the strategic competition between the United States and China. The full list of minerals and applications can be found in Appendix 3.

Given that these twenty minerals are all relatively scarce and are essential for manufacturing these applications, we do not distinguish between their comparative importance. Allies’ raw material contributions are crucial, as U.S. supply chains here are weaker than in chips and more vulnerable to Chinese leverage. To assess the extent to which allies can contribute to strengthening U.S. resiliency in this area, we focused on whether the ally had important critical minerals reserves, large-scale mining operations, or high-volume processing and refining capabilities.

Germany, the Philippines, the United Kingdom, and France are also able to contribute to strengthening critical minerals supply chains, but to a lesser degree. For example, Germany produces polysilicon for semiconductors and has lithium deposits and refining capabilities.21 The Philippines is the world’s second-largest miner of nickel and the sixth-largest producer of cobalt.22 The United Kingdom has refining capacity for platinum and the potential for large scale lithium refining.23 Its tungsten deposit at Hemerdon, one of the largest in the world, could supply significant volumes of tungsten for key defense applications.24 France has committed efforts to build a domestic critical minerals supply chain including launching a rare earth element production line for permanent magnets.25

After the COVID-19 supply chain shocks and due to the risk of China’s withholding critical minerals in response to U.S. export control measures, most U.S. allies recognize the importance of reinforcing supply chains, so we expect them to continue to support the process. Some countries, such as the Philippines—and to some extent the UK—face domestic hurdles to developing their capabilities. The Philippines, for example, needs stronger and more business-friendly mining infrastructure and regulatory frameworks.

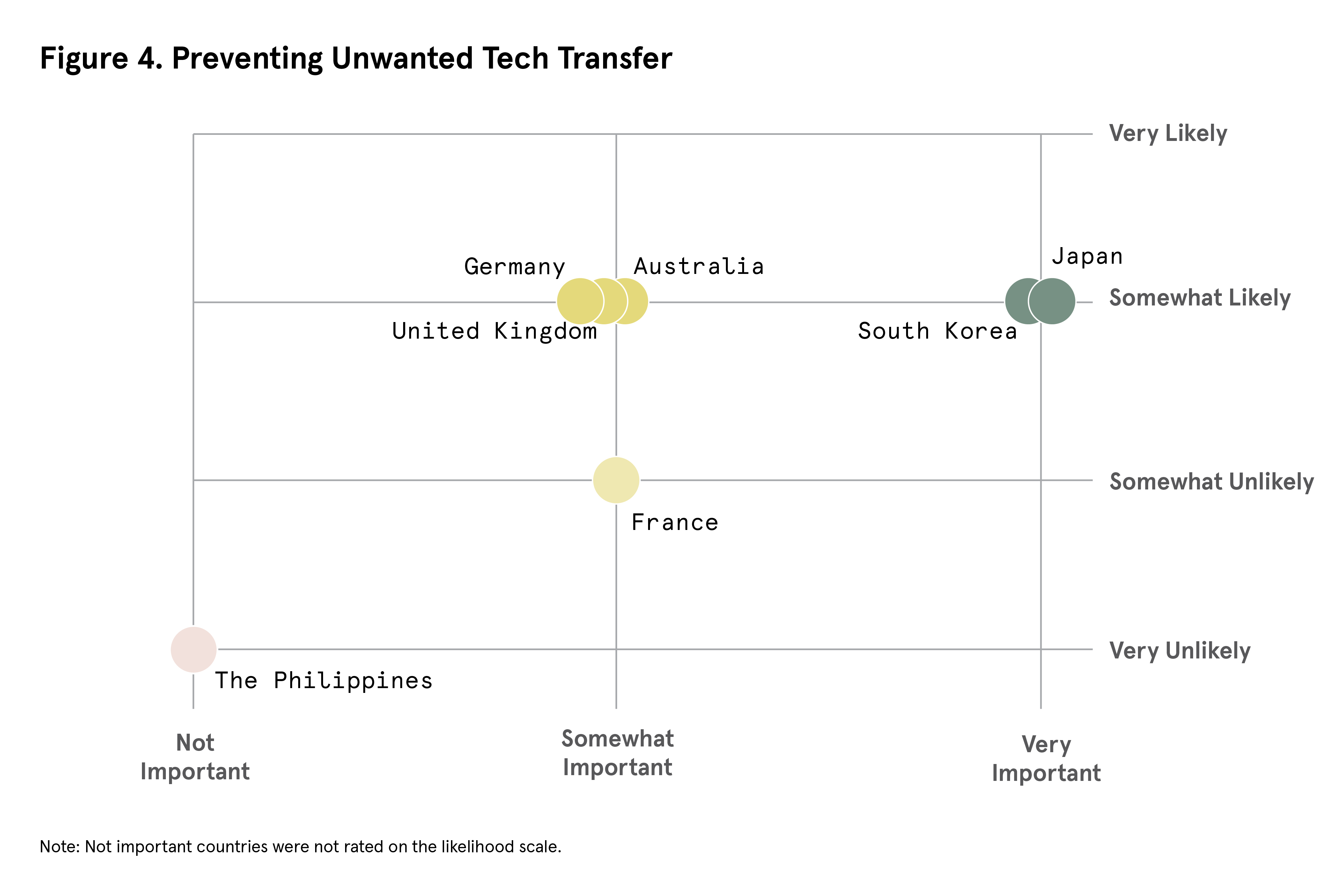

U.S. allies still have some sensitive and proprietary technologies—especially microelectronics, advanced computing and quantum technologies, artificial intelligence, and advanced telecommunications—that the United States seeks to deny to China. Those allies’ cooperation in preventing unwanted technology transfer will therefore be important to Washington.

That said, U.S. allies have so far done less than the United States to prevent unwanted dissemination of their technology to China. This is largely due to concern over Chinese retaliation and lower levels of concern about the consequences of technology transfer in the first place. Germany’s chip and automotive markets are currently very intertwined with China’s, for example, making technology restrictions especially vulnerable to such retaliation. Policies are evolving, however, as evidenced by Japan and the Netherlands’ decision to cooperate with the United States to limit the export of advanced chipmaking technology to China.

The United Kingdom, Germany, Australia, and France are also important, however, given their chip design capabilities and quantum computing research. The Philippines is the only ally in our study which is not important when it comes to protecting proprietary advanced technology.

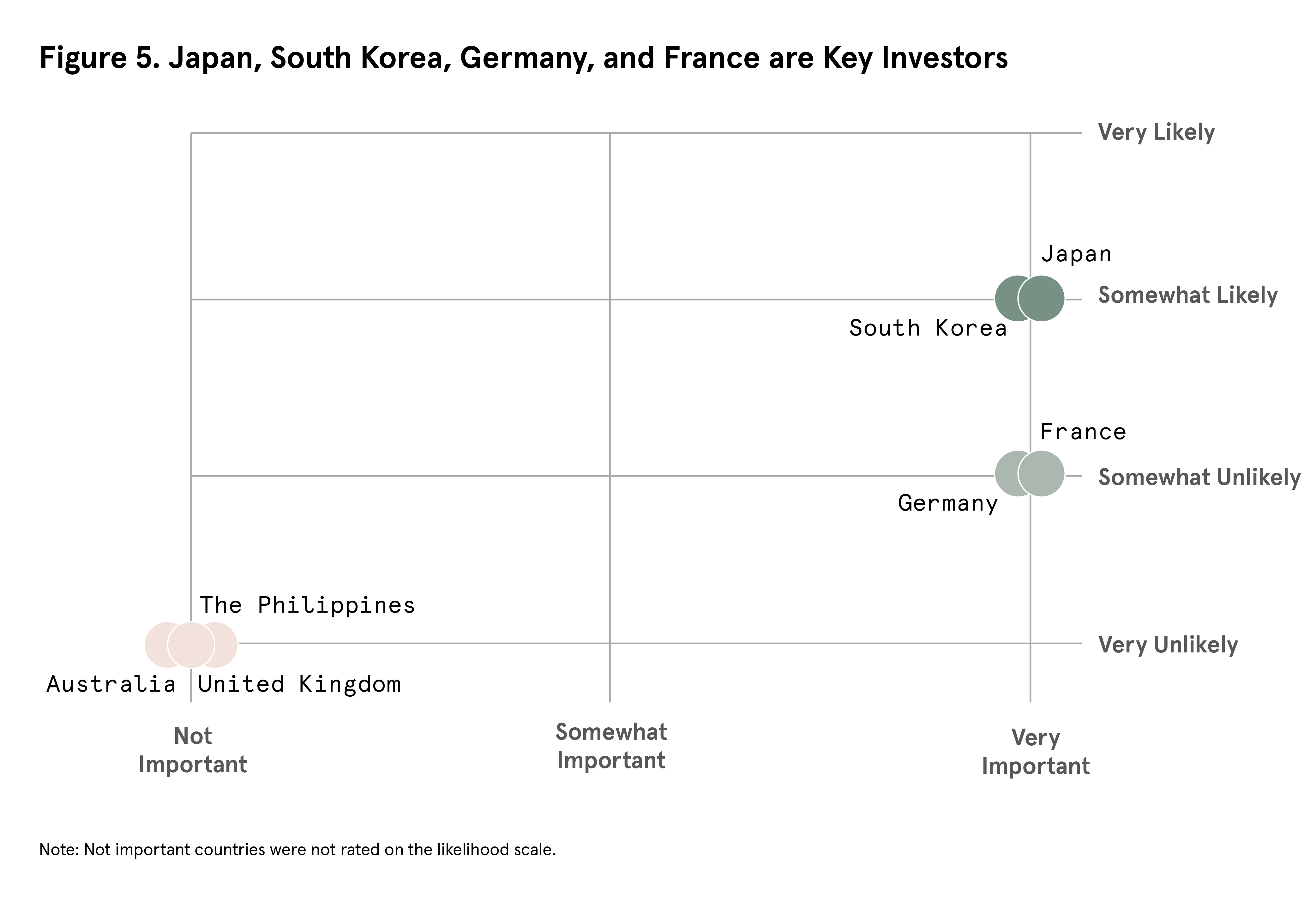

Allied foreign investment in China’s technology sector could pose risks if it strengthens China’s military capabilities. We thus examined whether allies were important contributors to China’s inbound FDI, how much is in advanced technology manufacturing, and whether allies have outbound FDI screening regimes.

Many allies are in the process of developing their outbound investment screening tools, although they may not place the same emphasis on controls as the United States. The relatively smaller size of their venture capital markets, however, reduces the importance of doing so while the importance of external markets for some—such as Germany, South Korea, and Japan—raises the cost of following the United States’ lead.36

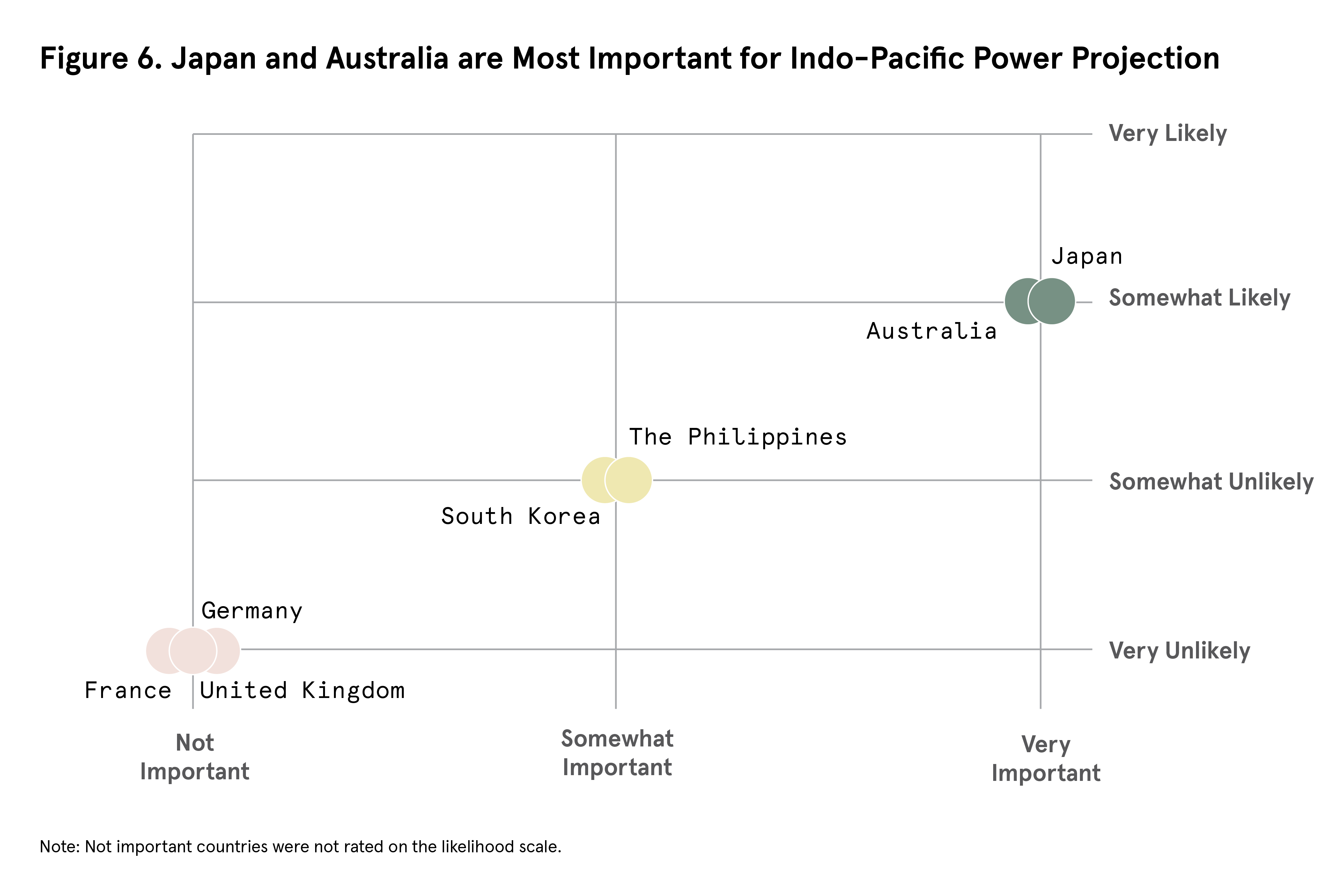

Given the Indo-Pacific’s size and distance from the continental United States, the U.S. military relies on allied basing and logistics to project power into the Indo-Pacific. Some allies also offer strike capabilities relevant to regional deterrence.

Japan and Australia both have a history of housing U.S. personnel or equipment, engage in consistent logistics coordination with the United States, and have native strike capabilities. Importantly, they would likely—although not certainly—offer support in the event of a war.

South Korea is home to large numbers of U.S. forces and has its own offensive capabilities. Those capabilities are directed against North Korea, however, and Seoul has historically been reluctant to countenance providing military support to the United States in a conflict with China. The Philippines is also a somewhat important partner due to proximity to Taiwan, but its own military capabilities are limited.

The question of whether U.S. allies in the region would in fact join the United States in a conflict over Taiwan is more fraught than often acknowledged. In the event of a war, several factors would influence allied levels of support for the United States, including domestic politics, how the conflict began, and China’s own threats and efforts to deter their participation. This ambiguity is gradually diminishing as China’s assertiveness grows, but it remains a sobering strategic dilemma for Washington.

America’s allies in Europe are not relevant in this category today—with the exception of some intelligence contributions of the United Kingdom. European military capabilities are rapidly increasing, but their focus remains, as it should, on securing Europe against Russian aggression.

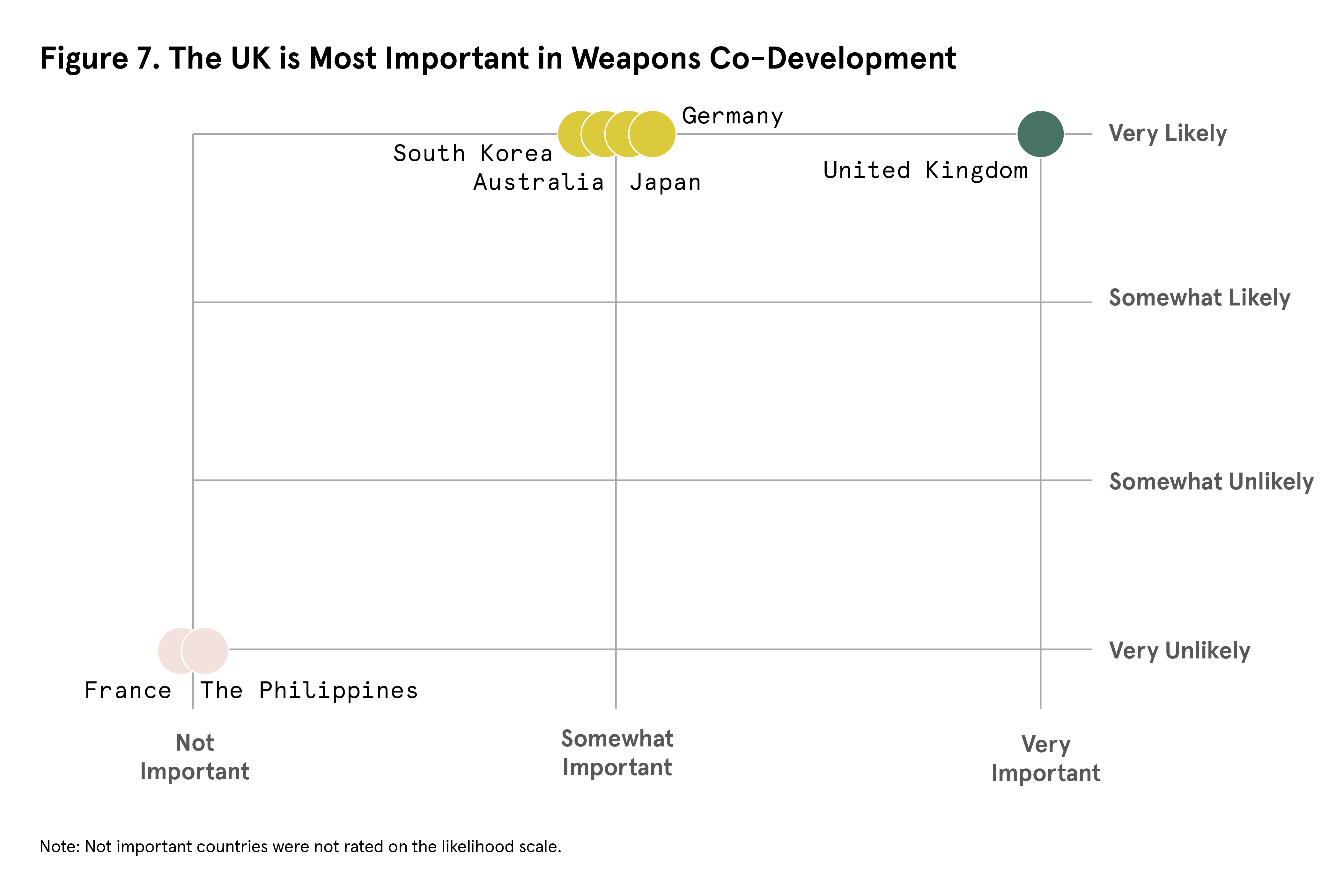

As Ukraine-related concerns about shortfalls in the U.S. defense industrial base have grown, Washington has looked to allies to help fill gaps. Allies also participate in longstanding co-development initiatives that aim to spread costs and benefits of large weapons platforms such as the F-35. An ally’s importance in such areas can best be gauged by their past record, technological prowess, and size of their defense industry.

Allies can shape structure and outcomes in global and regional institutions relevant to competition with China. We thus assessed allied capability across key international organizations—globally and in the region—through monetary contributions, voting power, and leadership positions.

The extent to which allies are willing to align themselves with the United States in international forums when it comes to China varies. The United Kingdom is probably the most aligned in this regard, with the other allies often, although not always, following the U.S. lead.

The Global South’s importance in U.S.-China competition is debated and can be difficult to measure, but it would be a mistake to ignore. Allies with influence stand to contribute, for example, through development aid, finance, and diplomatic weight. We use allied development assistance and institutional capacity for investment as rough proxies for influence. It should be noted that several allies—Europe especially—that have played important roles are now cutting funding.

The foregoing comparison should help clarify which alliances are worth the most attention and investment from Washington policymakers and alliance strategists. There are real benefits from alliances but also risks and limitations to what can be achieved. Pushing allies beyond what their domestic politics will likely allow or failing to account for the increased entanglement risks with some allies, could thus backfire.

When domestic public sentiment, political leadership, economic interests, or national geopolitical objectives diverge from U.S. goals, allies are obviously going to be far less inclined to support them. Moreover, even though allied concern about the challenge China poses has increased the willingness and capabilities of allies to support U.S. goals, perceptions of the United States are not altogether rosy.65

As discussed in detail in the case studies that follow, it would be a mistake not to also consider entanglement risks, which vary widely. Some allies amplify deterrence with little downside (Australia, Japan), while others, such as the Philippines, raise the danger of unwanted escalation for the United States. These risk assessments should factor more clearly in alliance design and management.

The United States should invest in its alliances, but with appropriate realism and restraint. America’s alliance network is an asset but must be frequently refined and recalibrated. U.S. strategy should prioritize its relations with allies that deliver the most impact, work with Europe to leverage their potentially strong nonmilitary contributions, and be realistic about gaps in allied political will and over-commitment risks. U.S. alliances can be fit for purpose in the twenty-first century, but only with clear-eyed adjustments to align them with today’s strategic realities.

“Friendshoring” aims to minimize vulnerable points in critical supply chains through relocating to or creating redundancies in manufacturing capabilities in allied countries.

Very Important

Somewhat Important

Not Important

Very Important

Somewhat Important

Not Important

Very Important

Somewhat Important

Not Important

Very Important

Somewhat Important

Not Important

Very Important

Somewhat Important

Not Important

Very Important

Somewhat Important

Not Important

Very Important

Somewhat Important

Not Important

Very Important

Somewhat Important

Not Important

This ally provides little ODA or is an ODA recipient.

The U.S.-Australia alliance has received growing attention from experts as Australia’s once warm relations with China have run aground. Australia is a capable partner across a range of issues, although it brings fewer resources—military or economic—than some other allies. It is also far smaller in population than the other allies in this report. The alliance with Australia, however, does not demand as much from the United States as some other alliances—there is little likelihood of being inadvertently entangled in a war with China on account of Australia. Canberra is also likely to continue to assist Washington in reinforcing supply chains, limiting China’s access to advanced technology, co-developing weapons systems, and providing development assistance to the Global South. It would be very important in a war over Taiwan—though its participation is not guaranteed.

Australia’s long-standing relationship with the United States has significantly deepened over the last decade, including with several initiatives for containing China. Its 1952 ANZUS Treaty with New Zealand and the United States is the foundation of the alliance.66 Since then, Canberra and Washington have coordinated closely on international crises and worked together on counterterrorism in the Middle East and dispute-resolution in the East and South China Seas.67 Importantly, Australia is a member of the “Five Eyes” intelligence group.68

Since their 2005 free-trade agreement, bilateral goods and services trade between Australia and the United States has more than doubled, and two-way investment has more than tripled.69 In 2023, Australia had the eighth-largest direct investment position in the United States at $116 billion, as well as the fourth-largest trade surplus with the United States at $17.3 billion.70 The two economies have become more integrated, but the Trump administration’s tariff policy might change this.71

The 2021 launch of AUKUS was a key development,72 through which the United States will share advanced nuclear-propulsion and sonar technologies to co-develop nuclear-powered submarines.73 Following their ministerial consultations in 2023, Australia granted the United States additional access to its airbases and agreed to host U.S. submarines for “regular and longer” visits.74 The two countries also launched a Strategic Commercial Dialogue in 2022 with the aim of strengthening trade relations, cooperating on critical supply chains, and coordinating responses to common threats.75

Prime Minister Anthony Albanese worked extensively with then president Joe Biden bilaterally and within multilateral groupings, such as the Quad with India and Japan.76 He has said he had “very warm” phone calls with Trump, and the two leaders have signaled their intent to meet to discuss AUKUS and tariffs.77 The relationship with the United States fared well during Trump’s first administration, when Australia was one of only two countries exempted from its tariffs on steel and aluminum.78 Public opinion about the United States is on a downtrend, however. According to the Lowy Institute, Australians’ trust in the United States has fallen by 20 percent since 2024, reaching its lowest level in the institute’s two-decade history.79

Australia’s relationship with China has been turbulent over the last decade. The two countries proclaimed a “comprehensive strategic partnership” in 2014, but tensions mounted from 2017 when Australia’s domestic intelligence agency issued a warning about Chinese interference through political donations.80 In 2018, Canberra introduced anti-foreign interference legislation and banned Huawei and ZTE from 5G networks, prompting Beijing to cut off diplomatic ties.81 Relations deteriorated further in 2020 when then prime minister Scott Morrison called for an investigation into the origin of the COVID-19 pandemic in China. In response, Beijing imposed heavy tariffs on Australian goods and detained several Australian nationals.82

Australia’s relationship with China has been turbulent over the last decade.

The Labor government in office since 2022 has pursued rapprochement with China through “strategic equilibrium” and “stabilization,” a shift from the more confrontational approach of the previous Liberal-National Coalition government.83 This has meant softening the rhetoric about China and working to ease mutual export restrictions, while being careful not to distance Australia from the United States.84 Albanese went to China in 2023 for the first prime-ministerial visit there in seven years, and followed with a second official visit and meeting with President Xi Jinping in July 2025.85 At the time, he said that, even with the removal of trade restrictions and the restoration of diplomatic contacts, the relationship would likely “remain difficult.”86

One manifestation of the tensions between China and Australia has been recent naval exercises by the Chinese navy in the vicinity of Australia.87 The U.S. military operates closely with Australian counterparts and in theory could become entangled in a military crisis between Australia and China. Right now, however, this possibility is remote. The recent standoff between Australia and China has the character of mutual posturing by regional powers rather than the raw aggression that has characterized China’s military and grey zone operations in the South China Sea—both Australia and China have been careful to keep the potential for accidental escalation low. On balance, therefore, America’s alliance with Australia poses the least risk of entanglement of any U.S. ally in the Indo-Pacific.

Australia is not an important ally for the United States in “friendshoring” semiconductor manufacturing supply chains because it lacks commercial-scale manufacturing facilities for semiconductors, relevant manufacturing equipment and OSAT capabilities.88 Australia also does not domestically produce and refine input materials necessary for semiconductors. Australia does possess research and development capabilities in semiconductor technologies in its universities and research institutions.89 National- and state-level initiatives are seeking to develop Australia semiconductor R&D capacity through industry and university partnerships. While U.S.-Australia collaboration under AUKUS Pillar 2 does not explicitly cover semiconductor supply chains, its goals for cooperation in advanced technologies including AI, quantum, and electronic warfare rely on securing semiconductor supply chains.90 Overall, Australia has little to offer the United States that would help it shift the production of legacy or leading-edge chips away from China.

On the other hand, Australia is very important for U.S. critical mineral interests. Australia possesses large scale deposits across many of the critical minerals and rare earths essential for U.S. strategic applications. It is the world’s largest miner of lithium and rutile titanium and the fourth-largest miner of rare earth elements for magnets and a leading rutile producer.91 Australia possesses among the world’s largest reserves of lithium, cobalt, manganese, nickel, tantalum, tungsten bauxite (for gallium), and zinc (for germanium).92 Australia is attempting to build refining and processing facilities for lithium, graphite, cobalt, rare earths, and high-purity silicon.93 In May 2025, Australia’s Lynas Rare Earths became the first facility to separate the materials and produce rare earth metal oxide outside of China, with its Malaysian refinery successfully refining dysprosium and terbium, two key rare earths in high-performance magnets.94 The company has signed a contract with the U.S. Department of Defense to build a processing facility in Texas, but it is uncertain if it will be built.95 The potential for Australian gallium production for advanced semiconductors as a byproduct of bauxite processing could be especially important for U.S. interests, since China has a near monopoly on global supply.96

Australia possesses large scale deposits across many of the critical minerals and rare earths essential for U.S. strategic applications.

Australia has demonstrated ongoing political interest in assisting U.S. efforts to pivot critical mineral supply chains away from China. However, Australia currently sends a large share of its minerals and rare earth elements to China for refining, creating a key chokepoint in the critical minerals supply chain.97 To remedy this, it is investing in its processing and refining capabilities, as part of the Critical Minerals Strategy 2023–2030.98 Canberra has undertaken domestic efforts to redirect its supply chains, including over four-billion-dollar in tax incentives to produce critical minerals through 2034, aimed at reducing reliance on Chinese sources. As part of the Quad and the Minerals Security Partnership, it participates in several U.S.-led international efforts internationally to diversify the processing and refining of critical minerals away from China.99 Australian Strategic Minerals also received a letter of interest for $600 million of funding from the U.S. Export-Import Bank (EXIM) to develop rare earths and critical minerals mining.100

Australia has a small semiconductor industry, but investments in quantum computing, space, and resource technology and biotechnology make it a somewhat important ally to the United States when it comes to preventing the unintentional dissemination of sensitive technologies to China. It ranks ninth globally in quantum research output and it is a global leader in superconducting circuit-based quantum processors, with the company Diraq producing the highest-fidelity ones to date.101 Australia also has a robust biotechnology innovation and research sector, with expertise in synthetic biology, vaccine development and clinical trials, but lacks the capacity to produce biotechnology products at scale.102

The Lynas Rare Earths Ltd. Processing plant in Kalgoorlie, Western Australia on August 3, 2022. Lynas is the world’s only commercial producer of separated heavy rare earths products outside China. (Source: Carla Gottgens/Bloomberg via Getty Images)

Australia is very likely to continue working with the United States in this regard. It shuttered its technological research programs on several fronts with China in 2019.103 Having banned Chinese technology companies Huawei and ZTE from its 5G networks, this year it banned the use of the Chinese AI DeepSeek app from federal-government devices.104 Australia is collaborating with the United States and United Kingdom under AUKUS Pillar 2 to coordinate the development and deployment of “advanced capabilities” with active working groups on: quantum technologies, artificial intelligence and autonomy, advanced cyber, undersea capabilities, and innovation.105 For example, the “Quantum Technologies” working group has established the AUKUS Quantum Arrangement (AQuA), an initiative to coordinate American, British, and Australian RDT&E efforts concerning quantum technologies such as alternatives for positioning and navigation systems.106 Australia and the United States have also taken steps to deepen their tech cooperation through public-private partnerships, such as the $3 billion investment by Australia in Microsoft in 2023.107

Australia is not an important ally for the United States when it comes to restricting FDI in China’s technology sector, largely due to the fact that its FDI in China is limited: Australian firms invested $450 million in China, while total FDI in the country was $163 billion.108 This investment is facilitated by the 2015 China-Australia Free Trade Agreement (ChAFTA) where Australian businesses have benefitted from lower tariffs.109 By contrast, that same year, China’s FDI stock in Australia was $57 billion and Hong Kong’s was $95 billion, making them respectively the tenth- and fifth-largest investors in the country.110 Chinese FDI in Australia is concentrated in mining and has expanded to healthcare and infrastructure in recent years, including a Chinese company controversially obtaining a ninety-nine-year lease on the strategic Port Darwin in northern Australia in 2015.111 Although China has reduced its FDI in Australia over the last few years, the size of its existing investments present a strategic vulnerability.

Australia is somewhat likely to support restricting its FDI in China’s technology sector, as well as technology transfers and military funding, exports and related services to China. The 2024 Defence Trade Controls Amendment Act and the Defence Trade Legislation Amendment Regulations intends for Australia to develop a “robust export control regime.” The Act introduced three new offenses concerning violations related to the supply, resupply, or servicing of goods on the Defence and Strategic Goods List to countries requiring permits, and established two implementation working groups for industry and higher education research.112 Australia does not, however, have a developed national security screening regime for outbound foreign direct investments and Australian firms are unlikely to stop investing in China altogether.

Australia is a very important ally for the United States when it comes to providing basing, logistics, intelligence, and strike capabilities for the U.S. military in the case of a Taiwan contingency. Australia does not allow permanent foreign military bases on its territory, but the United States has had a sustained rotational Marine Corps presence in the north of the country since 2012 and expanded access to key Australian air bases since 2017.113 Tindal Air Base in northern Australia, for example, was upgraded to accommodate deployments of U.S. B-52 strategic bombers, and U.S. B-2 Spirit stealth bombers were deployed to the air force base at Amberley in eastern Australia in 2022 and 2024.114 Under the U.S.-Australia Force Posture Agreement of 2012, both countries have invested in critical military infrastructure—such as maintenance and fuel facilities—positioning bases in northern Australia as “unsinkable aircraft carriers” to project U.S. power in the Pacific.115

Furthermore, under AUKUS Pillar 1, U.S. and UK nuclear attack submarines will be rotationally deployed from Perth in southwest Australia from 2027, supported by an expansion in local maintenance and shipbuilding capacity, while a new yard is under construction in Adelaide, South Australia, which will build nuclear-powered submarines.116 Through AUKUS, Australia is scheduled to receive three American Virginia-class nuclear attack submarines in the early 2030s, although there are significant doubts that the United States can raise submarine production output enough to meet this.117

Australia has precision strike capabilities including over seventy F-35A multirole stealth fighters and the U.S. HIMARS system.118 The Albanese government has committed over one billion dollars to purchase additional stocks of advanced medium-range missiles and is developing loitering munitions to strengthen air defense and aerial strike capabilities.119 At sea, Australia has purchased and tested U.S. LRASM anti-ship missiles and has Tomahawk land attack cruise missile–equipped surface vessels.120 Australia’s current Collins-class submarines are armed with anti-ship missiles and torpedoes.121

Australia is the only Indo-Pacific ally that provides high-value intelligence to the United States.

Australia is the only Indo-Pacific ally that provides high-value intelligence to the United States. It is a member of Five-Eyes and operates a joint satellite communications and signals intelligence surveillance base at Pine Gap since 1988. The Jindalee Operational Radar Network (JORN), which has over-the-horizon cover up to 3,000 kilometers, also provides valuable monitoring capabilities for U.S. operations in the region.122

Australia has increased bilateral and multilateral exercises with the United States.123 The Talisman Sabre, Pitch Black, and Predator Run multilateral training exercises have coordinated large deployments in the Pacific between the two countries and key allies and partners. Australia’s navy also conducts maneuvering exercises in the South China Sea with the navies of the United States and the United Kingdom.124 An Australian two-star general is embedded in the command structure of the U.S. Indo-Pacific Command,125 and in 2023 an Australian was appointed as the first foreigner in a deputy commander position in the U.S. Pacific Air Forces in 2023,126 underscoring the two militaries’ deepening integration.127

Australia has not committed to supporting Taiwan in a conflict.128 This reflects that fact that public opinion in Australia is divided over involvement in a war over Taiwan. In a 2023 poll, 42 percent of respondents said they supported Australia getting militarily involved if China invaded Taiwan (down from 51 percent in 2022) while 56 percent said they were opposed.129 The share of those saying they were “very concerned” about China opening a military base in the Pacific also dropped from 60 percent to 42 percent.130 In response to Chinese exercises around the island, Canberra often states that it opposes “any unilateral change to the status quo across the Taiwan Strait,” and it has encouraged “peace and stability” across the strait in joint statements with the United States.131 Canberra, like Washington, thus maintains a policy of strategic ambiguity in this regard. Various degrees of support are possible to imagine—for example, Australia could offer the United States support with logistics, command-and-control, intelligence, surveillance, and reconnaissance—but not deploy its own forces into combat.132

Australia is a somewhat important ally for the United States when it comes to co-developing military technology and adds value—but the United States would not be significantly disadvantaged if that cooperation were to end. There is collaboration across a wide range of advanced weapons systems including commitments to co-develop, co-produce, and co-sustain the PrSM, a next-generation long-range precision-guided missile for the HIMARS rocket system; co-producing and co-assembling GMLRS rockets in Australia by 2025; and co-producing M795 155 mm high explosive howitzer ammunition.133 Both countries’ governments and companies collaborate on the Guided Weapons and Explosive Ordnance Enterprise under which Australia has invested over $2 billion to acquire more long-range strike systems and manufacture longer-range munitions domestically.134 Australia also develops advanced aerial combat systems with the U.S. including the Integrator drone and the MQ-28 Ghost Bat autonomous “wingman” combat drone while Australian companies continue to participate in the production of parts for the F-35.135 Australia has also pledged to invest $3 billion in the U.S. submarine industry to support the timely delivery of the Virgina-class vessels it is due to receive.136

Australia can sustain its collaboration with the United States via its robust research ecosystem—which includes specialized technology fields such as quantum computing, hypersonics, and advanced materials—but this requires additional funding to maintain its waning competitive edge.137 Australia and the United States collaborate on hypersonic technology under the Hypersonic International Flight Research Experimentation program that was established in 2007.138 AUKUS includes a funding pool of $252 million for a Hypersonic Flight Test and Experimentation Project Arrangement, which will allow its members to use each other’s testing facilities and to share technical information to develop, test, and evaluate hypersonic systems.139 To facilitate the co-development of advanced military technologies, Australia was granted a partial exemption from the U.S. International Traffic in Arms Regulations (ITAR), such that over 70 percent of defense-related goods covered by ITAR no longer require State Department export licenses.140

Australia is very likely to continue co-developing military technology with the United States, particularly considering the long-term goals of AUKUS and the immense capital benefits Australia derives from this cooperation—although the small size of its defense industry and bureaucratic barriers are real limitations. As a part of its efforts to reconstruct its defence spending infrastructure, Canberra released its 2024 Integrated Investment Program (IIP) that allocated an additional $5.7 billion and $50.3 billion above the previous spending trajectory through 2033–34.141 The 2024 IIP also reprioritizes funding and directs a plurality of it to maritime readiness and long-range strike capabilities.142 Canberra launched the Advanced Strategic Capabilities Accelerator in 2023 to overcome these hurdles and to facilitate defense cooperation within AUKUS, committing up to $2.47 billion over the next decade to streamline funding.143 Projects include the Ghost Shark stealth and autonomous long-range submarine.144

Australia is a key ally for the United States in its efforts to deepen multilateral ties in the Indo-Pacific, including as a founding member of the Asia-Pacific Economic Cooperation (APEC), the Quad, and the Minerals Security Partnership. It does not, however, play a key role in global international institutions.

By total subscriptions and voting power, Australia ranked fifth among countries participating in the Asian Development Bank in 2024, and sixth among those in the China-led Asian Infrastructure Investment for 2025.145 Australia became first Dialogue Partner of the Association of Southeast Asian Nations (ASEAN) in 1974, established a “comprehensive strategic partnership” with it in 2021, hosted a fiftieth anniversary Australia-ASEAN special summit in 2024, and works closely with its members through the ASEAN-Australia Centre.146 Australia’s APEC Support Program gives technical support for economic development projects in regional neighbors including Papua New Guinea and Indonesia.147 Australia also plays a leading role in the Pacific Islands Forum (PIF), contributing approximately 36 percent of the budget for the PIF Secretariat in 2023.148 In 2022, Australia also joined the United States in launching the Indo-Pacific Economic Framework for Prosperity (IPEF), which aims to align the United States and its allies and partners in the region on supply chain resilience, clean development, and fair-trade practices.149

Australia voted with Washington in 73 percent of UN General Assembly votes in 2023, making it the ninth most-aligned country.150 Among Asia-Pacific countries, Australia was joint-first (100 percent) on Ukraine-related votes and second (73 percent) in votes classified as important by the State Department.151 However, Australia will not move in lockstep with the United States at the UN on contested issues such as the Israel-Gaza war.

We estimate that Australia has some degree of relevant influence in third countries of the Global South, especially in the Pacific. It is the world’s fourteenth-largest provider of ODA, with a budget of $3.4 billion for this fiscal year.152 Australia has been especially active in its neighborhood, for example, by engaging with Pacific Island nations through $630 million in economic assistance over five years and police-training initiatives.153 It has focused on countering China’s expanding influence and security presence in the Pacific, as evidenced by its $118 million four-year funding package to train new Royal Solomon Police Force recruits that would “reduce any need for outside support” after the Solomon Islands signed a bilateral pact with China.154 It allocates the bulk of its bilateral development assistance to countries in its neighborhood. In 2023, it devoted $1.2 billion to countries in Oceania and $962.3 million to countries in Asia, making it a significant alternative to China for assistance there.155 It does not have a dedicated development finance institution, but the Australian Infrastructure Financing Facility for the Pacific (AIFFP) provides infrastructure financing through loans and grants to contribute to a “stable, secure, and prosperous Pacific.”156

Aside from re-engagement with China diplomatically, the shift to a policy of stabilization under the Albanese government has not meant significant policy changes, and Australia remains largely aligned with the United States on China and foreign policy in general.157 The Labor Party’s win in May 2025 elections and Trump’s apparent good relations with Albanese signal strategic continuity. That said, Trump’s imposition of tariffs has not gone down well in Canberra, and Australians’ trust in the United States has fallen to its lowest point in two decades after Trump’s return to the White House. Thirty-two percent of respondents in one poll this year said they did not trust the United States to act responsibly in the world, compared to 16 percent in 2024.158 This could slow the cooperative momentum that has built up around China in recent years, limiting the scope for deepening cooperation across key strategic areas—especially if AUKUS were to run aground of political or other obstacles. Ultimately, Australia may share U.S. concerns about China, but it is looking at the problem from a different vantage point. Like the United States, it faces a challenge from China but also a risk of entanglement if it draws too close to other U.S. regional allies in this report.

Japan is the United States’ most important Indo-Pacific ally, a core player in the semiconductors sector, a technological giant, the world’s fourth-largest economy whose military capabilities are expanding, host to critical U.S. bases in the region, and a key partner to the Global South. U.S.-Japan economic relations are very robust—with bilateral trade worth $227.9 billion in 2024—and they are each the largest investor in the other’s economy.159 Japan has increased its defense spending in response to China’s military aggression and political assertiveness, but the United States remains its main source of security. While public opinion is mixed on support to U.S. operations in the event of a crisis or war over Taiwan, Japan is likely to continue supporting U.S. diplomatic and military efforts to promote a “free and open Indo-Pacific” in response to a more assertive China.

Over the past decade, the alliance between the United States and Japan has strengthened through regular high-level diplomacy, deepening economic integration, and increasing security ties across successive U.S. and Japanese administrations. Much of the change has come as Japan has recognized the challenge posed by China and steered away from decades of restraint on defense and toward a more active regional role. Its strategy over the last decade has combined an effort to build a strong regional network of partners with a more assertive security and defense policy in the service of a “free and open Indo-Pacific.”160

Whereas the United States once provided almost entirely for its security, Japan has recently embarked on a major transformation of its security policy that involves increasing defense spending to 2 percent of GDP, investing in key capabilities such as in cyber, and developing a long-range counterstrike capability that will allow it to strike targets in China and North Korea. Japan still needs the United States as a security guarantor, but its ability to defend itself and provide valuable capabilities for regional deterrence is increasing meaningfully.

Japan is the United States’ fifth-largest trading partner by export value and has the seventh-largest trade deficit with the United States ($68.5 billion in 2024).161 It is also the largest source of FDI in the United States by beneficial ownership, at over $783.3 billion in 2023. Japanese investments are primarily in the manufacturing sector, accounting for over $375.5 billion (16.8 percent) of FDI in U.S. manufacturing in 2023.162

A survey conducted after Trump’s imposition of tariffs in April 2025 found that 77 percent of Japanese respondents did not believe the United States would come to Japan’s defense in a crisis.

Japan has been subject to U.S. tariffs, however, which may explain a recent souring in Japanese perceptions of the United States. A survey conducted after Trump’s imposition of tariffs in April 2025 found that 77 percent of Japanese respondents did not believe the United States would come to Japan’s defense in a crisis—a notable increase from previous surveys, where fewer than 60 percent expressed such doubts.163 U.S. tariffs, and changing leadership in Japan following Prime Minister Shigeru Ishiba’s September 7 resignation, introduce new uncertainties in the relationship.164

The Sino-Japanese relationship is defined by Japan’s careful balance between its increasingly assertive posture and its pragmatic high-level diplomacy. Since 2004, China has alternated between being Japan’s largest and second-largest export market, highlighting a significant dependency on the Chinese market.165 The 2022 Japanese National Security Strategy took the important step of labelling China as the “greatest strategic challenge” to its security and calling for a decisive shift in Tokyo’s defense posture in the region, a buildup in its long-range strike capabilities, and an effort to strengthen the alliance with the United States.166 Tokyo has also maintained a high-level dialogue with Beijing through bilateral exchanges on the sidelines of international forums, however.167 Ishiba and his predecessor, Fumio Kishida, framed Japan’s China policy as aiming for a “constructive and stable” relationship. This underscores its dual-track approach: deterring aggression as the region’s key counterweight to Chinese power while preserving diplomatic and economic engagement.

The risk that the United States would be entangled in a war on account of its alliance with Japan is low. The main risk comes from the Senkaku/Diaoyu Islands dispute. These are a cluster of uninhabited islands in the East China Sea between Okinawa and Taiwan, the largest of which is about the size of Manhattan’s Central Park. The islands are claimed by Japan, Taiwan, and China, but have been under Japanese administration since the United States handed them over in 1972. Clashes between Japanese and Chinese coast guard and fishing vessels since 2010 have increased along with China’s growing regional assertiveness and developing naval forces. There is also growing tension between Chinese and Japanese air and naval forces in the area and China has claimed an air defense identification zone (ADIZ) that includes the airspace above the islands. Japan has meanwhile upgraded its military capabilities on neighboring islands.

Historically, the United States has carefully avoided taking a position on the dispute over whether or not the islands belong to Japan, but Washington has also made clear that it considers the islands to be under Japanese administrative control and therefore covered under the U.S.-Japan Security Treaty. This raises the possibility that America could be drawn into a conflict with China over these otherwise unimportant islets. As in the case of the South China Sea disputes, Washington might seek to meet its treaty responsibilities with economic sanctions or other nonmilitary means, but if Japanese forces were seriously harmed by China, it could become difficult to avoid some form of military action—especially given that the United States has trained jointly with Japan for such a scenario.168 Unlike the Philippines, however, Japan is a major regional power, with considerable and growing military forces and enormous political weight. This lowers the risk that the United States would actually be called upon to make good on its treaty obligations as a consequence of the dispute—both because Japan has more resources of its own and because China must move more cautiously in this case.

Broader possibilities that the United States could be dragged into a war with China by Japan are very remote.169 In theory, China might conduct a bolt out of the blue attack on Japan, firing its considerable missiles against Japanese military and civilian sites. But this seems extremely unlikely outside the context of a war that has already begun between China and the United States. Indeed, the most likely route to China-Japan conflict is a U.S.-China conflict over Taiwan, in which case China might seek to strike U.S. bases in Japan. In this scenario, Japan would be entrapped into a war by its relations with America, not the other way around.

As one of the world’s largest and most technologically advanced economies, Japan is a very important ally for the United States when it comes to diversifying semiconductor manufacturing supply chains.170 In 2022, Japan passed the Economic Security Promotion Act, a landmark law aimed at safeguarding critical infrastructure, securing supply chains, and promoting technological innovation in sensitive sectors such as semiconductors.171 This led to establishing the Leading-edge Semiconductor Technology Center that same year to strengthen domestic research on advanced chips.172

Caption: Tokyo University PhD student conducting semiconductor research at Tokyo University. Japan is known for its robust semiconductor research and development. (Source: Photo by YUICHI YAMAZAKI/AFP via Getty Images)

Japan is an important ally for the input materials and tools for advanced semiconductors as it dominates the coater and developer market and is a substantial producer of photoresists and other chemicals used in the extreme ultraviolet (EUV) lithography process. Tokyo Electron is the world’s third-largest supplier of semiconductor manufacturing tools, controlling a significant part of the market for photoresist coating application tools, which are an indispensable constituent of the photolithography process.173 Japanese companies make up 10 percent of the global semiconductors market but produce 88 percent of coaters/developers, 57 percent of wafer-cleaning systems, 53 percent of silicon wafers, and potentially up to 90 percent of photoresists—all key parts of the semiconductors production process.174 Japan also produces over 90 percent of EUV photoresists—a key material to manufacture chips more advanced than 7 nanometers (nm)—and it accounts for 75 percent of krypton fluoride/argon fluoride (deep ultraviolet) photoresists production—crucial components for manufacturing 130nm–22nm chips.175 To further boost its manufacturing capacity, Japan has partnered with the United States in the Rapidus venture aimed at producing next-generation 2 nm chips.176 TSMC, Taiwan’s preeminent semiconductors manufacturing company, also opened the Japan Advanced Semiconductor Manufacturing, Inc. foundry in 2024 that will diversify legacy and advanced chip production away from Taiwan.177 Japan also possesses domestic OSAT capabilities through an alliance of thirty companies that is seeking to reduce production costs, but still at smaller scale than Taiwan or American facilities.178

Japan is very important for U.S. critical mineral interests. Its secondary (recycled) platinum and palladium refining capacity accounted for around 10 percent of global demand in 2023.179 Japan is the second-largest producer of titanium sponge, which can be used to produce metal for aerospace structures and munitions.180 Japan refines antimony, is among the few economically advanced countries refining high-purity gallium, and operates one of the only lithium hydroxide facilities outside of China.181 Through producers like Shin-Etsu, Japan is also a producer of advanced rare earth magnets with a largely non-Chinese supply chain.182 Japan also produces refined nickel product and some recycled tungsten.183

Large quantities of cobalt, nickel, and yttrium deposits have been located in Japan’s EEZ at depths of over 5,000 meters near Minamitorishima Island (Japan’s most eastern territory).184 Despite plans to begin extraction from 2026, this is unlikely to be important in the medium-term due to the fact that deep sea mining at those depths will be difficult and expensive.185 Japan has a unique ability to secure its critical minerals supply chains by financing overseas extraction projects through the Japan Oil, Gas and Metals National Corporation (JOGMEC) and Japan Bank for International Cooperation (JBIC), the former of which partnered with the U.S. International Development Finance Corporation to coordinate global diversification of critical mineral supply chains.186 Japanese trading houses such as Mitsubishi have the experience, knowledge, and capital to support diversification and friendshoring, including through overseas investments.187

Given the volatility of Sino-Japanese relations, Japan has strong incentives to diversify and secure its semiconductors and critical-minerals supply chains by collaborating with the United States.

Given the volatility of Sino-Japanese relations, Japan has strong incentives to diversify and secure its semiconductors and critical-minerals supply chains by collaborating with the United States. Japan has joined the U.S.-led Minerals Security Partnership in 2022 and has signed the U.S.-Japan Critical Minerals Agreement to support the Biden administration’s clean energy friendshoring efforts in 2023.188 It also works with the United States in several forums to strengthen semiconductor supply chains, including the U.S.-Japan Critical Minerals Agreement and the trilateral Economic Security Dialogue with South Korea.189

Japan is a very important U.S. partner when it comes to preventing the unintentional dissemination of sensitive technologies to China. Beyond previously described capabilities in semiconductor manufacturing tools and materials for advanced chip production, it also retains a competitive advantage in NAND memory, power semiconductors, microcontrollers, and CMOS image sensors.190 In March 2025, the Japanese legislature enacted the AI Promotion Act, which created a guiding set of AI principles while encouraging coordination and innovation between industry and government.191 Japan has a high-end quantum research industry and ranks fifth globally in quantum research output—and among U.S. allies it ranks third in quantum computing, communications, and sensing research output.192 In 2025, Japanese IT company Fujitsu developed the world’s largest-class superconducting quantum computer with 256 qubits and the Japanese government announced a $7.4 billion commitment to quantum technologies. It led Western nations in public investments from 2023 to 2025.193 Japan also has a strong biotechnology sector, with research expertise in pharmaceuticals and biological sciences.194 While Japan’s quantum and biotechnology industries are growing, they both lag those in the United States and China, making them less important in this regard.

Japan has responded positively to the United States’ efforts to restrict exports of specific technologies to China over the last few years. A key development was Japan’s deal with the Netherlands in 2023 to restrict exports of certain advanced semiconductors technology and equipment to China.195 Following pressure from the Biden administration, Japan expanded its export restrictions to twenty-three leading-edge chip-making technologies that same year.196

That said, Japan is still more permissive than the United States. While Washington applies a strict presumption of denial, Tokyo exports to China whenever possible.197 Japanese semiconductors equipment providers are still reliant on Chinese markets for the largest share of their revenue: Japanese exports of semiconductors equipment increased across fiscal year 2024, with the percentage of exports to China rising from 39 percent in Q1 to 47 percent in Q4—evidence of how important allied cooperation on export restrictions can be.198 Yet, at the same time, Japan sees China’s advances in chip-making as a threat to the efforts to revive its own industry, and this is likely to shape its export policy for the foreseeable future.199

Japan is a very important ally for U.S. efforts to restrict FDI into China’s technology sector, due to the fact that it was the fifth-largest source of FDI in China in 2024, investing over $2.66 billion (although it has fluctuated some in recent years).200 Japanese companies are focusing their investments in China primarily in the technology, manufacturing, and automotive industries. For example, Toyota plans to establish a new wholly owned EV manufacturing plant in Shanghai in an effort to enhance its footprint in the world’s largest automotive market.201

Despite these ties, slowing Chinese economic growth, persistent operational challenges, intellectual property theft, and growing geopolitical tensions have all driven Japanese firms to diversify production to other countries.202 In a 2024 poll of Japanese firms, over half said they would either cut spending in China or keep it at current levels, a clear departure from the steady Japanese FDI increases in the years following the 2010 islands dispute.203

Japan has a very limited outbound FDI screening regime that requires prior notification for individuals or firms involved in weapons, narcotics, or leather goods.204 Given the size of investments in China, limited domestic markets and smaller venture capital sector, Japan is likely to be reluctant to enact further outbound FDI restrictions.205 FDI data and corporate sentiment point toward a recalibration of Japanese business strategy in Asia but not a full decoupling from China.

Japan and the United States signed their Mutual Security Treaty in 1960, and Japan today hosts more U.S. military personnel than any other country in the world. These forces include the largest Air Force combat air wing, a carrier battle group, and several nuclear-powered submarines.206 Around half of these forces are stationed on Okinawa, but there are several other U.S. bases in Japan, such as the headquarters of the U.S. Seventh Fleet in Yokosuka and of U.S. Forces Japan at Yokota Air Base.207 Kadena Air Base in Okinawa is home to the 18th Air Wing.208 Japan’s strategic location and the extensive U.S. military presence there make it a very important base for responding to any Taiwan contingency.209

Japan’s military forces are also developing rapidly. The 2022 National Defense Strategy marks a significant departure from the country’s post-Second World War consensus on the constitutionally mandated restraint on defense issues and points the way toward a more robust deterrent capability. Japan has also committed itself to increasing defense spending to 2 percent of GDP—a level unprecedented in the postwar era.210 It is also in the process of strengthening its advanced cyber capabilities and procuring a counterstrike weapons system that will allow it to strike targets in China and North Korea.211 This signals a higher level of military readiness and will add an additional deterrent to Beijing’s operations against Taiwan and elsewhere in the region. Japan already has advanced anti-submarine warfare, anti-ship warfare, and maritime reconnaissance capabilities.212 Japan possesses indigenously produced anti-ship missiles, has ordered U.S. Tomahawk land attack missiles for counterstrike, and is developing hypersonic gliders for deployment on land by 2026.213 With over 140 on order, its air force will operate the largest fleet of F-35 stealth multirole fighters outside the U.S. Air Force and has domestically produced F-2 fighters which can launch supersonic anti-ship and land attack missiles.214 Japanese submarines are equipped with indigenously developed torpedoes and anti-ship missiles, and the navy is developing a long-range submarine-launched cruise missile.215

The extent of Japan’s contributions to U.S. operations, should China attack Taiwan, would likely depend on how the conflict starts.

While the U.S. bases in Japan could play a significant role in a Taiwan contingency, the extent of Japan’s possible support for U.S. operations remains somewhat uncertain. Previously, Japan’s role in a Taiwan contingency was rarely discussed, but now the strategic environment has markedly changed and this issue has emerged as a key focus of U.S.-Japan military planning.216 There is growing recognition in Japan that any conflict over Taiwan would directly impact the country’s security, which is reflected in the shift in public and policy discourse on Japan’s involvement from virtually nonexistent to increasingly mainstream. Public opinion is divided over Japan’s role in a war over Taiwan, but a majority envisions providing some form of support to the United States (see Table 3). The extent of Japan’s contributions to U.S. operations, should China attack Taiwan, would likely depend on how the conflict starts and whether the parliament can justify declaring a state of emergency.217

Japan’s advanced industrial base makes it an increasingly valuable partner to the United States for co-developing certain military technologies, particularly as it relaxes its de facto ban on arms exports. For decades, cooperation was somewhat constrained by this obstacle, with co-development of the Standard Missile-3 Block IIA missile-defense interceptor and the F-2 fighter the only exceptions.218 Restrictions have been gradually relaxed since the de facto ban was lifted in 2014.219 Since, the United States and Japan have started co-producing advanced air-to-air missiles and U.S. designed Patriot PAC-3 missiles, while Japanese companies produce some advanced engine components for the F-35 program.220 Japan’s naval forces are also closely integrated with the U.S. navy through common upgrades of the Aegis ballistic missile defense system.221

The United States and Japan signed a Memorandum of Understanding for Research, Development, Test and Evaluation Projects in 2023 that could strengthen technology for hypersonics and counter-hypersonics, critical areas given China’s rapid advances in this field.222 In 2024, the State Department approved over $200 million in foreign military sales to support Japan’s development of the Hyper Velocity Gliding Projectile program.223 Both countries are also exploring cooperation in outer space, including in deep-space observation, deep-space radar, and standalone space-domain-awareness satellites to monitor China’s expanding anti-satellite arsenal.224 Lifting the ban also opened the door for Japan to work with other U.S. allies, including by collaborating in the Global Combat Air Program with Italy and the United Kingdom and by bidding to export frigates to Australia.225 Japan may also participate selectively in the AUKUS security partnership between Australia, the United Kingdom, and the United States on advanced technology initiatives.226

Japan is a very important and increasingly influential ally in international forums and has taken a leading role in advancing a free and open Indo-Pacific—a concept it first articulated under then prime minister Shinzo Abe in 2016—to counter China’s aspirations for regional hegemony.227 It is also a founding member of APEC and signed a “Comprehensive Economic Partnership” with ASEAN in 2007 and collaborates with ASEAN through the Japan-ASEAN Ministerial Initiative for Enhanced Defense Cooperation (JASMINE) to expand efforts to “create a security environment that does not allow any unilateral attempts to change the status quo by force or coercion”—a statement easily interpreted as aimed at China.228

While the alliance with the United States remains the cornerstone of its security strategy, Tokyo is working to diversify and to deepen its security partnerships across the Indo-Pacific and beyond.229 Within multilateral groupings such as the Quad, the Trilateral Strategic Dialogue, and the Security and Defense Cooperation Forum, as well as through other groupings with Australia, the Philippines, and South Korea, Japan plays a central role in shaping regional security norms.230

Japan also contributes to regional economic development as the leading contributor to the Asian Development Bank, holding the largest voting share on parity with the United States in 2024.231 It has also brought anti-dumping cases against China in the World Trade Organization and pushed the G7 to counter Chinese economic coercion when it chaired the group in 2023.232 Japan is also closely aligned with the United States in the United Nations: for example, it voted similarly in 90 percent of UN Security Council votes in 2023, when Japan held a nonpermanent seat.233 Among the Indo-Pacific countries, Japan was the most aligned with the United States on Ukraine votes (100 percent) and fourth on “important” votes (70 percent). However, not holding a permanent seat in the Security Council limits Japan’s influence in the UN.

Japan’s robust development finance institutions and its long history of overseas development lending make it a key partner for the United States when it comes to influence in the Global South and providing countries of the Global South with alternatives to financing from China in particular. Among the members of the Organization for Economic Co-operation and Development, Japan was the fourth-largest provider of official development assistance (ODA) in 2024.234 In 2023, Japan allocated a massive $10.8 billion in bilateral assistance to Asian countries, $2.6 billion to African countries and $1.6 billion to the Middle East.235 Japan puts enormous financial power toward development projects overseas to compete with China, leveraging its development finance institutions. The Japan Bank for International Cooperation (JBIC) finances projects and exports globally, and the Japan International Cooperation Agency (JICA) administers all Japanese ODA, through grants, loans, and technical cooperation. Japan demonstrated its significance in the development finance space when it launched its “Partnership for Quality Infrastructure” in 2015, two years after China launched the BRI. This initiative accelerated infrastructure assistance across Asia through JICA, in collaboration with the ADB.236 Japan deploys its development assistance in South and Southeast Asia in ways that compete directly with China’s.237 In 2023, Japan amended its Development Cooperation Charter to allow ODA partnerships aimed at enhancing economic security cooperation.238

Abe proved to be pro-United States and hawkish on China, but the more pragmatic Ishiba sought to prioritize Japan’s needs in its relationships with China and America instead of pursuing a balancing strategy against either. Ishiba’s resignation in September 2025 amid inflation at home and coping with the Trump administration’s tariffs presents challenges for stable relations.239 Still, Tokyo’s concerns about the threat posed by China may make even more dovish politicians favor deepening ties to Washington on the issue. For example, a joint statement in February 2025 took the allies’ support for Taiwan a step further by saying Japan (and the United States) would support “Taiwan’s meaningful participation in international organizations.”240 China recalled diplomats from Japan to protest this development, but Tokyo has not changed its position.241 Japan’s next prime minister will take up the difficult tasks of navigating ongoing trade and investment talks with Washington and fulfilling commitments to strengthen Japan’s own defense capabilities. Despite frictions, the alliance is deeply rooted. Japan and the United States have the potential to continue mutually beneficial close collaboration across economic, technological, and security domains—unless their domestic politics get in the way.